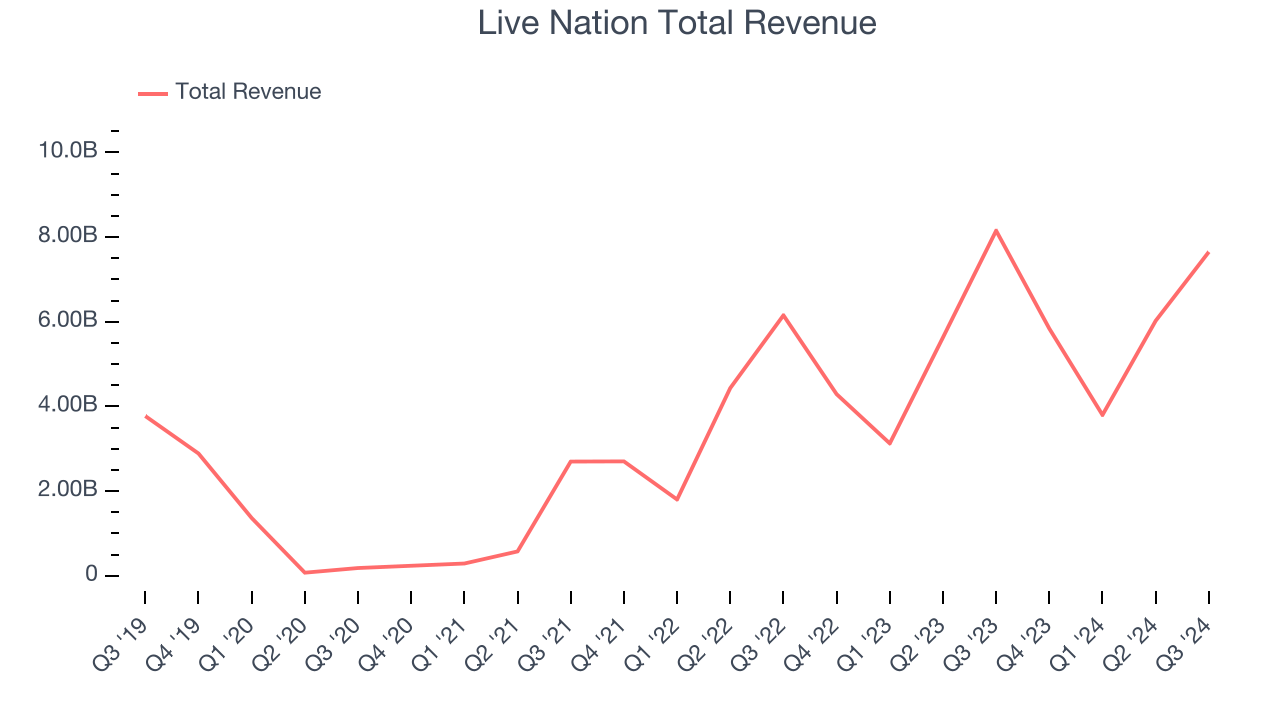

Live events and entertainment company Live Nation (NYSE: LYV) fell short of the market’s revenue expectations in Q3 CY2024, with sales falling 6.1% year on year to $7.65 billion. Its GAAP profit of $1.66 per share was 3.9% above analysts’ consensus estimates.

Is now the time to buy Live Nation? Find out by accessing our full research report, it’s free.

Live Nation (LYV) Q3 CY2024 Highlights:

- Revenue: $7.65 billion vs analyst estimates of $7.81 billion (2.1% miss)

- Adjusted operating profit: $910 million vs analyst estimates of $$862 (5.6% beat)

- EPS: $1.66 vs analyst estimates of $1.60 (3.9% beat)

- Growing concerts pipeline in large venues (stadiums, arenas, and amphitheaters), up double-digits compared to this point in 2023; stadium pipeline up double-digits compared to this point in 2022

- Over 20 million tickets already sold for Live Nation concerts in 2025, pacing up double-digits

