We’ve seen an impressive recovery since the pre-election lows for the major market averages, with the S&P-500 (SPY) up over 10% and the Nasdaq 100 (QQQ) up roughly 9% as of Wednesday’s close. However, most of the performance post-election has come from the more cyclical sectors, while stay-at-home stocks have taken a beating following the vaccine news.

The good news is that this shift from growth to value has left a few tech stocks trading at reasonable valuations, and two names are sporting industry-leading growth. In this article, we’ll cover two names that should be at the top of one’s shopping list if we do get a sharp correction in the general market. Let’s take a closer look below:

(Source: TC2000.com)

Snap Inc. (SNAP) and Netflix (NFLX) have little in common as they both hail from different industries within the vast tech sector, but both companies do share one trait: massive earnings growth. In SNAP’s case, the company just came off a blow-out Q3 report with average revenue per user [ARPU] coming in 20% above estimates at $2.73, and average daily users now sitting just shy of 249 million. This translated to 18% growth year-over-year in daily active users, suggesting that the adoption of the popular camera App is nowhere near over.

On the more critical headline numbers, revenue grew an incredible 52% year-over-year, translating to a 3500-basis point improvement sequentially (52% vs. 17%), and gross margin jumped 700 basis points year-over-year to 58%. These outstanding results were driven by increased spend from advertising partners, and media companies continue to see significant traction moving shows to Snapchat. On a monthly basis, over 50 million users are watching TV content on the platform each month. Given this sharp increase in gross margins and revenue, it’s looking like we’ll see a move to profitability much quicker than expected.

(Source: YCharts.com, Author’s Chart)

As shown in the earnings trend above, SNAP has been posting net losses for years now, but this is expected to change dramatically in FY2021. Following the most recent earnings report, FY2021 EPS estimates have jumped from $0.04 to $0.16, and FY2021 annual EPS estimates have jumped from $0.32 to $0.62.

This is a massive improvement in the earnings trend, and it gives SNAP the title of top-100 growth stock based on its FY2022 growth rate of 285% if these annual EPS estimates hold. While the stock might look expensive at nearly 300x FY2021 annual EPS estimates, it’s worth noting that this estimate is quite stale and less important, with almost 300% growth expected the following year. In fact, if we compare the current share price of $41.00 to FY2022 estimates, the stock is trading at just over 65x earnings, which isn’t that unreasonable for a less mature growth name.

(Source: TC2000.com)

If we look at SNAP’s technical picture, we can see that the stock just blasted out of a multi-year base on record buying volume, and base breakouts of this size rarely fizzle out after a few months. In fact, this breakout is projecting a move above $55.00, assuming it's successful.

Judging by the strength of the breakout, I would be shocked if this ended up being a failed yearly breakout. While this doesn’t mean that SNAP can’t pull back over the next few weeks to digest its gains, I expect funds that accumulated the stock on the breakout to defend their positions on any further weakness. Therefore, if we were to see a pullback below $36.75, I believe this would be a low-risk buying opportunity.

