Long-term investing is about owning high-quality businesses that compound steadily over time. Here are two stocks that stand out for their durable business models, consistent execution, and ability to grow value patiently for investors willing to hold for the long run.

Smart Stock #1: ServiceNow

Valued at a $136 billion market capitalization, ServiceNow (NOW) is an enterprise software company that helps large organizations run their internal operations digitally and automatically. Basically, its workflow platform replaces manual work, emails, spreadsheets, and disconnected systems. By adopting AI, it has positioned itself as a core platform for enterprise AI and workflow transformation, which is most likely why Wall Street rates this stock a consensus “Strong Buy.”

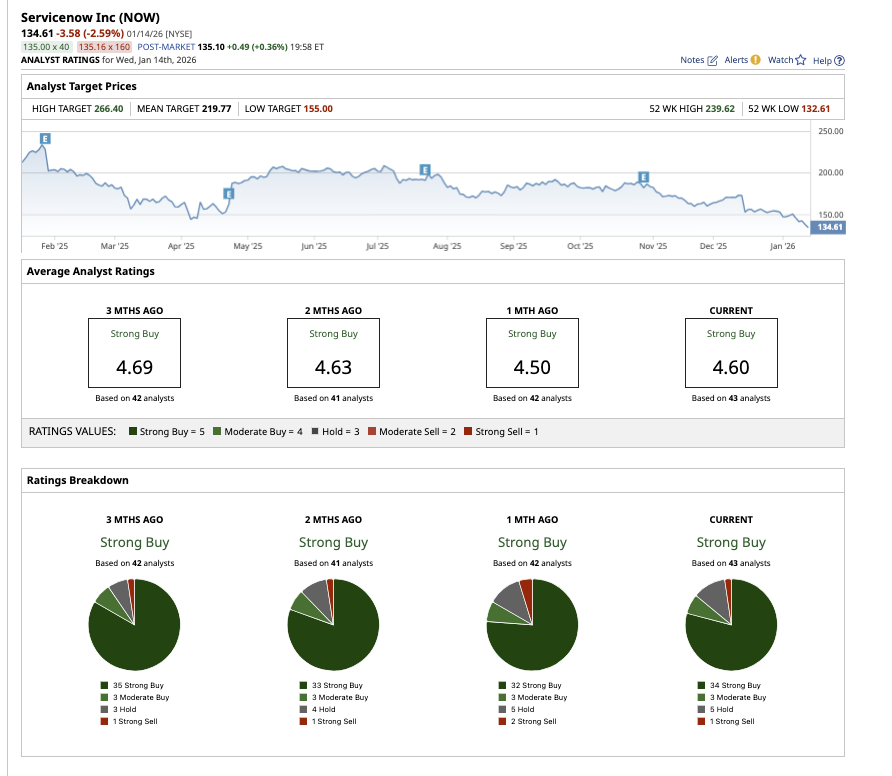

ServiceNow earns money by selling long-term, recurring software subscriptions to large enterprises and governments, with higher revenue as customers expand usage across the platform. In the third quarter, subscription revenues reached $3.3 billion, growing 20% year-over-year (YOY). Remaining performance obligations (RPO) climbed to approximately $24.3 billion, representing 23% YOY growth, while current RPO grew 21% to $11.3 billion. Profitability also exceeded expectations in the quarter, with adjusted net income up to $4.82 per share.

Deal activity remained exceptionally strong in the quarter. The company closed 103 deals worth more than $1 million in net new annual contract value (ACV), with three exceeding $20 million. Large-customer adoption has continued to grow, with the number of customers generating more than $50 million in ACV increasing by more than 20% YOY.

In the Q3 earnings call, management emphasized that core workflows such as ITSM, ITOM, ITAM, HR, security and risk, CRM, and industry workflows all played a role in driving broad-based demand.

Management stated that AI solutions are on track to achieve $500 million in ACV in 2025, indicating significant progress toward the $1 billion target in 2026. Now Assist, in particular, outperformed expectations with 12 transactions above $1 million, including one exceeding $10 million. Furthermore, ServiceNow experienced tremendous growth across industries. Transportation and logistics led with over 90% YOY growth in net new ACV, followed by retail, hospitality, and education, all of which increased by more than 50%. Energy, utilities, and government continue to be strong sectors for ServiceNow as well.

ServiceNow ended the quarter with a strong balance sheet, holding $9.7 billion in cash and investments. During Q3, the company repurchased around 644,000 shares, nearly 70% more than the prior quarter, primarily to manage dilution. The company has $2 billion in authorization remaining under its repurchase program. The company’s board also approved a five-for-one stock split which is intended to make shares more accessible and provide employees with greater flexibility in managing equity.

ServiceNow will report its Q4 results on Jan. 28. The company anticipates subscription sales of $3.42 billion to $3.43 billion and an operating margin of 30%, but cautions that potential government shutdown-related timing concerns may affect U.S. federal deal closings. Analysts predict ServiceNow’s earnings to increase by 25% in 2025, followed by a 17% increase in 2026. With AI, data, and workflows unified, ServiceNow sits at the center of enterprise AI transformation and a growing opportunity set ahead.

What Does Wall Street Say About NOW Stock?

NOW stock has dipped 40% over the last year, compared to the broader market gain of 17%. Overall, on Wall Street, NOW stock has a “Strong Buy” consensus rating. Out of the 43 analysts covering the stock, 34 have a “Strong Buy," three suggest a “Moderate Buy," five recommend a “Hold,” and one has a “Strong Sell.” The mean target price for NOW is $219.69, which implies 72% potential upside from current levels. Its high price estimate of $266.40 implies potential upside of 109% over the next 12 months.

