Stocks are trading at some of the highest valuations in history. According to the Buffett Indicator, which compares total U.S. stock market capitalization to GDP, valuations sit at roughly 217%. That’s well above the 150% peak reached during the dot-com bubble.

Other metrics confirm the froth. The S&P 500 Index ($SPX) price-book ratio recently hit 5.46x, the highest on record and nearly double its long-term median. Meanwhile, Bank of America now flags the market as “statistically expensive” across all 20 of its tracked valuation metrics — a clean sweep that hasn’t occurred in decades. The firm also reports that 60% of its bear-market signposts are currently triggered, which is worryingly close to the 70% level that has marked previous market peaks.

Michael Burry has taken notice. The investor who famously shorted the housing market in 2008 has returned with a bold new position. His latest 13F filing from now-deregistered Scion Asset Management revealed significant put option exposure to Nvidia (NVDA) and Palantir (PLTR), two of the most visible players in the AI-driven rally that was originally catalyzed by the introduction of ChatGPT in late 2022.

And Burry’s not the only one raising a red flag.

Late last year, the European Central Bank warned that growing concentration in U.S. mega-cap tech stocks — particularly those tied to artificial intelligence — could pose structural risks.

Warren Buffett has continued trimming equity exposure while building a record $381 billion in cash. And Ray Dalio, the billionaire founder of Bridgewater and a widely followed market pundit, believes the rally is becoming overextended and increasingly vulnerable to a sharp correction.

In early November, Dalio suggested that the Federal Reserve’s shift toward easier monetary policy could fuel a short-term “liquidity melt-up” — a final burst of euphoria that inflates valuations before sentiment turns. “It would be reasonable to expect that, similar to late 1999 or 2010-2011, there would be a strong liquidity melt-up that will eventually become too risky and will have to be restrained,” Dalio told Business Insider. “During that melt-up… is classically the ideal time to sell.”

A Closer Look at Michael Burry’s Bet Against AI Stocks

Circling back to Michael Burry, his latest 13F filing offers a rare glimpse into how one of the market’s most contrarian investors is preparing for a potential pullback.

After warning about stretched valuations in broad terms, Burry went straight to the heart of the AI trade by loading up on put options tied to Nvidia and Palantir, two of the most visible and richly valued names in the space.

According to Scion Asset Management’s most recent filing, the firm held put options covering 1 million shares of NVDA and 5 million shares of PLTR. On paper, those positions totaled $186.6 million and $912.1 million, respectively.

But these headline numbers can be misleading. SEC rules require funds to report options using notional value, which is the number of shares controlled multiplied by the stock price, not the premium paid.

That means a single put on a $100 stock would show up as $10,000 of exposure, even though the premium paid could be significantly less. So while Burry’s filing reports more than $1.1 billion in notional exposure, the actual capital committed was almost certainly much lower. Based on standard contract sizes, the trades likely involved around 50,000 puts on Palantir and 10,000 on Nvidia. That’s a sizable footprint, and suggests targeted short positioning.

However, there’s still a lot we don’t know. The filing doesn’t include strike prices, expiration dates, or details about whether these are standalone puts or part of a multi-leg strategy. There’s also no indication of long or short positions in the underlying stocks, which suggests Scion is using the options as a pure directional bet rather than pairing them with a stock hedge.

While we don’t know the strike prices or expiration dates on these trades, it seems likely Burry wasn’t expecting them to pay off immediately. Much like his bet against the housing market during the Great Recession, a slow-burn thesis feels more consistent with his style.

The timing of the 13F filing is also unusual. Scion submitted it two weeks ahead of the deadline. Whether that was intentional or not, the message was clear. Burry wants the market to know he is betting against AI.

For investors and traders who share that concern, or are simply looking for pockets where valuations may have outpaced fundamentals, we’ve outlined two additional names worth considering.