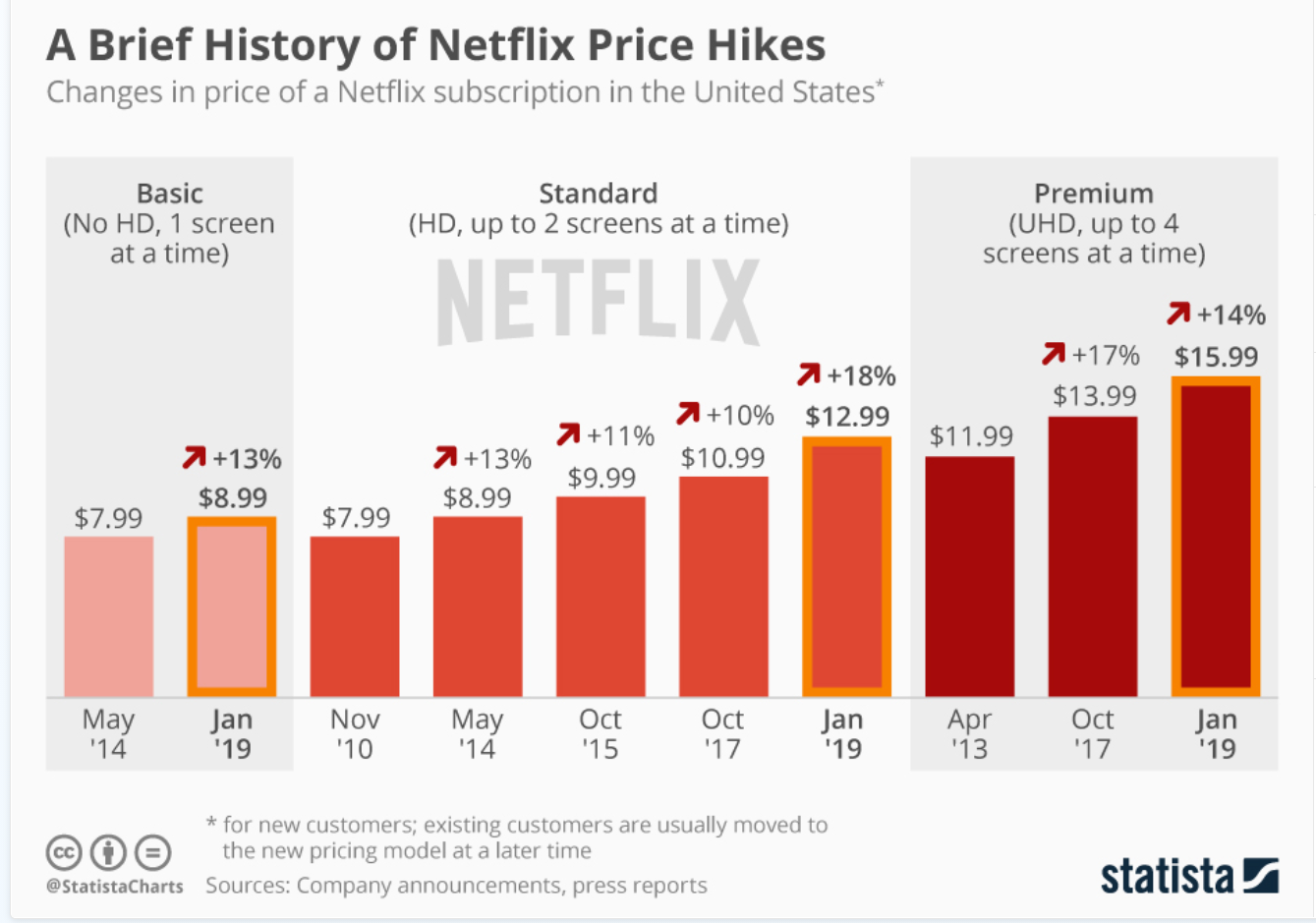

(Source: Statista.com)

Moving over to Netflix, the company is rarely thought of as a growth company, and it’s endured its share of criticism over the years over both price hikes, questionable shows, and its inability to continue its subscriber growth. However, despite all the naysayers, the company has continued to show it has strong pricing power with successful price hikes for years now while maintaining its massive subscriber base. This has allowed the company to maintain its strong margins and massive recurring revenue base.

In a world where there’s so little going on outside, given that many have anxiety about going out, NFLX is a staple for so many households. While the latter point is merely conjecture, I see no reason for investors to write off NFLX as a growth name. This is because the company is one of the only large-cap tech names set to double its annual EPS in the next two years. Meanwhile, given that the stock has been consolidating for months, the valuation is actually very reasonable. Let’s take a closer look:

