We maintain several market timing models, each with differing time horizons. The "Ultimate Market Timing Model" is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Asset Allocation Model is an asset allocation model that applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, "Is the trend in the global economy expansion (bullish) or contraction (bearish)?"

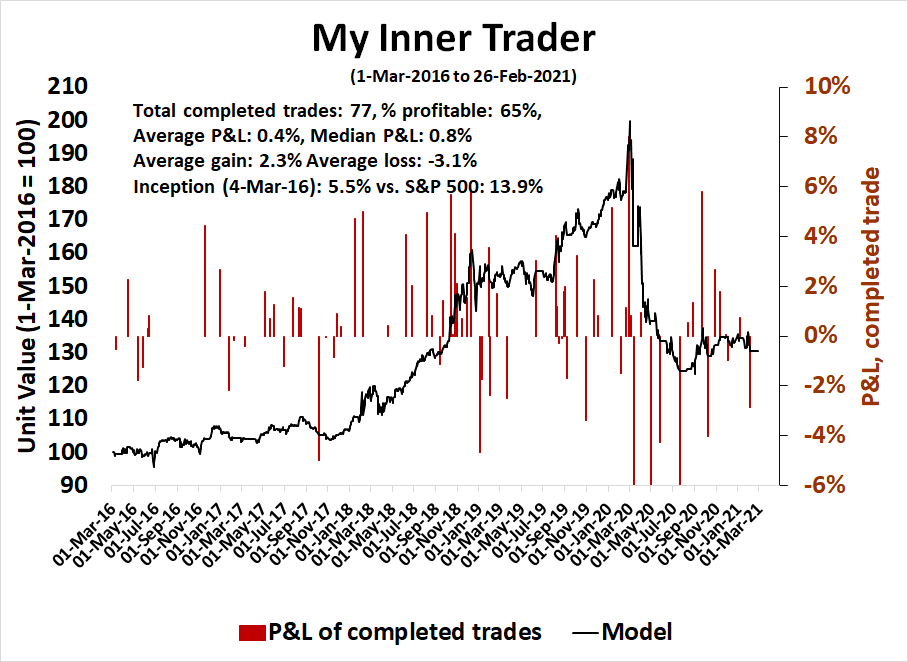

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don't buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts are updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities*