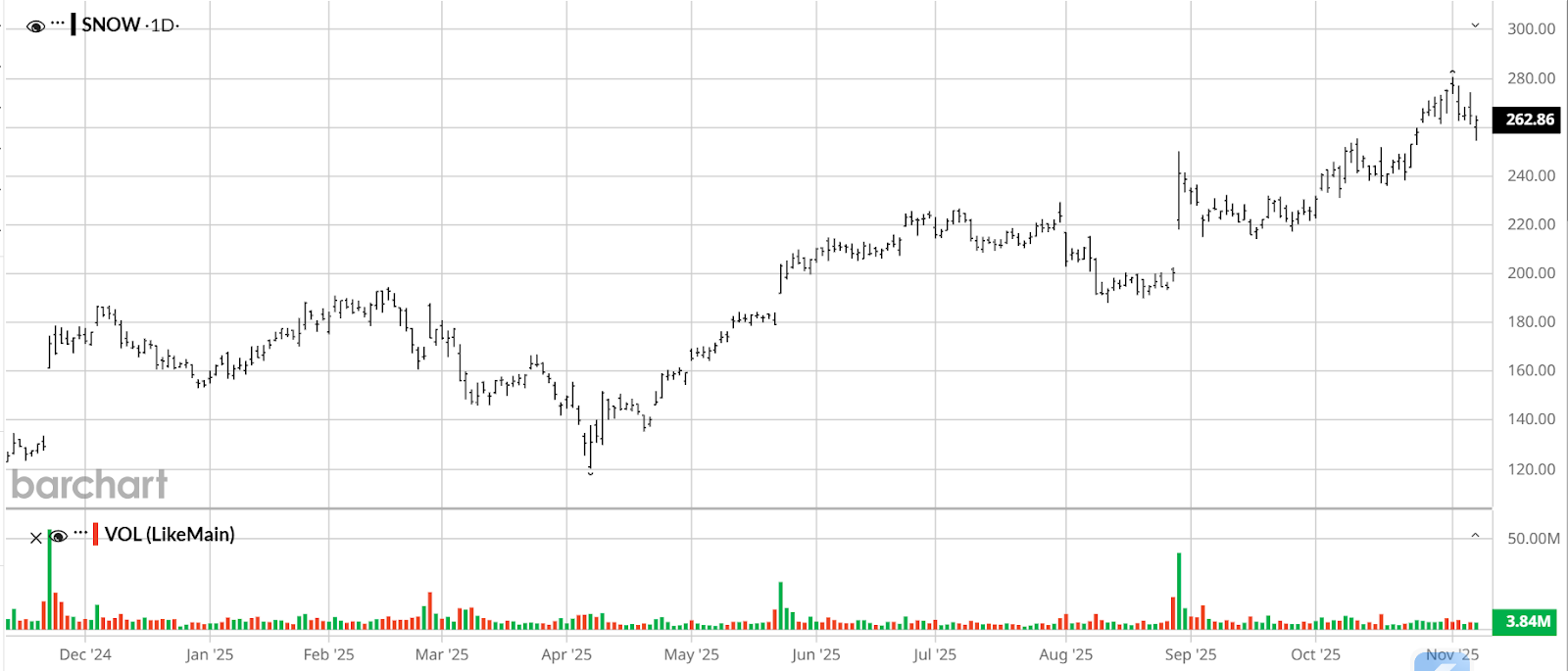

Snowflake: A Palantir Proxy with Weaker Fundamentals

For traders who share Michael Burry’s concern that the AI-fueled rally may be getting ahead of itself, Snowflake (SNOW) presents a compelling, if less spotlighted, alternative to high-profile shorts like Nvidia or Palantir.

Unlike those two companies, which are both profitable and expanding rapidly in their respective domains, Snowflake continues to post losses and burn cash while also trading at valuation levels that are difficult to justify. On top of that, the stock has surged nearly 100% over the past 12 months.

Since Snowflake went public in 2020, it has never reported a quarterly GAAP profit. And free cash flow (FCF) trends remain inconsistent. Of the last six quarters, three were negative, including a recent outflow of $359 million in the most recent quarter. Despite impressive revenue growth, that means questions about spending discipline and operational leverage continue to weigh on the outlook.

