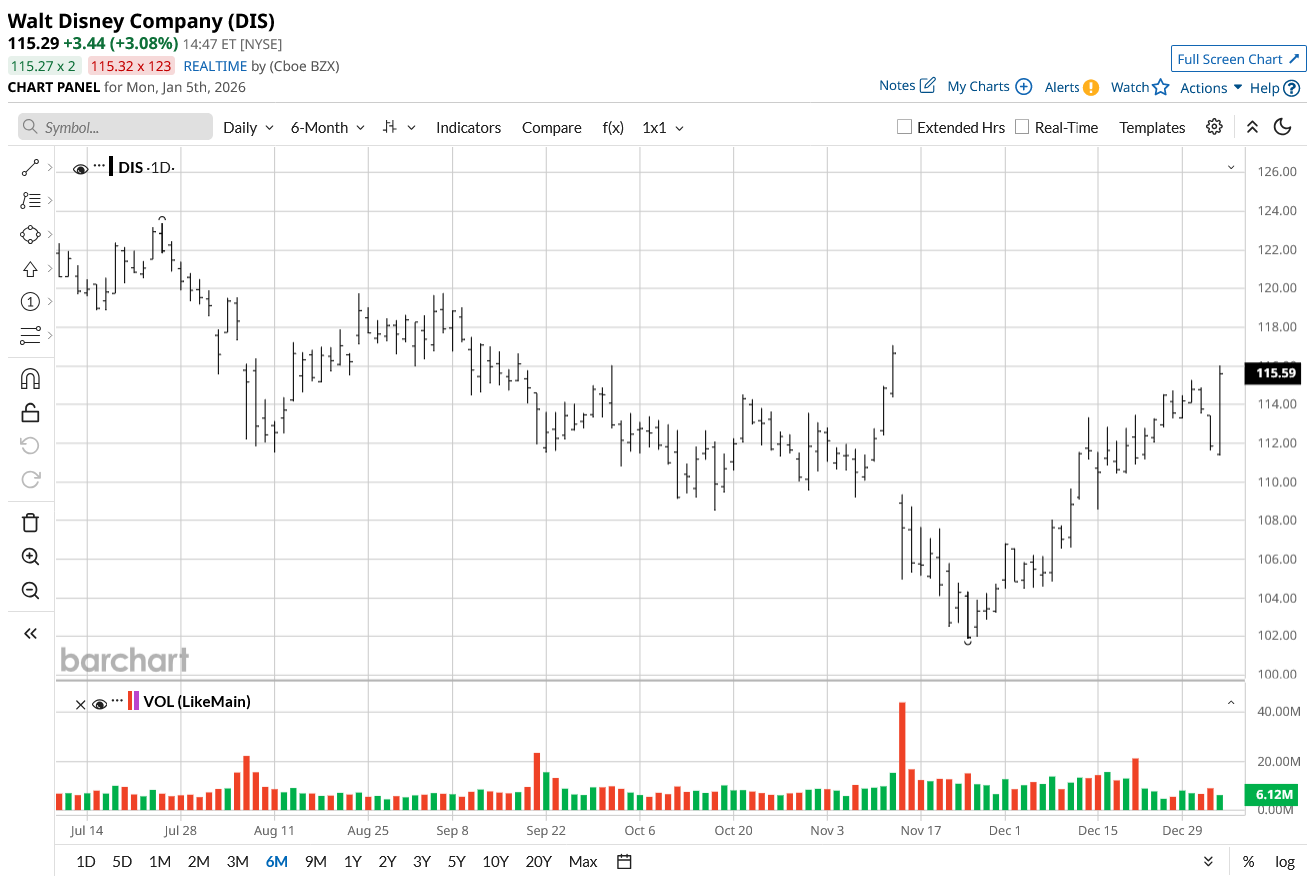

Walt Disney (DIS) stock has been an underperformer, having remained sideways in the past 12 months. One factor that has contributed to the time correction is mixed results. In the last two quarterly numbers, Disney has missed on revenue estimates even as the company delivered better-than-expected EPS.

However, the sideways movement, valuation consideration, and the company’s outlook for FY26 and FY27 point to an attractive entry opportunity.

Recently, Wolfe Research analyst Peter Supino assigned an “Outperform” rating for DIS stock with a price target of $133. Peter believes that DIS stock is undervalued at 16 times FY26 earnings when compared to S&P 500 ($SPX) multiples and Netflix’s (NFLX) market value. The analyst also highlights that “valuable intellectual property” strengthens the case for higher valuations.

About Disney Stock

Walt Disney is an entertainment company with a focus on the Americas, Europe, and Asia Pacific. The company operates in three segments—Entertainment, Sports, and Experiences.

