We maintain several market timing models, each with differing time horizons. The "Ultimate Market Timing Model" is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Asset Allocation Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, "Is the trend in the global economy expansion (bullish) or contraction (bearish)?"

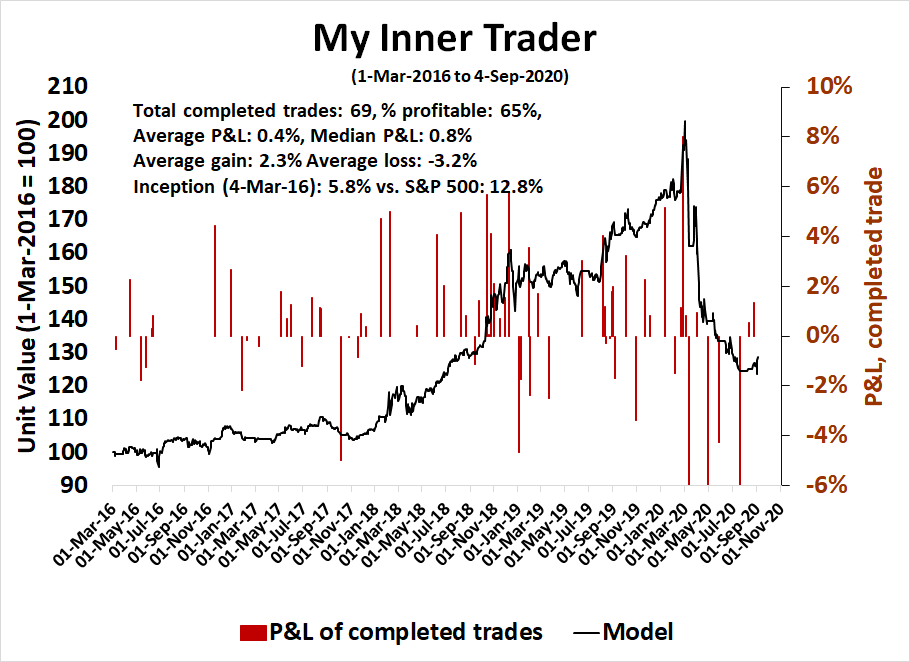

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don't buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the those email alerts are updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Sell equities*

- Trend Model signal: Neutral*

- Trading model: Bearish*

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of the those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

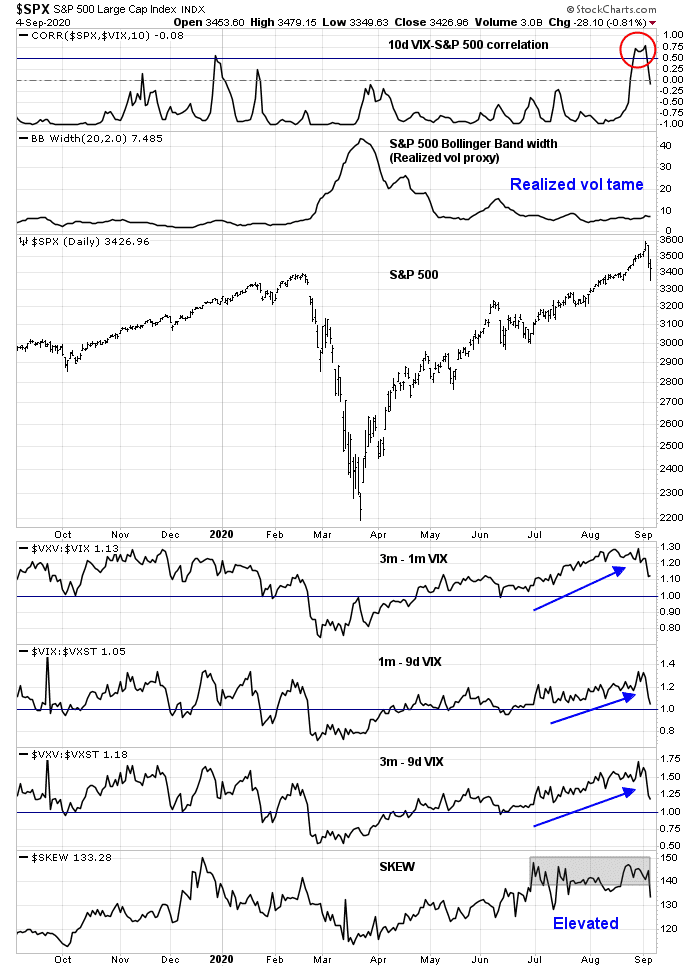

Why Are VIX and SPX Moving Together?

