The artificial intelligence (AI) boom has ignited one of the most intense technology races in history, with chipmakers battling for dominance in data centers, cloud infrastructure, and the next generation of AI workloads. And while Nvidia (NVDA) continues to command the spotlight, recent market turbulence has reminded investors that leadership in this space is anything but settled. Shares of the AI darling and its closest rival, Advanced Micro Devices (AMD), came under pressure last week after a report suggested Meta (META) may consider spending billions on Google’s (GOOG) (GOOGL) AI chips. This sparked fears that AMD could lose ground just as excitement around its MI series accelerators has begun to build.

But according to Mizuho’s Jordan Klein, investors may be looking at the situation through far too narrow a lens. Klein argues that the AI race isn’t a short-term sprint where early leaders automatically secure long-term victory. Instead, he describes it as a multi-phase marathon. In other words, no single headline—whether about a Google-Meta deal or a temporary pause in demand—should be mistaken for a definitive turning point.

With that, let’s take a closer look at why AMD still has a strong chance to finish at the front of the pack.

About Advanced Micro Devices Stock

Advanced Micro Devices is a globally recognized semiconductor firm specializing in the development and distribution of high-performance computing products. AMD offers a broad range of products, including AI accelerators, x86 microprocessors, and graphics processing units (GPUs), available both as standalone components and integrated within other systems. The company’s product lineup includes well-known brands like AMD Ryzen processors and AMD Radeon graphics. It currently has a market cap of $348.8 billion.

Shares of the chipmaker have rallied 80.1% on a year-to-date basis. Still, AMD shares pulled back sharply in November, dropping 22.8% from their recent all-time high of $267.08 as investors grew concerned about everything from interest rates and rising memory prices to Google’s increasing momentum in AI.

Is the AI Race Over for AMD?

Shares of Advanced Micro Devices came under pressure last week after The Information reported that Meta Platforms was in discussions to spend billions on Google’s AI chips. The reasoning behind the recent pullback was obvious. The report said Meta was in talks to begin using Google’s tensor processing units (TPUs) in its data centers starting in 2027. These chips, a type of application-specific integrated circuit (ASIC), offer a cheaper and more energy-efficient alternative to AMD’s more versatile GPUs. With that, the stock fell on concerns that Google’s TPUs could chip away at demand for AMD’s GPUs.

Some analysts noted that AMD may face increased investor scrutiny, given its role as an OpenAI supplier and its positioning as an alternative to Nvidia. “The company has built their story around becoming the viable second source to NVDA, and hitched their wagon to OpenAI’s horse,” said Bernstein analyst Stacy A. Rasgon. The analyst noted that with Google’s Gemini competing against OpenAI’s large-language models and Google’s TPUs emerging as a potential alternative to both Nvidia and AMD chips, the report undermines the AMD narrative. He reiterated the firm’s “Market Perform” rating on AMD stock.

Other voices on Wall Street were more optimistic about AMD’s prospects. Mizuho TMT specialist Jordan Klein said that while this could pose a “modest challenge” for Lisa Su-led AMD, it’s far too early to declare a winner in the AI race. Klein stated that viewing AI leadership as settled in late 2025 is “myopic.” He said the AI race will continue to see rapid shifts in positioning as companies invest heavily in compute, memory, networking, and power infrastructure. “This is a marathon that will see many different lead changes,” Klein wrote, noting how quickly sentiment swung earlier this year when Google was widely seen as trailing OpenAI. That said, the analyst’s comments suggest there’s still a case for buying AMD on the dip.

Bank of America’s Vivek Arya also defended Nvidia and AMD, pushing back against the market’s sharp rotation. Arya reaffirmed “Buy” ratings on both stocks. He said AMD continues to benefit from multiple growth drivers across CPUs, GPUs, embedded products, and gaming.