- Trend Model signal: Bullish*

- Trading model: Bullish*

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

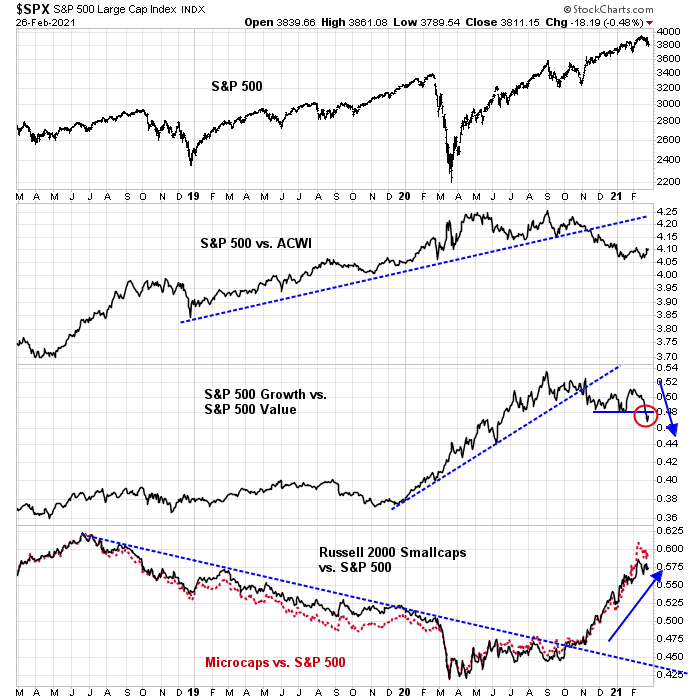

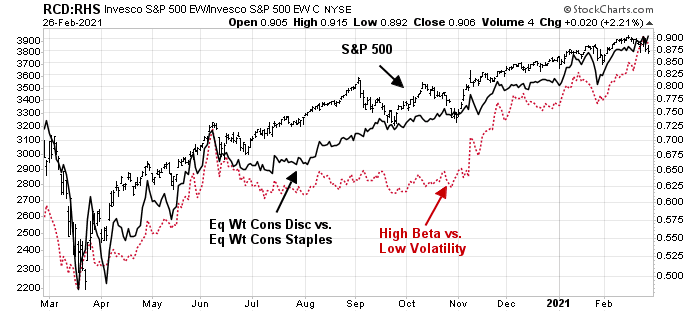

More signs of a Great RotationThe leadership of the last market cycle was dominated by three main themes, the US over global equities, growth over value, and large-caps over small-caps. Leadership began to change in 2020. Small-cap stocks broke their relative downtrend first. November's Vaccine Monday, when Pfizer announced its positive vaccine results, sparked a shift in the other two factors.

Since then, small-cap stocks have roared ahead against their large-cap counterparts. Last week saw another confirmation of the Great Rotation when value/growth relationship broke a key relative support level.