The valuation only adds to those concerns. Snowflake has operated at a loss every quarter since its IPO in 2020, yet still trades at levels that are difficult to justify. Its price-sales (P/S) ratio is over 25x, and price-book (P/B) is near 39x, both far exceeding sector norms. Since the company has never posted positive net income, a price-earnings (P/E) ratio can’t even be calculated, highlighting just how disconnected the stock is from traditional profitability metrics.

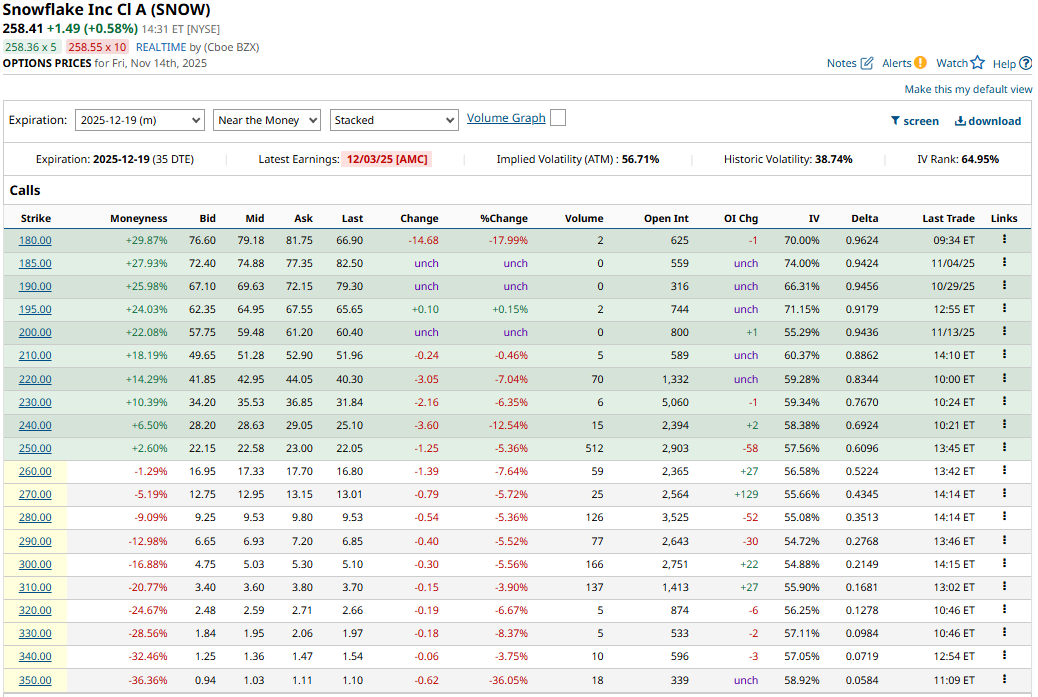

In terms of short positioning, the options on Snowflake aren’t exactly cheap. December monthly contracts reflect an implied volatility of roughly 57%, with an associated implied volatility rank (IV Rank) around 65%. IV Rank compares current implied volatility to its range over the past year. A reading above 50% means option prices are on the higher end of that 12-month range, while a lower IV Rank suggests they’re relatively inexpensive.

Options traders often scan for lower IV Ranks when looking to buy options, particularly puts designed to express a short thesis. Elevated IV makes it harder to achieve favorable risk-reward, especially if the move takes time to play out. But in today’s market, most AI-related names have experienced extended run-ups, and that makes finding “cheap” options across the sector a tall order.

And with Snowflake, there are several other factors to consider. The company operates in the same enterprise data and analytics space as Palantir, offering some thematic overlap without the same brand recognition or loyal investor base that may help names like NVDA and PLTR withstand short-term selling pressure.

Unlike Palantir, which generates a large portion of its revenue from long-term government contracts, Snowflake’s public-sector exposure is more narrow in comparison. That leaves it more dependent on commercial spending cycles and overall sentiment in the tech sector. Considering its ongoing losses, uneven cash flow, and sharp 12-month rally, Snowflake therefore stands out as a compelling candidate for traders looking to fade the AI hype.