- Gross Margin (GAAP): 24.5%, up from 22.3% in the same quarter last year

- Operating Margin: 8.4%, in line with the same quarter last year

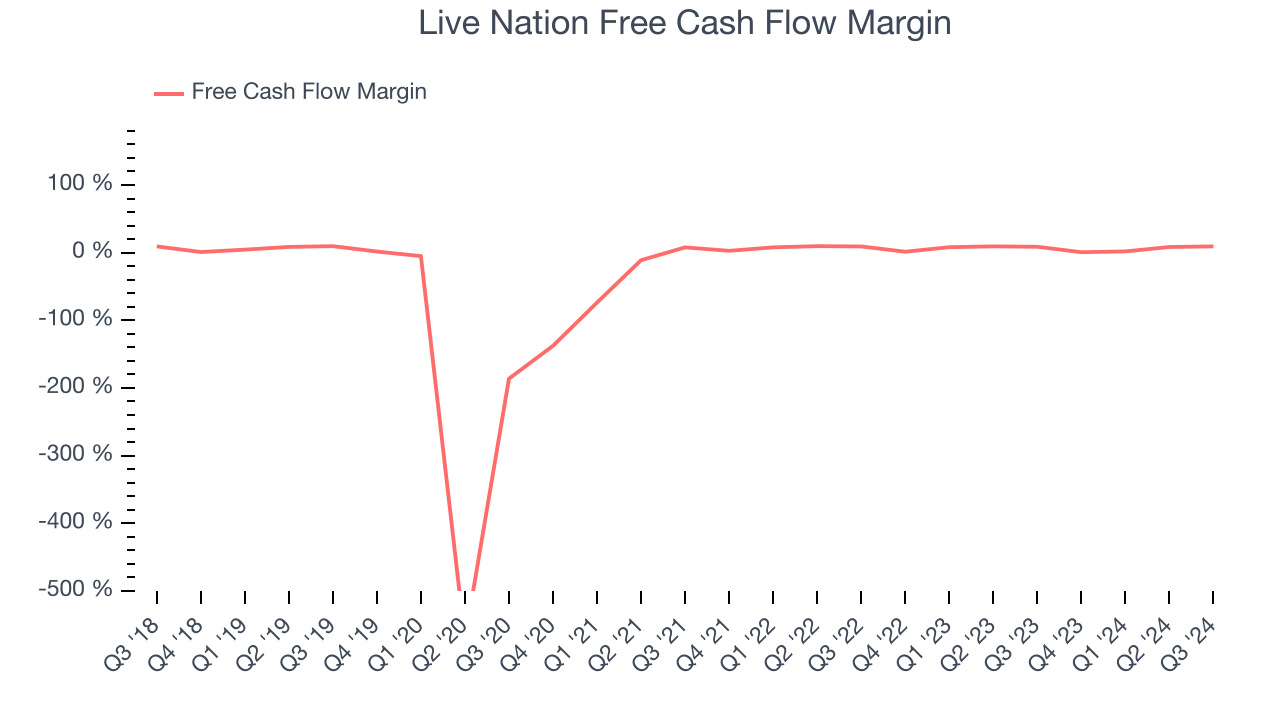

- Free Cash Flow Margin: 9.3%, similar to the same quarter last year

- Market Capitalization: $28.33 billion

Company Overview

Owner of Ticketmaster and operator of music festival EDC, Live Nation (NYSE: LYV) is a company specializing in live event promotion, venue management, and ticketing services for concerts and shows.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Sales Growth

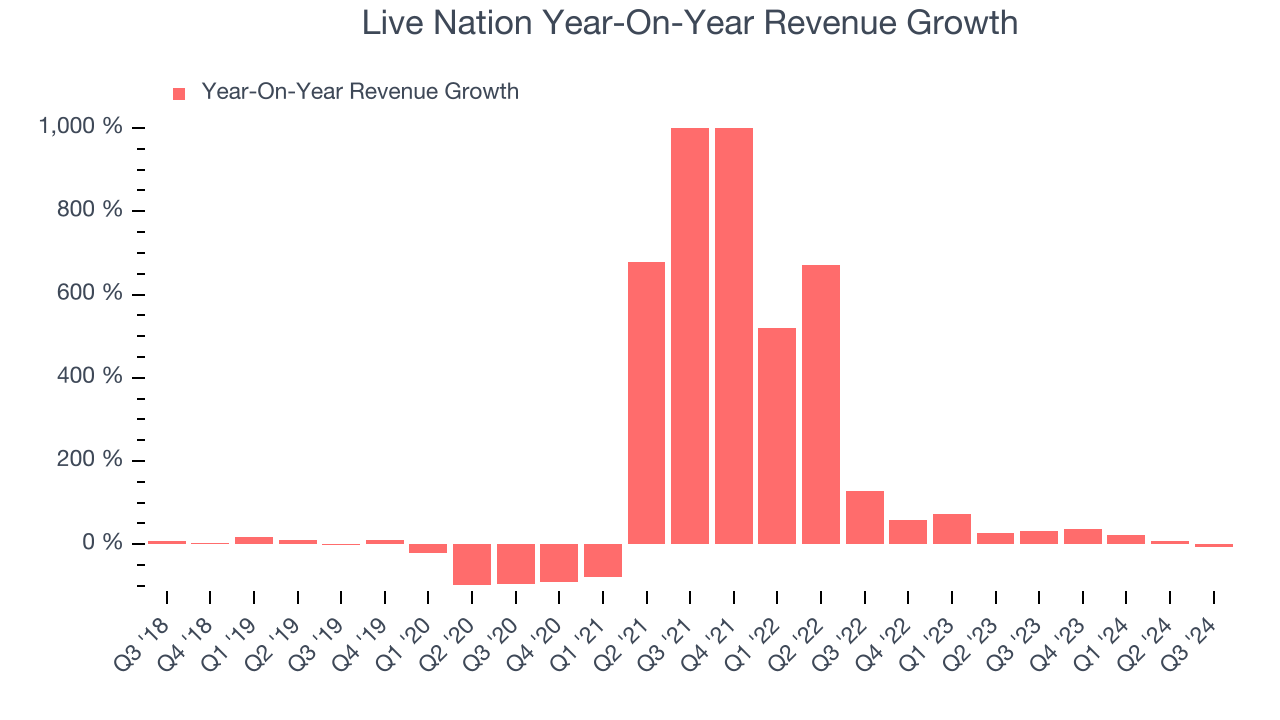

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Over the last five years, Live Nation grew its sales at a decent 15.7% compounded annual growth rate. Its growth was slightly above the average consumer discretionary company and shows its offerings resonate with customers.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Live Nation’s annualized revenue growth of 24.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated. Note that COVID hurt Live Nation’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

This quarter, Live Nation missed Wall Street’s estimates and reported a rather uninspiring 6.1% year-on-year revenue decline, generating $7.65 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 12.3% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Live Nation has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 6.5%, subpar for a consumer discretionary business.

Live Nation’s free cash flow clocked in at $712.4 million in Q3, equivalent to a 9.3% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

Over the next year, analysts’ consensus estimates show they’re expecting Live Nation’s free cash flow margin of 5.7% for the last 12 months to remain the same.

Key Takeaways from Live Nation’s Q3 Results

Revenue missed but adjusted operating profit and EPS both beat. The company also made encouraging comments about the pacing of the concert pipeline and tickets already sold for 2025. The stock traded up 4.3% to $129.27 immediately following the results.

So should you invest in Live Nation right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.