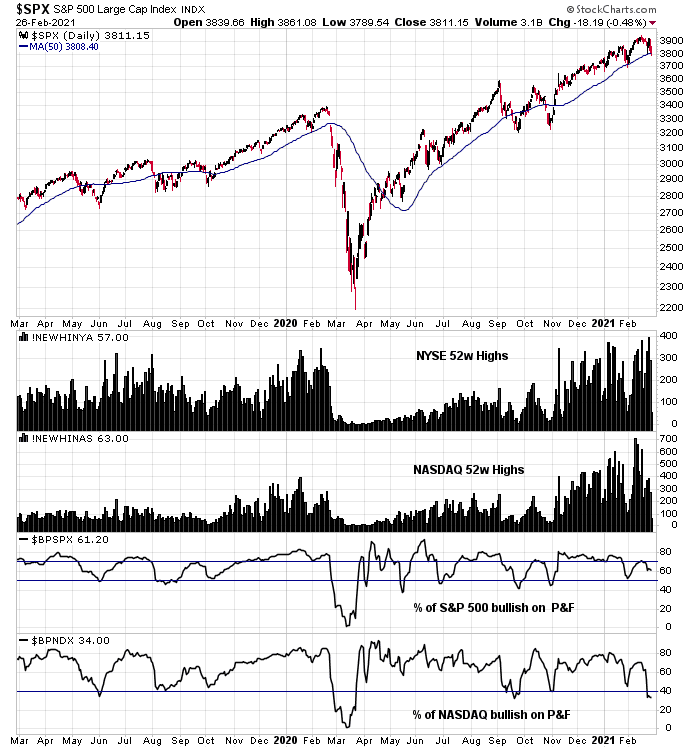

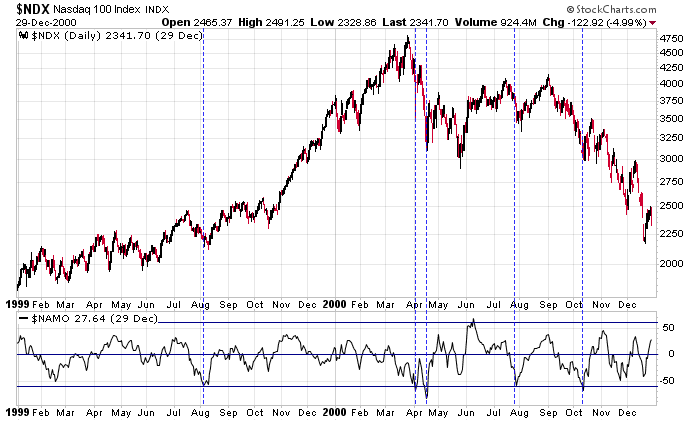

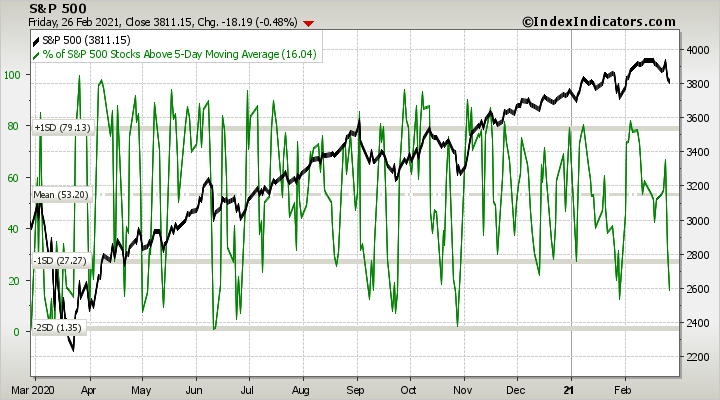

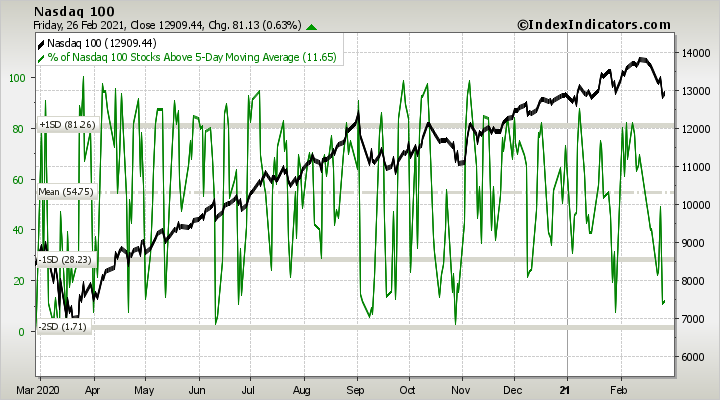

A great gulfA great gulf has appeared between the market internals of the high-flying growth names, as represented by the NASDAQ 100, and the broadly-based market. Even as the S&P 500 weakened to test its 50-day moving average (dma), NYSE 52-week highs held up well until Friday while NASDAQ highs deteriorated. As well, the percentage of S&P 500 on point and figure buy signals staged a mild retreat, while the similar indicator for NASDAQ stocks fell to oversold levels.

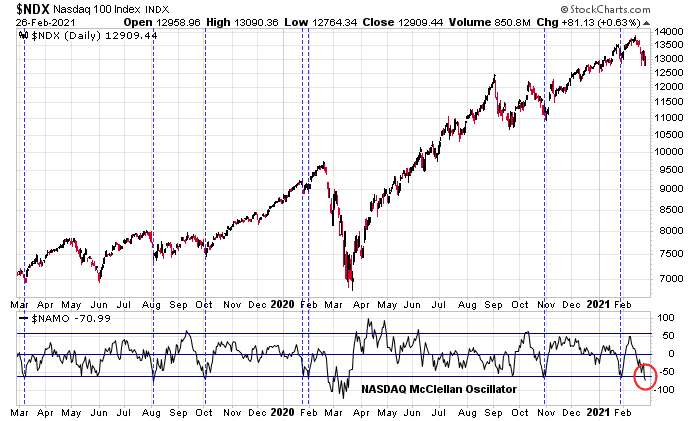

The NASDAQ McClellan Oscillator (NAMO), which became near overbought in early February, has retreated to an oversold extreme.

For some context, here is how the NASDAQ 100 and NAMO behaved during the period leading up to and after the dot-com top of 2000, which is as bad as growth stock got. Oversold conditions in the bull market of 1999 were intermediate-term buy signals, while oversold conditions in the bear market that began in 2000 were tactical buy signals that only resolved in short-term rallies, but the index did bounce.

In light of the change in leadership from growth to value, expect the latter scenario of short-term tactical rallies to be in play.

