As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the hardware & infrastructure industry, including Diebold Nixdorf (NYSE: DBD) and its peers.

The Hardware & Infrastructure sector will be buoyed by demand related to AI adoption, cloud computing expansion, and the need for more efficient data storage and processing solutions. Companies with tech offerings such as servers, switches, and storage solutions are well-positioned in our new hybrid working and IT world. On the other hand, headwinds include ongoing supply chain disruptions, rising component costs, and intensifying competition from cloud-native and hyperscale providers reducing reliance on traditional hardware. Additionally, regulatory scrutiny over data sovereignty, cybersecurity standards, and environmental sustainability in hardware manufacturing could increase compliance costs.

The 9 hardware & infrastructure stocks we track reported a slower Q1. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 0.7% above.

Luckily, hardware & infrastructure stocks have performed well with share prices up 22.3% on average since the latest earnings results.

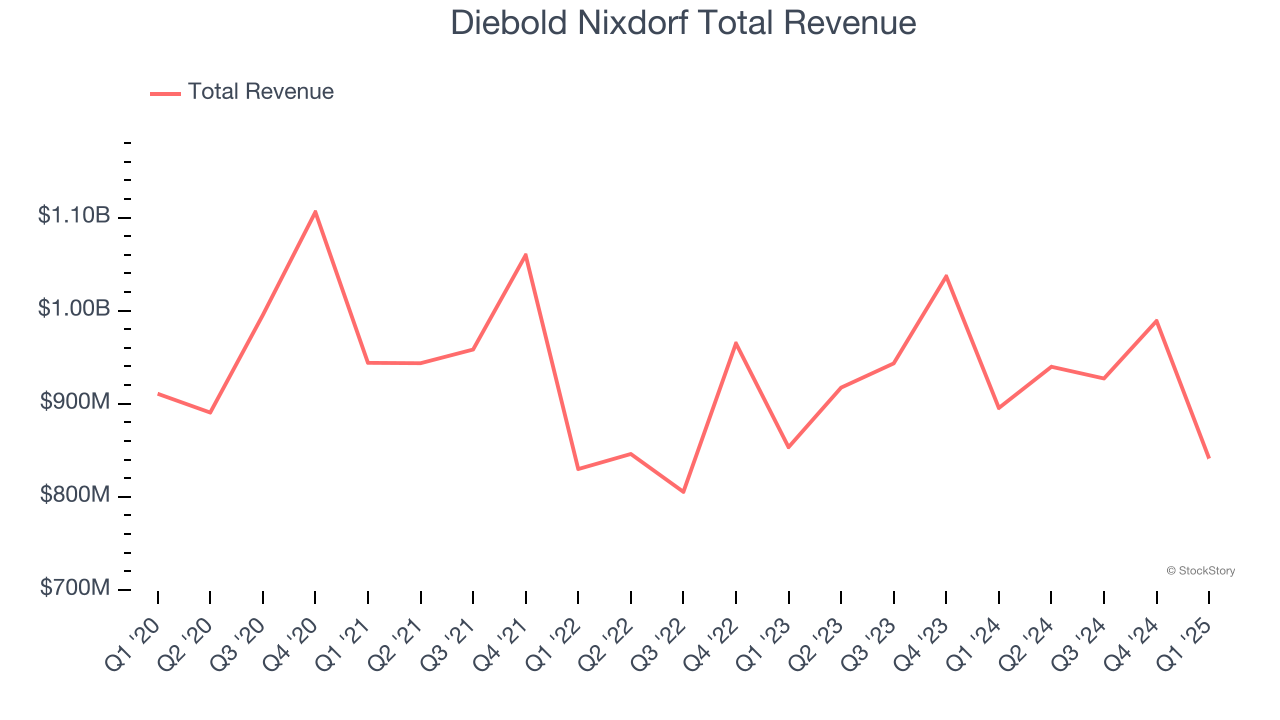

Diebold Nixdorf (NYSE: DBD)

With roots dating back to 1859 and a presence in over 100 countries, Diebold Nixdorf (NYSE: DBD) provides automated self-service technology, software, and services that help banks and retailers digitize their customer transactions.

Diebold Nixdorf reported revenues of $841.1 million, down 6.1% year on year. This print fell short of analysts’ expectations by 0.6%. Overall, it was a softer quarter for the company with a significant miss of analysts’ EPS estimates.

Diebold Nixdorf delivered the slowest revenue growth of the whole group. Interestingly, the stock is up 30% since reporting and currently trades at $59.

Read our full report on Diebold Nixdorf here, it’s free.