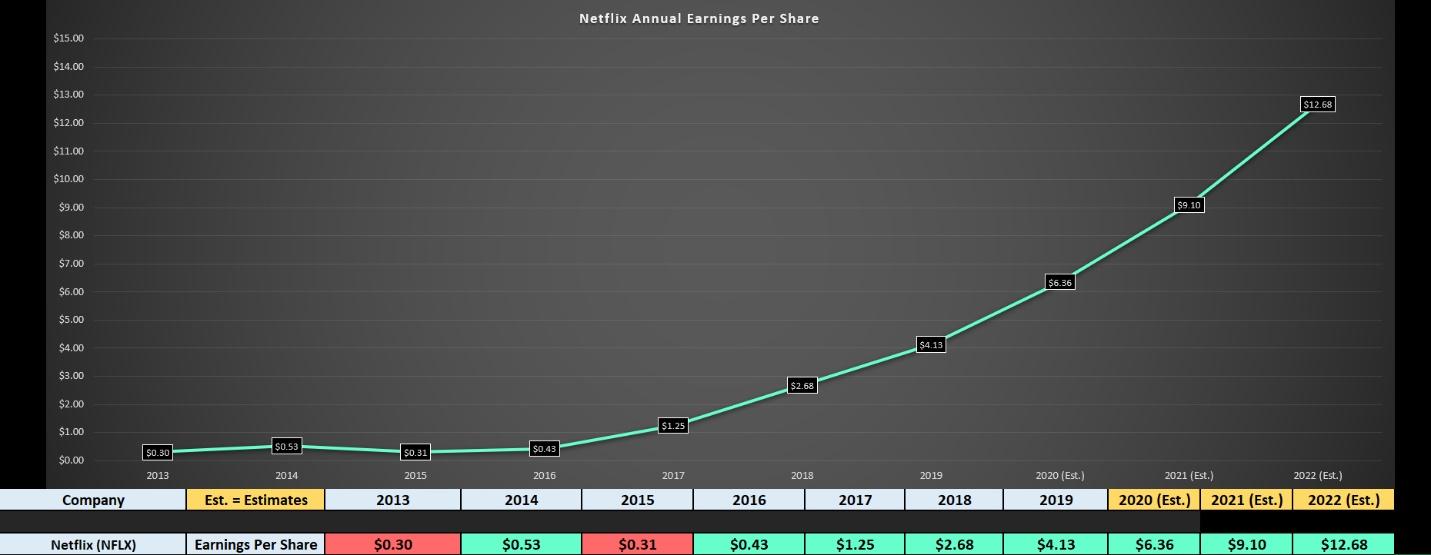

(Source: YCharts.com, Author’s Chart)

As shown in the chart above, NFLX has seen exponential growth in annual EPS since FY2013, with annual EPS up over 1000% from $0.30 to $4.13. The company is on track to grow annual EPS by over 50% in FY2020 from $4.13 to $6.36, and FY2022 annual EPS estimates have continued to rise following the pandemic.

Currently, FY2022 estimates are sitting at $12.68, which suggests that NFLX could double its annual EPS again even as a mega-cap tech company. This combination of a unique product/service and commanding lead vs. its peers, as well as double-digit earnings growth and a compound annual EPS growth rate of over 20%, makes NFLX a must-own for long-term investors. Besides, it’s not every day you get to buy the stock at barely 75x next year’s earnings.