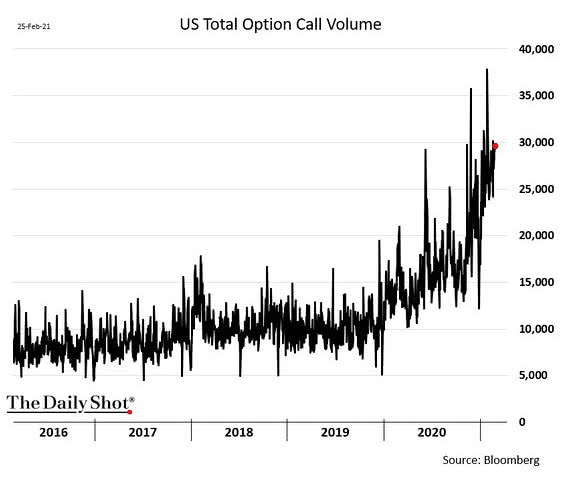

Waiting for a small investor shakeoutWhile these readings argue for a tactical relief rally, I don't think the bottom is here just yet because the retail investor remains overly exuberant. Standard indicators of equity risk appetite don't work well in this environment because the market is undergoing an internal rotation from growth to value.

We need to see the inexperienced Robinhood investor crowd to become washed out, which has not happened so far. Call option volumes are still rising in a parabolic way. I am reminded of Bob Farrell's Rule #4: "Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways."