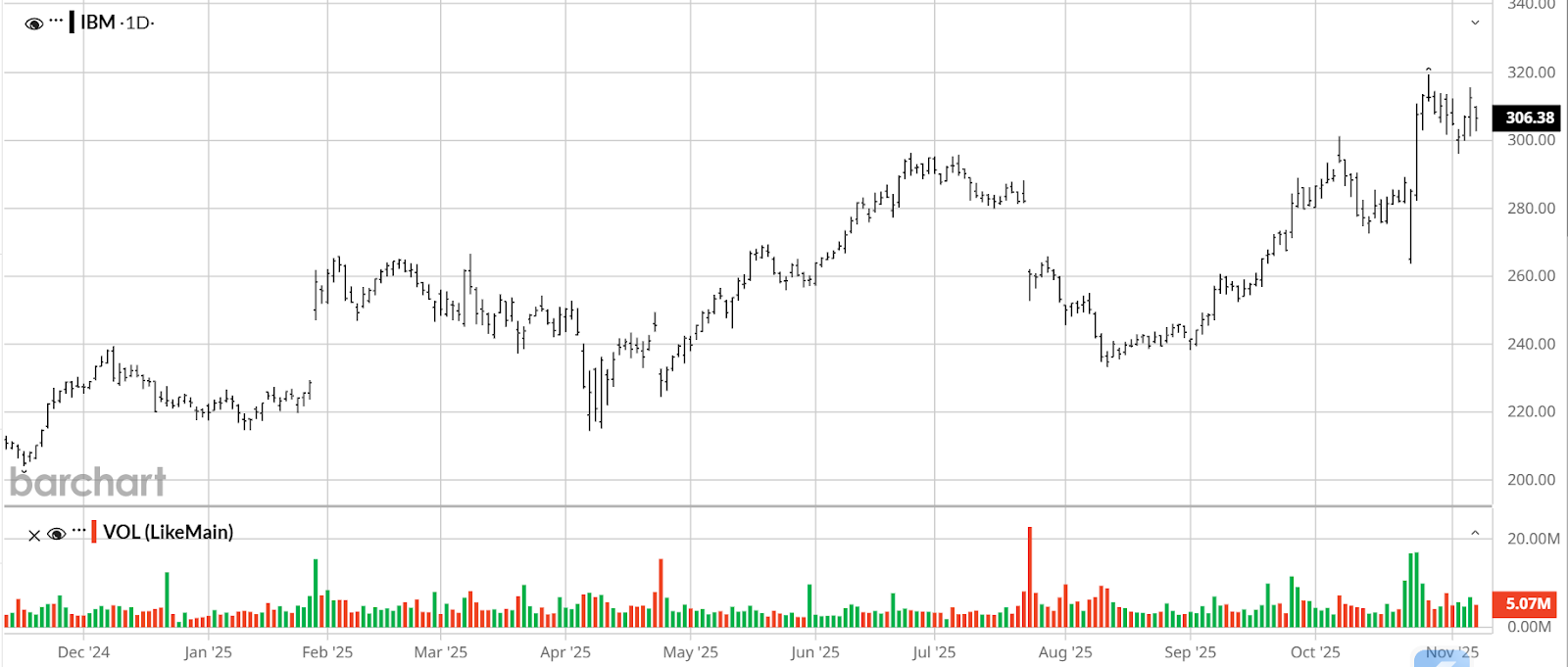

IBM: Strong Rally, Low IV Rank Create a Potential Short Opportunity

For those looking for a bearish AI trade where options are priced more attractively, International Business Machines (IBM) stands out as a potential candidate. The stock has quietly surged nearly 46% over the past 12 months, an impressive run for a traditionally slower-moving name.