For FY25, Disney reported 3% year-on-year (YoY) growth in revenue to $94.4 billion. While revenue was flat on a YoY basis for the sports business, the entertainment and experiences segments witnessed 3% and 6% growth, respectively.

While Disney has an optimistic outlook for FY26 and beyond, the stock has corrected by 7% in the past six months. This seems like a good accumulation opportunity before fundamentals and growth acceleration trigger major positive price action.

Positives From FY 2025 Results

Besides the headline numbers, there are multiple positives to note from the company’s FY25 results. For Q4 2025, Disney reported paid subscribers of 131.6 million, which was higher by 3% on a quarter-on-quarter (QoQ) basis. It’s likely that subscriber growth will be sustained on the back of a strong asset of content.

In the Experiences segment, Disney reported 6% revenue growth. With two new cruise ships joining the fleet in the coming months, growth will be supported. At the same time, the company has expansion projects at all of its theme parks. These investments provide growth visibility.

From a balance sheet perspective, Disney reported $5.7 billion in cash as of FY25. A strong cash buffer coupled with robust cash flows ensures headroom for aggressive investments. It’s also worth noting that the company ended FY25 with total debt of $42 billion. On a YoY basis, total debt declined by $3.8 billion. With prospects of healthy cash flows, deleveraging is likely to continue.

Strong Outlook for Fiscal Years 2026 and 2027

Disney has guided for strong growth in the next two financial years. To put things into perspective, the company expects double-digit EPS growth in FY26 on a YoY basis.

Further, Disney expects operating cash flow of $19 billion. With targeted capital expenditure at $9 billion, the free cash flow is expected to be robust at $10 billion. This will ensure aggressive share repurchase besides the cash dividend.

Even for FY27, the company has guided for double-digit EPS growth as compared to FY26. As growth sustains, it would potentially imply further upside in cash flows and headroom for dividend growth.

What Analysts Say About DIS Stock

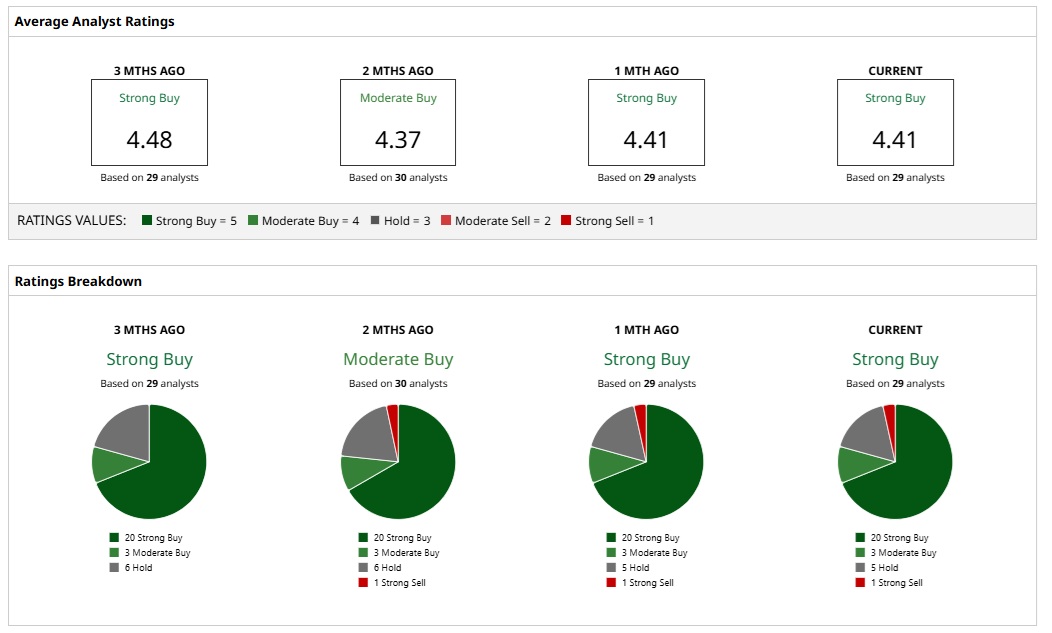

Based on the ratings of 29 analysts, DIS stock is a consensus “Strong Buy.” While 20 analysts assign a “Strong Buy” rating to DIS, three analysts have a “Moderate Buy” rating, and five analysts have a “Hold” rating. Further, one analyst believes that the stock is a “Strong Sell.”

Based on these ratings, analysts have a mean price target of $135.28 currently, which would imply an upside potential of 17%. Further, with the most bullish price target of $160, the upside potential for DIS stock is 39%.

The bullish view is underscored by the point that DIS stock trades at 16 times FY26 earnings. Additionally, the dividend yield is attractive at 1.32%, and with the guidance for healthy earnings growth, there is a case for higher dividends in the coming years.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart