We maintain several market timing models, each with differing time horizons. The "Ultimate Market Timing Model" is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Asset Allocation Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, "Is the trend in the global economy expansion (bullish) or contraction (bearish)?"

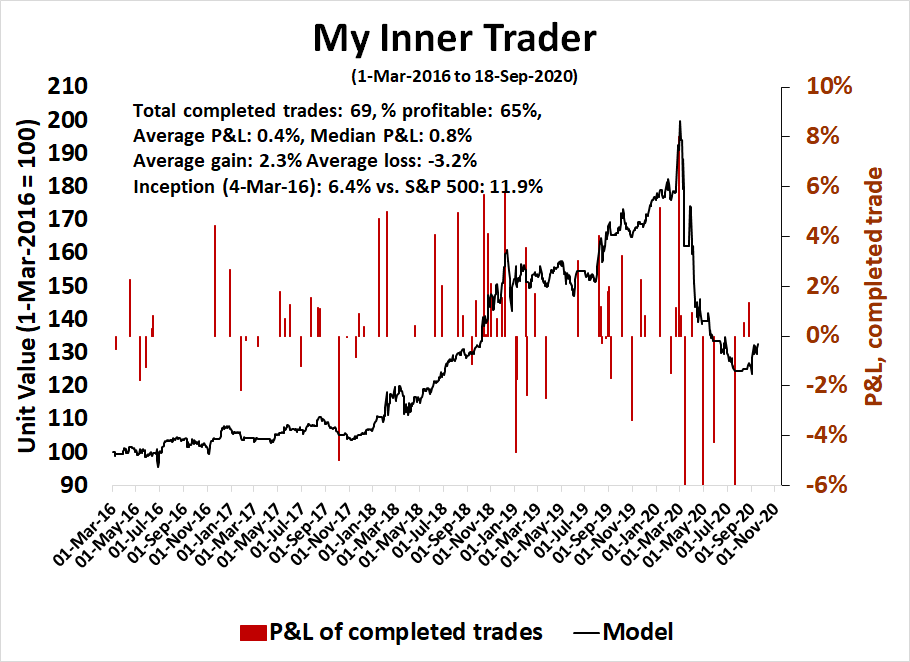

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don't buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the those email alerts are updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Sell equities*

- Trend Model signal: Neutral*

- Trading model: Bearish*

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of the those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

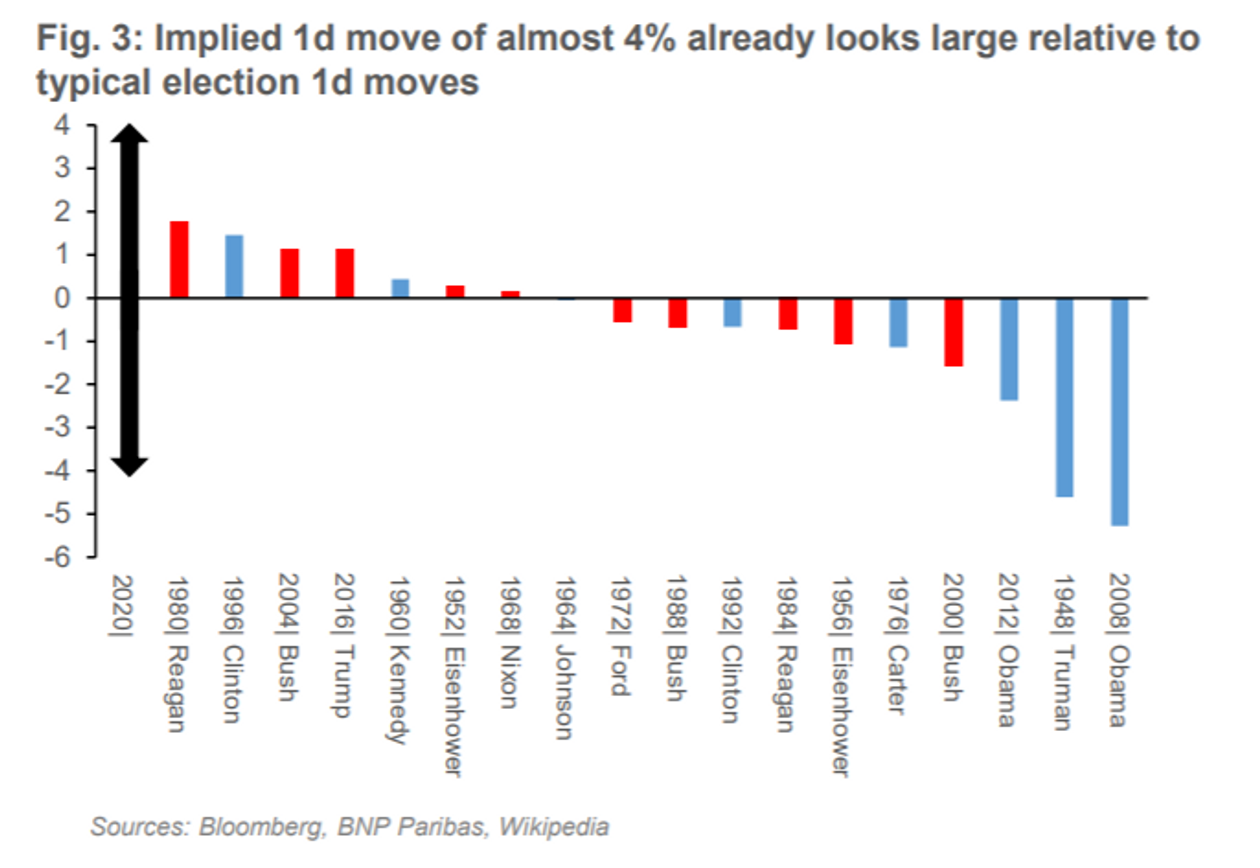

More election volatilityWhile I am not a volatility trader, my recent calls on the evolution of volatility have been on the mark. Three weeks ago, I raised the possibility of a volatility storm (see Volmageddon, or market melt-up?) owing to rising election jitters. I concluded "I would estimate a two-thirds probability of a correction, and one-third probability of a melt-up, but I am keeping an open mind as to the ultimate outcome". Two weeks ago, I turned more definitive about rising volatility and called for a volatility storm (see Brace for the volatility storm).

The rising election induced volatility theme has become increasingly mainstream in the financial press. Bloomberg highlighted that the one and three month spread in the MOVE Index, which measures bond market volatility, is spiking.

Marketwatch also reported that analysis from BNP Paribas shows that the implied equity market volatility over the election window is sky high compared to past realized returns of election results.

In addition, all these option readings were taken before the news about the death of Supreme Court Justice Ruth Bader Ginsburg. Should the election results be contested and wind up in the Supreme Court, the odds of a 4-4 deadlocked decision just rose with Ginburg's death, in which case the lower court's decision would stand. This raises the odds of judicial and constitutional chaos. Imagine different states with wildly inconsistent decisions on balloting. The Supreme Court nomination fight also raises the political resolve of both sides in Congress. Don't expect any stimulus bill before the election, and even a Continuing Resolution to fund the federal government beyond September 30 is in jeopardy. Watch for implied volatility to rise in the coming week.

It seems that the bears have taken control of the tape, based on a combination of election uncertainty and a reversal of excessive bullish retail positioning on Big Tech stocks.

The full post can be found here.