Meanwhile, Morgan Stanley analysts Brian Nowak and Joseph Moore wrote in a research note that Nvidia and AMD aren’t facing any immediate threat, as Meta’s latest move appears to be more of a diversification effort. “We don’t think Meta’s aspirations are changing: they want to diversify their compute infrastructure,” they wrote. Notably, AMD said at its annual Advancing AI event in June that Meta uses its Instinct MI300X chips for its Llama 3 and Llama 4 models and that the tech giant plans to use its current MI350 series and future generations of AMD accelerators as well.

Finally, Wedbush analyst Dan Ives named AMD as one of his “top ten tech stocks to own in the AI revolution.” AMD is “set to gain market share in AI arms race,” Ives said, adding that the stock offers a “compelling valuation.” “We believe this is a 1996 moment ... and NOT a 1999 bubble moment and remain firmly bullish on tech stocks into year-end and 2026 despite recent investor bearish fears,” the analyst said.

A Look at AMD’s Q3 Results

On Nov. 4, AMD reported better-than-expected financial results for the third quarter of 2025. The company posted a record revenue of $9.25 billion, driven by ongoing AI tailwinds, beating Wall Street estimates by $500 million. The top line grew 36% in the third quarter, slightly above the 32% increase in the second quarter and matching the 36% growth seen in the first quarter. Its profit came in at $1.20 per share, excluding certain items, topping expectations by $0.03.

AMD’s data center business, the biggest beneficiary of AI spending, grew 22% year-over-year (YoY) to $4.3 billion in the quarter, exceeding analysts’ expectations of $4.14 billion. The good news is that the segment’s growth rate improved sequentially—it was 14% in Q2—though it remains well below the pace of Nvidia’s data center business. Unsurprisingly, the growth was mainly fueled by strong demand for its 5th-generation AMD EPYC processors and AMD Instinct MI350 Series GPUs. Chief Executive Officer Lisa Su said on the conference call that AMD expects its AI business to bring in “tens of billions” of dollars in annual revenue by 2027.

What also stood out was AMD’s client and gaming segment, where revenue jumped 73% from a year earlier, driven by stronger client sales and higher gaming revenue. More precisely, Client revenue rose 46% YoY to $2.8 billion on robust demand for Zen 5 Ryzen CPUs, while Gaming revenue soared 181% YoY to $1.3 billion, boosted by strong demand for Radeon GPUs like the RX 9000 series.

Looking ahead, management said they anticipate roughly $9.6 billion in Q4 revenue, representing about 4% sequential growth and a 25% YoY increase. While analysts had expected $9.2 billion on average, some forecasts went as high as $9.9 billion, which contributed to a drop of as much as 5% in AMD’s stock during extended trading. Still, the stock ended the following trading session more than 2% higher as investors continued to digest the results.

Analysts currently expect AMD’s EPS to grow 20.22% YoY to $1.31 in Q4, while revenue is projected to increase 25.78% YoY to $9.63 billion.

What Do Analysts Expect for AMD Stock?