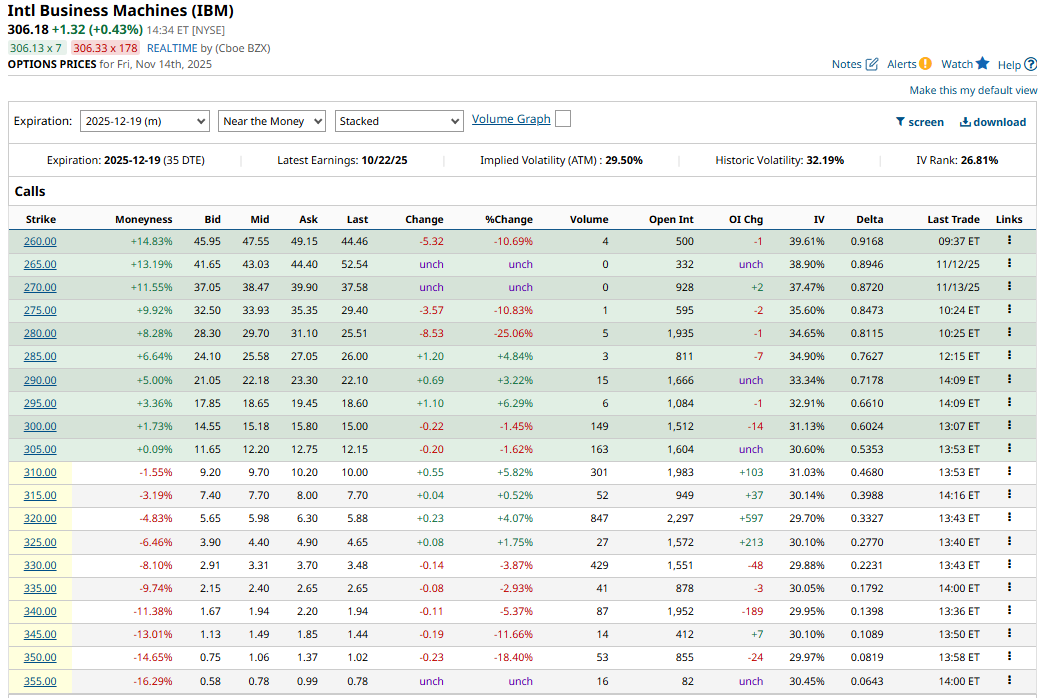

Yet despite that rally, option premiums remain surprisingly restrained, with December monthly contracts showing an IV Rank of just 27%. That’s well below the 50% level that some traders use to differentiate between high and low implied trading opportunities.

As mentioned earlier, IV Rank compares current implied volatility to its range over the past year. A lower IV Rank typically means options are trading near the lower end of that range, which can be more favorable for buyers than for sellers. In IBM’s case, historical volatility sits at 32.2%, while current implied volatility is around 30%. That close alignment suggests option prices aren’t significantly inflated relative to realized movement, which adds to the appeal.

While IBM’s fundamentals are more solid than a high-multiple name like Snowflake, its valuation has crept higher. The stock trades at a P/E of roughly 28.7x, compared to an industry average around 24x. Its P/S ratio is 4.7x, versus 3.5x for peers, and its P/B ratio of 10.5x is nearly three times the industry average of 3.7x. In other words, IBM isn’t exactly cheap, even if it is more profitable.

The company has posted positive GAAP net income in 10 of the last 11 quarters, with only a small loss in Q3 of last year. That said, free cash flow has been far more volatile. IBM recorded negative FCF in four of the past six quarters, including significant outflows of $2.99 billion in Q1 2025 and $1.26 billion in Q3 2024. While IBM typically generates solid cash flow over the course of a full year, the recent swings suggest some operational sensitivity, particularly if macro conditions or sentiment within the enterprise tech sector begin to deteriorate.

Ultimately, IBM represents a more stable but still exposed player in the AI ecosystem. If the broader narrative falters, even profitable names like IBM wouldn’t be immune to a sector-wide re-rating. In that bearish scenario, lower-priced options could offer a rare opportunity to benefit from a downside move without overpaying for this potential opportunity.

On the date of publication, Andrew Prochnow did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Michael Burry Warned That the AI Bubble Is About to Burst. If You Agree, Use Options to Bet Against These 2 Stocks.

- These 3 Unusually Active Puts Deep ITM Offer Strategic Plays for Both Bulls and Bears

- Cisco Delivered Strong, But Lower Free Cash Flow and FCF Margins - Has CSCO Stock Peaked?

- These 2 ETFs May Be the Best-Kept Secrets on Wall Street