California-based Applied Materials, Inc. (AMAT) is the world's largest supplier of semiconductor manufacturing equipment and one of the most important companies in the global semiconductor supply chain. Valued at $357 billion by market cap, Applied Materials provides the tools, software, and services that chipmakers use to manufacture advanced semiconductors, display panels, and other electronic components.

Companies worth $200 billion or more are generally described as “mega-cap stocks,” and AMAT definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the semiconductor equipment & materials industry. The company is a market leader in key chipmaking processes such as deposition, etching, inspection, and advanced packaging, enabling customers to produce increasingly powerful and complex semiconductors. Its extensive technology portfolio, deep relationships with leading chipmakers, large installed equipment base, and strong research and development capabilities create significant competitive advantages.

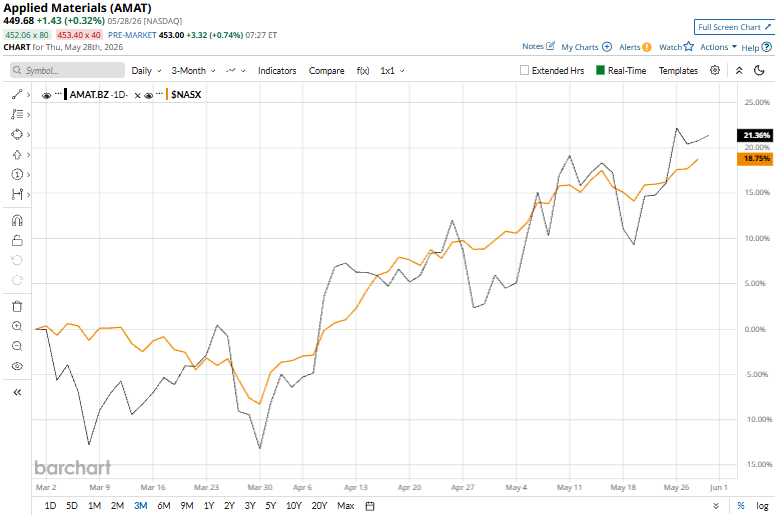

AMAT shares recently touched their 52-week high of $462.40 on May 27. Over the past three months, AMAT stock has gained 20.8%, outpacing the broader Nasdaq Composite’s ($NASX) 18.8% rise over the same time frame.

Shares of AMAT rose 75% on a YTD basis and climbed 178.3% over the past 52 weeks, notably outperforming NASX’s 15.8% YTD gains and 40.9% returns over the last year.

To confirm the bullish trend, AMAT has been trading above its 50-day and 200-day moving averages since mid-September, 2025, with slight fluctuations.

Shares of Applied Materials rose 4.9% on May 20 after the company announced a partnership with Broadcom Inc. (AVGO) to accelerate the development of advanced chip-packaging technologies for next-generation AI systems. The collaboration reinforced investor confidence in Applied Materials' ability to capitalize on growing AI-driven semiconductor demand.

The stock also benefited from positive analyst sentiment after Morgan Stanley reiterated its “Overweight” rating and raised its price target, citing the company's strong positioning to benefit from increased AI-related spending.

AMAT’s rival, Lam Research Corporation (LRCX), has taken the lead, with an 85.8% uptick on a YTD basis and solid 278.6% gains over the past 52 weeks.

Wall Street analysts are bullish on AMAT’s prospects. The stock has a consensus “Strong Buy” rating from the 38 analysts covering it, and the mean price target of $514.09 suggests a potential upside of 14.3% from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- The S&P 500’s Price Is Getting Better Every Week, But This Indicator Keeps Getting Worse. Why 52% Could Be The Market’s Tragic Number.

- Why Morgan Stanley Is Betting That $1,100 Is in Store for AppLovin Stock

- Unusual Options Activity Points to Boston Scientific Stock as a Hot M&A Target

- Snowflake Stock Rallies on Blockbuster Q1 Results. It Turns Out That Gen AI Isn’t Eating Its Lunch.