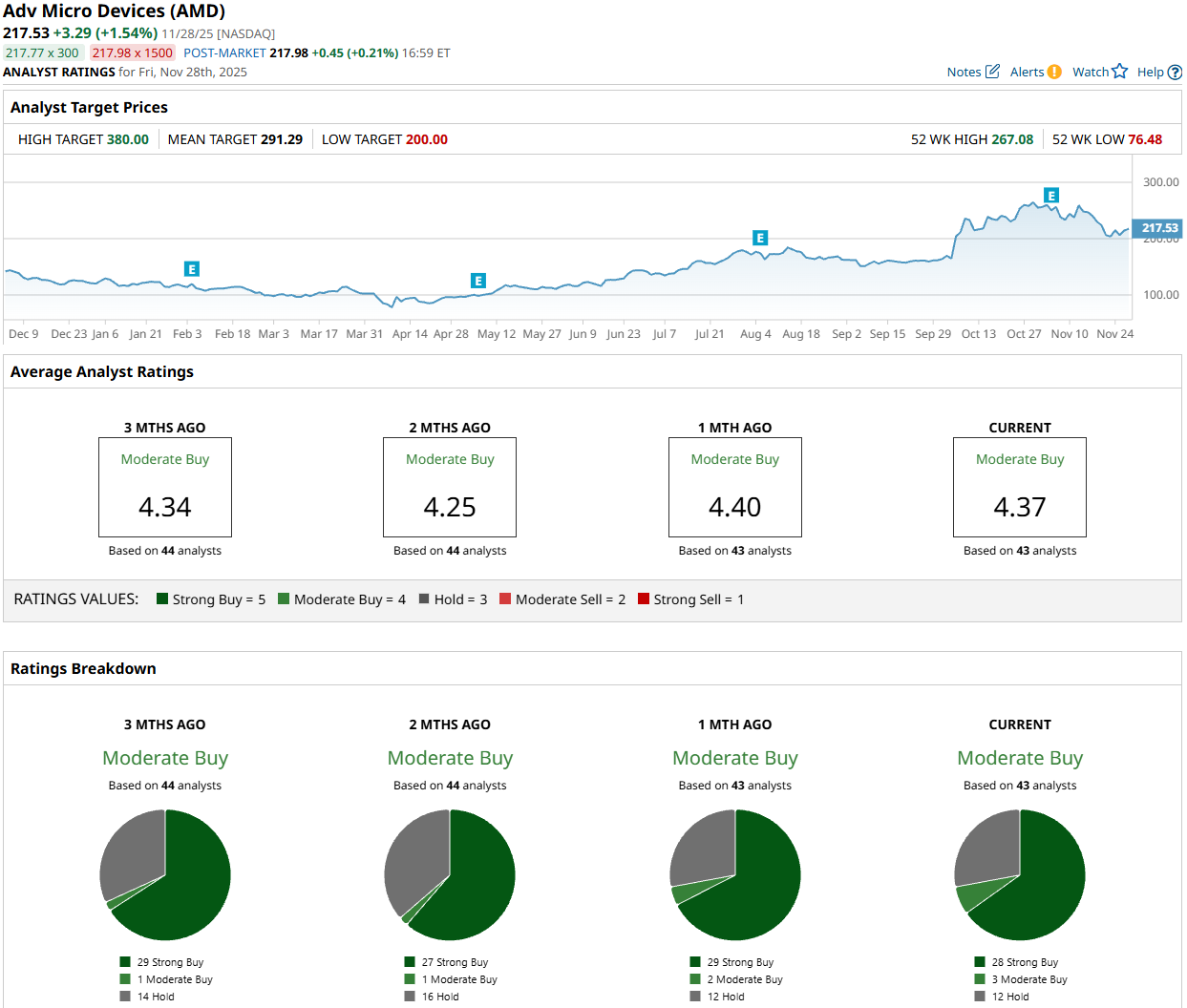

Most Wall Street analysts remain upbeat on AMD, as indicated by the stock’s consensus “Moderate Buy” rating. Out of the 43 analysts covering the stock, 28 recommend a “Strong Buy,” three a “Moderate Buy,” and 12 suggest holding. The average price target for AMD stock is $291.29, which sits 33.9% above Friday’s closing price.

To sum up, it’s still too early to draw any conclusions about who will ultimately come out on top in the AI race. We’ll likely continue to see rapid shifts in positioning as new developments and announcements emerge. AMD has a solid position in the AI race and even has the potential to emerge as a winner. AMD’s recent agreements with OpenAI, Oracle, and the U.S. Department of Energy highlight growing interest in its MI series of AI accelerators. Some investors viewed these deals as a sign that AMD might finally begin to challenge Nvidia’s dominance in the AI chip market. CEO Lisa Su said last month that the chipmaker expects the data center TAM to reach $1 trillion by 2030, with the company well-positioned to capitalize on that massive growth.

On the date of publication, Oleksandr Pylypenko had a position in: NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Morgan Stanley Just Named This Stock a Top Semiconductor Pick. Should You Buy Shares Now?

- AMD Stock Drops 15% in a Month: Should You Buy, Sell, or Hold?

- Is XPEV Stock a Buy for 2026 as XPeng Targets Breakeven and Pivots to Physical AI?

- Cathie Wood Is Buying GOOGL Stock as Alphabet Approaches $4 Trillion. Should You?