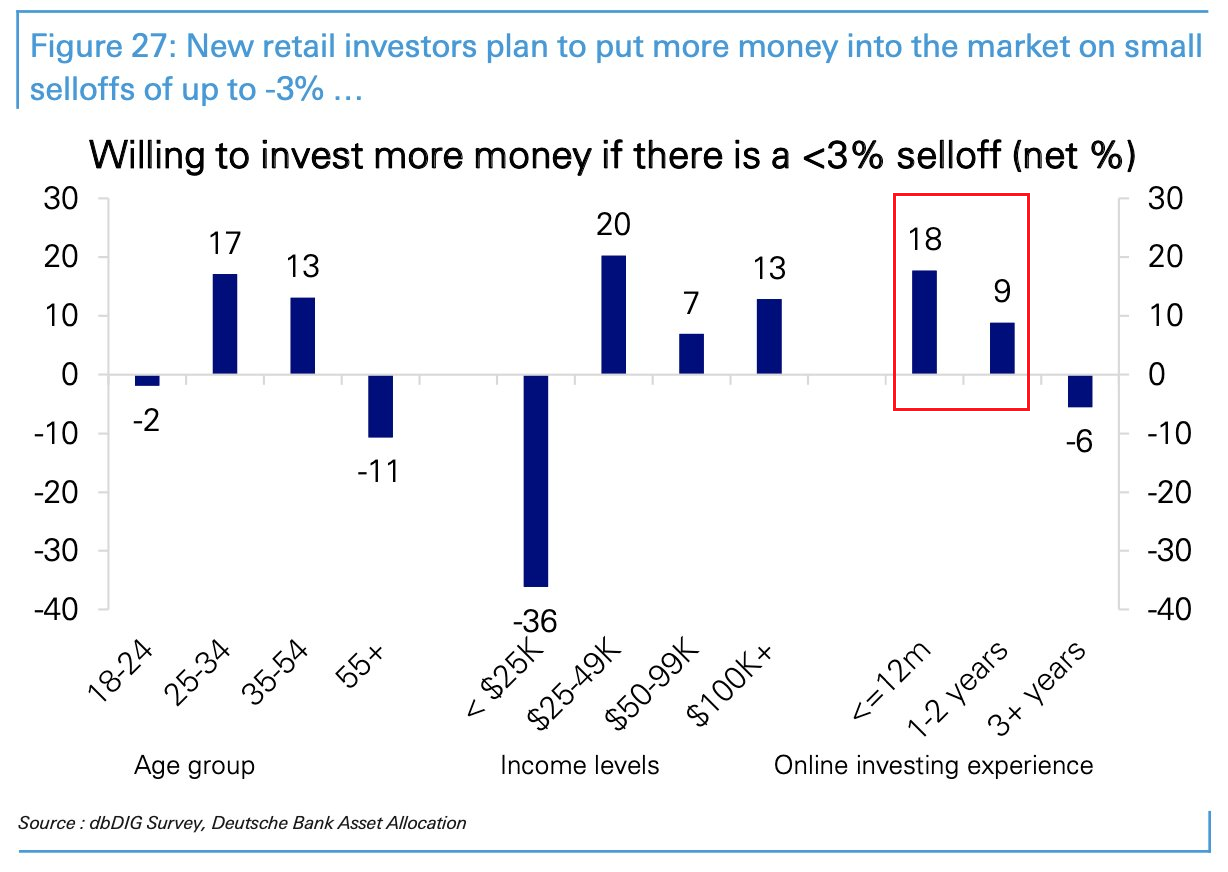

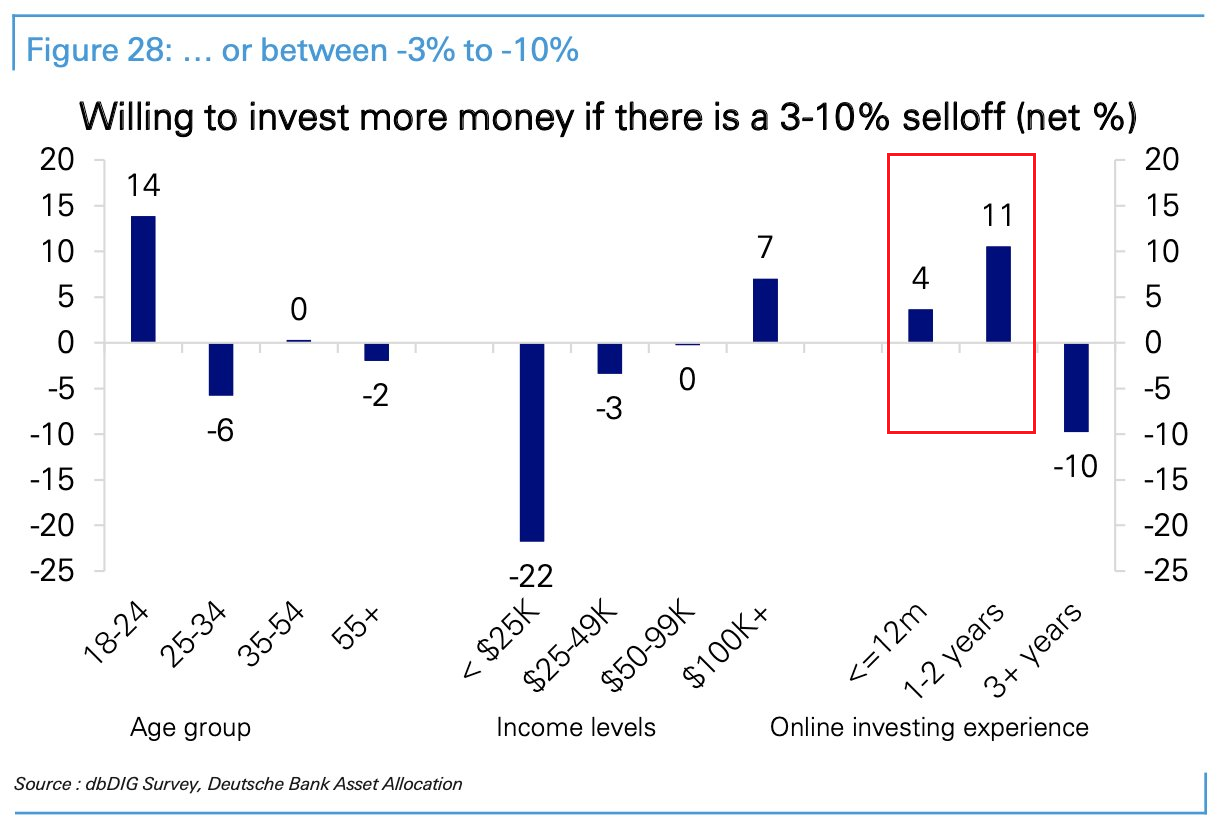

Deutsche Bank conducted a survey of retail investors, and there is a remarkable difference in bullishness between the Boomers and their younger counterparts. More remarkably, bullishness is concentrated in the least experienced group.