Smart Stock #2: Arista Networks

As AI workloads scale rapidly, this next company's importance in the AI ecosystem is growing rapidly. Valued at $164.5 billion, Arista Networks (ANET) designs high-speed computer networks that help large firms, cloud providers, and AI data centers move enormous amounts of data quickly and reliably.

In the third quarter, Arista generated $2.31 billion in revenue, 28% YOY growth, supported by strong demand from cloud, AI, enterprise, and campus customers. A growing portion of revenue came from software and services, which accounted for 18.7% of total sales, highlighting the increasing role of higher-margin offerings. Profitability also improved, with an adjusted gross margin of 65.2%, owing to a positive product mix and inventory dynamics. Diluted EPS rose 25% YOY to $0.75.

Deferred revenue increased to $4.7 billion, indicating strong client demand and an ongoing ramp-up of AI-related deployments. Notably, the Americas generated roughly 80% of revenue, with international markets accounting for around 20%. Management stated that AI-driven networking demand is unlike anything previously seen, with clients transporting massive data sets over increasingly complicated architectures.

Arista's EtherLink portfolio — which provides centralized control over automation, security, traffic management, and telemetry — is driving this massive demand. These networks are designed to maximize the efficiency of AI accelerators, ensuring that data flows quickly and consistently even at large scale. The company ended the quarter with $10.1 billion in cash, cash equivalents, and investments. Arista also retains $1.4 billion under its authorized share repurchase program. Management reaffirmed its target of at least $1.5 billion in AI-related revenue by 2025. Looking ahead, fiscal 2026 goals include $2.75 billion in AI data center revenue as part of a larger $10.65 billion total revenue target, meaning roughly 20% overall growth.

Management expects the total addressable market for networking to exceed $100 billion in the coming years, providing a long runway for expansion. With that in mind, analysts anticipate strong earnings growth of 27% in 2025 and nearly 17% in 2026. At roughly 42 times forward earnings, ANET stock also trades at a premium, reflecting expectations for continued momentum. For investors comfortable with the short-term volatility, Arista represents a high-quality way to gain exposure to the infrastructure powering the AI revolution over the long term.

What Does Wall Street Say About ANET Stock?

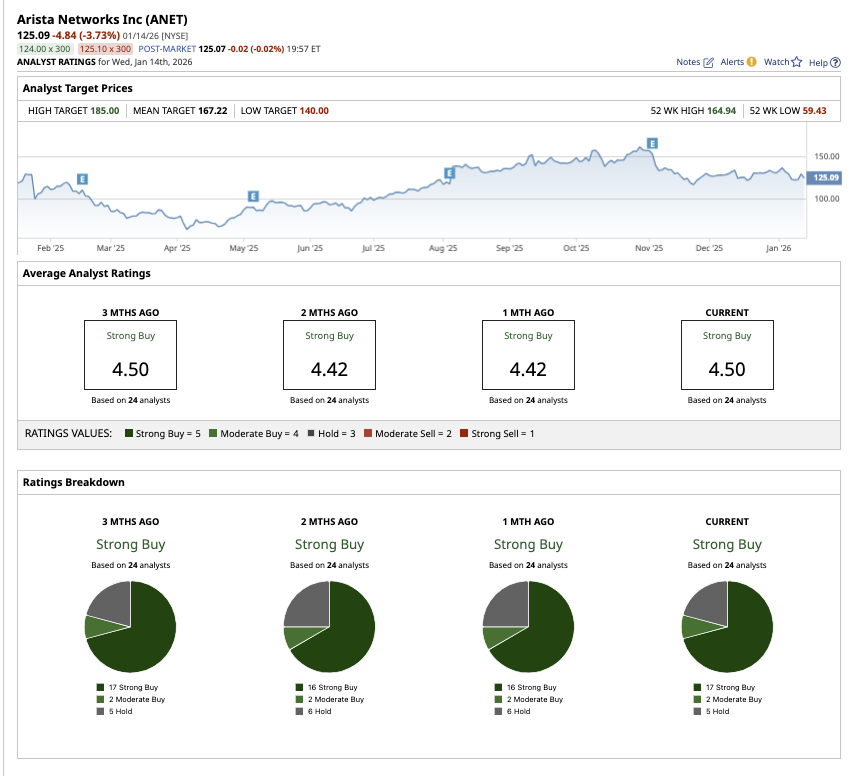

ANET stock has surged 10% over the past 52 weeks, slightly underperforming the broader market. So far this year, the stock is also down 1%. Nonetheless, ANET's average price target of $167.22 implies a potential surge of 29% from current levels. Meanwhiel, the Street-high estimate of $185 implies potential upside of about 42%.

Overall, Wall Street rates ANET stock as a consensus “Strong Buy.” Out of the 24 analysts covering shares, 17 have a “Strong Buy” recommendation, two rate Arista as a “Moderate Buy,” and five suggest a “Hold" rating.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- The Most Overlooked Dividend Kings to Buy in 2026

- 2 Smart Stocks for Patient Long-Term Investors to Buy Now

- Super Micro Computer Is One of the Most Shorted Stocks. Could a Squeeze Take It Higher in 2026?

- Intel Reports Earnings on January 22. Here Is Where Options Data Says INTC Stock Could Be Trading Next.