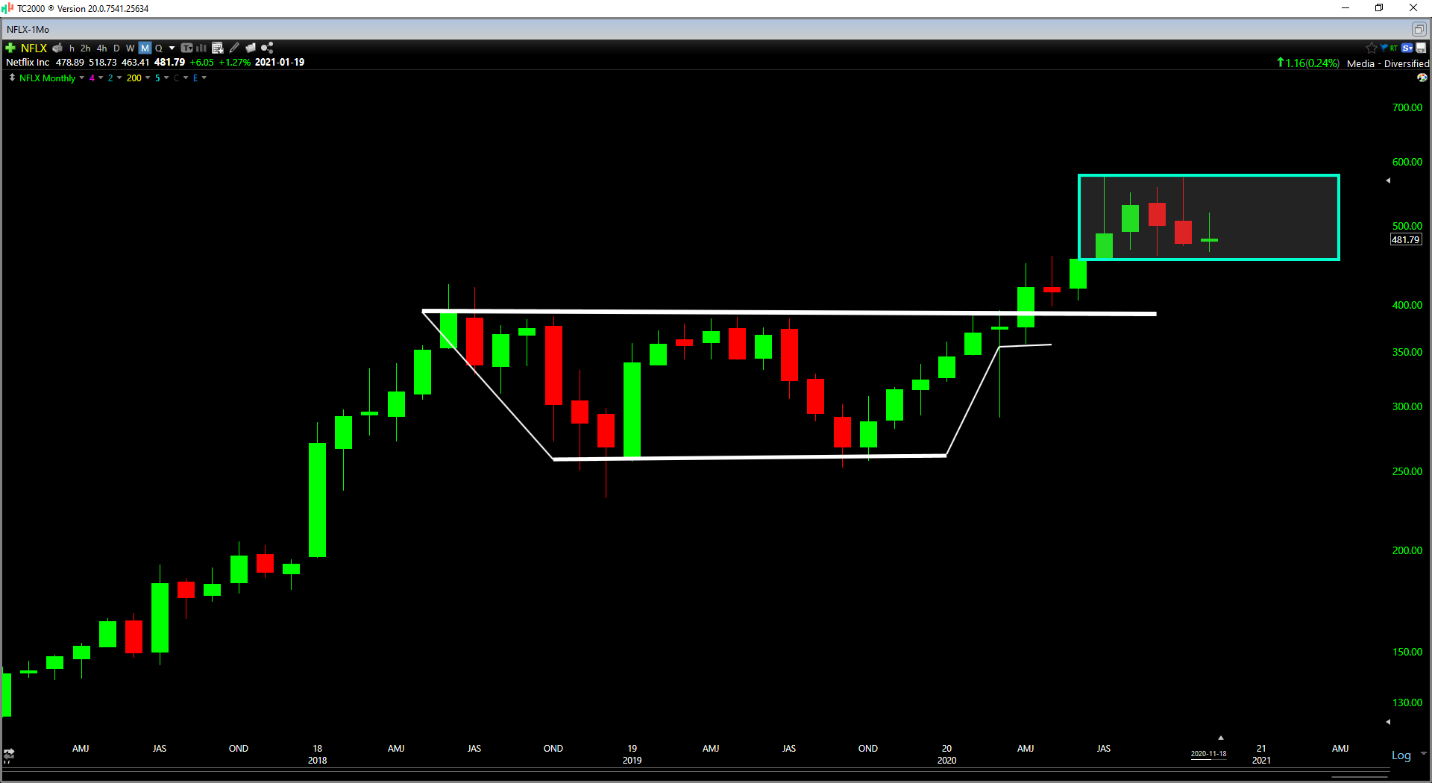

(Source: TC2000.com)

Some investors might argue that the best days for NFLX are over, but big money seems to disagree as the stock broke out of a massive base earlier this year and is now enduring its first correction since this breakout. While there’s no guarantee that this breakout resolves to the upside, this is setting up a low-risk buy point for investors against the bottom of this base near $460.00.

Therefore, for investors who own the stock from lower, I believe any pullbacks below $450.00 would be a low-risk add point. This would be a shake-out from this base that might scare off weak hands, but it would do zero damage to the big picture, as we see above. In fact, I would consider any pullbacks to be noise as long as they hold above the $400.00 level on a monthly close. Given NFLX’s strong technicals and fundamental picture, I continue to remain bullish on the stock.

While the market is quite overbought short-term, and there’s not much value out there with the S&P-500 trading at its lowest yield in nearly a decade, I believe there is still lots of value left in SNAP and NFLX. In NFLX’s case, the recent consolidation has allowed the valuation to improve considerably, and this is still a growth story in its middle innings with international potential.

In SNAP’s case, the company’s shift to profitability is just getting started, and the stock is set to be a top-100 growth stock for FY2022 based on 250%+ annual EPS growth. Therefore, if we see a correction in NFLX below $455.00 or SNAP below $37.00, I would expect this to be a buying opportunity. For now, I continue to hold NFLX but have no position in SNAP yet.

Disclosure: I am long NFLX

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

Why Investors DON’T Care About Covid-19 Anymore

5 WINNING Stocks Chart Patterns

SNAP shares were trading at $40.47 per share on Thursday morning, down $0.16 (-0.39%). Year-to-date, SNAP has gained 147.83%, versus a 12.21% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 2 Tech Stocks With Massive Growth Potential to Buy on Weakness appeared first on StockNews.com