In a raging bull, it takes a kid with no fear. But this new cohort will learn their lessons about risk when the market turns. When asked if they are willing to buy a dip of 3% or less, investors with less than two years of experience were willing to step into the breach.

The least experienced investors were less enthusiastic when the pullback deepens to 3-10%.

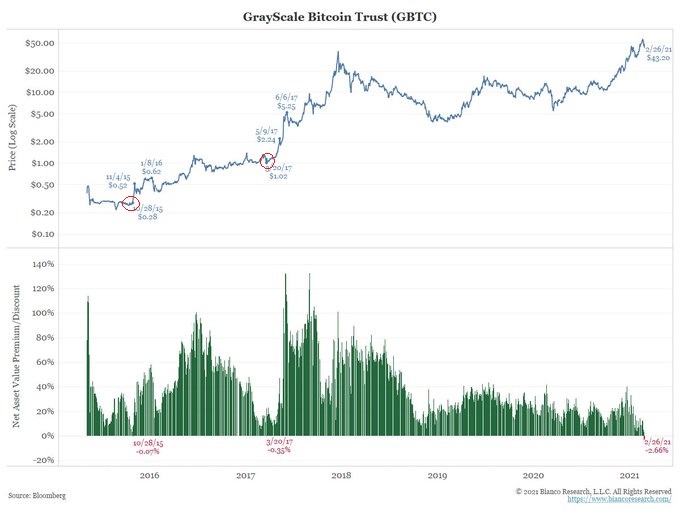

One risk appetite indicator reflective of this Robinhood crowd that I am monitoring is Bitcoin (BTC). The returns of BTC have been highly correlated with the relative returns of the high-flying ARK Innovation ETF (ARKK) relative to the S&P 500.

Jim Bianco observed that the "biggest Bitcoin Fund, Grayscale $GBTC, is trading at a discount for only the 3rd time ever, and its largest." Is this a buy signal, as it has been in the past, or the start of a significant risk-off episode?

The 56-week pattern in play?Where does that leave us? I wrote about an intriguing analysis by Gordon Scott about the 56-week pattern in early December (see Melt-up, or meltdown?).Here is how it works: any time the S&P 500 index (SPX) rises more than five percent within a 20-session stretch, 56-weeks later there is often a sell-off of varying proportions. This happens consistently enough that if you track through the data, you can calculate that the average return for the 40-day period at the end of 56 weeks is almost a full one percent lower than the average return for any other 40-day period over the past 26 years. The reason for bringing it up now is that, as shown in the chart below, the recent pullback came at the beginning of such a pattern. Even more interesting is that three more ending patterns are due to create selling in close proximity during the second quarter of 2021. The 56-week pattern has a simple explanation. To take advantage of favorable tax treatment, many high-net worth investors and professional money managers prefer to hold positions longer than one year. What that means is that if a lot of them buy at the same time, it shows up in the market averages. A little more than a year later, there comes a point where a lot of money is ready to be taken out of one position and moved into another.

Tactically, the market may stage a relief rally in the coming days. Both the S&P 500 and NASDAQ 100 are highly oversold and due for a bounce early in the week.

As well, NYMO has also flashed an oversold reading as the S&P 500 tests its 50 dma.

But don't be fooled by any rally. We are in need of a small investor sentiment washout that hasn't happened yet. These conditions argue for a period of choppiness and growth to value rotation in the coming weeks.

Disclosure: Long TQQQ