Something odd is happening in the equity option market.

- Until the market sold off last Thursday, the VIX and SPX had been rising together. The 10-day correlation of the VIX and SPX spiked to over 0.7, which is highly unusual as the two indices tend to be negatively correlated with each other (top panel).

- The rise in implied volatility, as measured by the VIX Index, was not matched by rising realized volatility. The second panel in the chart below shows the width of the SPX Bollinger Band as a proxy for implied volatility, which has been tame.

- Until the market sold off last Thursday, the term structure of the VIX was steeply upwards sloping. The spread between 9-day, 1-month, and 3-month implied volatility was uniformly high by historical standards.

- The SKEW Index, which measures the price of hedging tail-risk, was also elevated.

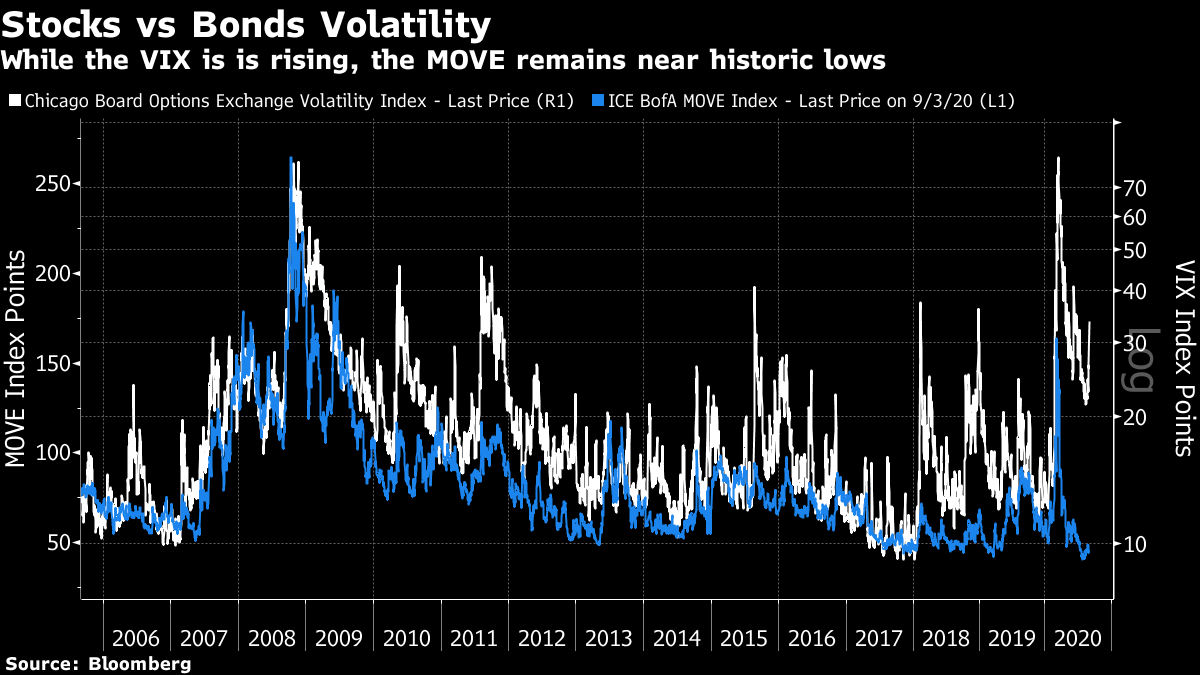

Equally puzzling is the disconnect between stock and bond implied volatility. While stock volatility has surged, bond market volatility remains tame. What's going on?

Historically, high correlations between SPX and VIX have usually led to market sell-offs. Under a minority of circumstances, they have also signaled market melt-ups. How can we explain these unusual conditions in the option market?

The full post can be found here.