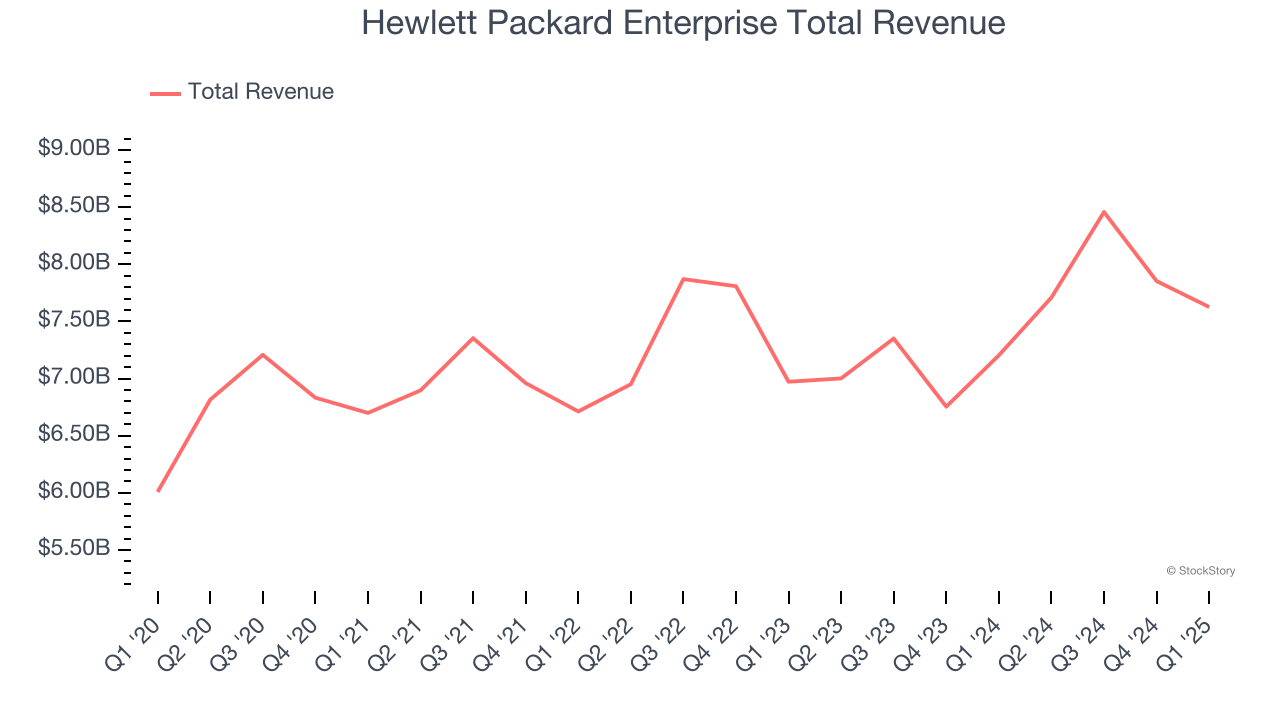

Best Q1: Hewlett Packard Enterprise (NYSE: HPE)

Born from the 2015 split of the iconic Silicon Valley pioneer Hewlett-Packard, Hewlett Packard Enterprise (NYSE: HPE) provides edge-to-cloud technology solutions that help businesses capture, analyze, and act upon their data across hybrid IT environments.

Hewlett Packard Enterprise reported revenues of $7.63 billion, up 5.9% year on year, outperforming analysts’ expectations by 2.3%. The business had a very strong quarter with an impressive beat of analysts’ ARR and EPS estimates.

Hewlett Packard Enterprise delivered the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 20.8% since reporting. It currently trades at $21.34.

Is now the time to buy Hewlett Packard Enterprise? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: HP (NYSE: HPQ)

Born from the legendary Silicon Valley garage startup founded by Bill Hewlett and Dave Packard in 1939, HP (NYSE: HPQ) designs and sells personal computers, printers, and related technology products and services to consumers, businesses, and enterprises worldwide.

HP reported revenues of $13.22 billion, up 3.3% year on year, exceeding analysts’ expectations by 0.9%. Still, it was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates.

As expected, the stock is down 4.7% since the results and currently trades at $26.

Read our full analysis of HP’s results here.

Xerox (NASDAQ: XRX)

Pioneering the modern office copier and inventing technologies like Ethernet and the laser printer, Xerox (NASDAQ: XRX) provides document management systems, printing technology, and workplace solutions to businesses of all sizes across the globe.

Xerox reported revenues of $1.46 billion, down 3% year on year. This result was in line with analysts’ expectations. However, it was a softer quarter as it recorded a significant miss of analysts’ EPS estimates.

The stock is up 33.3% since reporting and currently trades at $5.88.

Read our full, actionable report on Xerox here, it’s free.

Pure Storage (NYSE: PSTG)

Founded in 2009 as a pioneer in enterprise all-flash storage technology, Pure Storage (NYSE: PSTG) provides all-flash data storage hardware and software that helps organizations manage their data more efficiently across on-premises and cloud environments.

Pure Storage reported revenues of $778.5 million, up 12.3% year on year. This print topped analysts’ expectations by 1.1%. It was a strong quarter as it also put up a solid beat of analysts’ EPS estimates and full-year revenue guidance meeting analysts’ expectations.

The stock is up 3.3% since reporting and currently trades at $56.93.

Read our full, actionable report on Pure Storage here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.