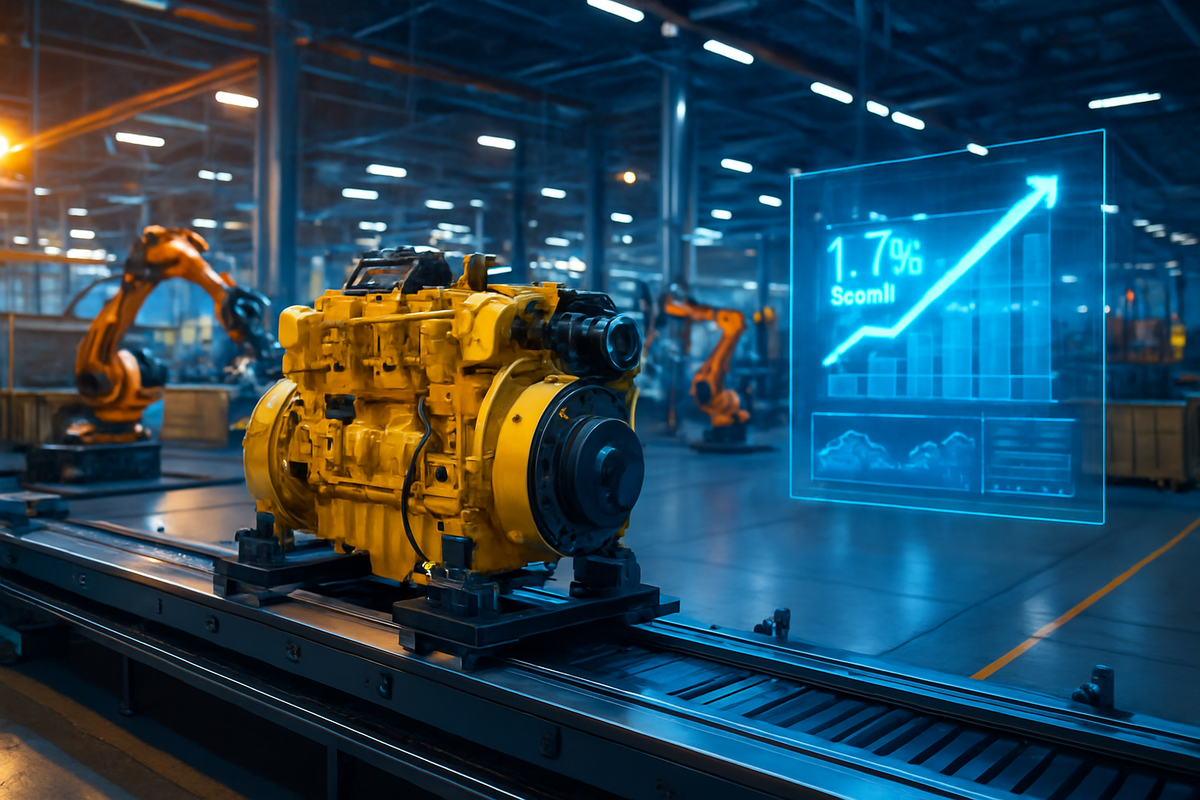

The U.S. manufacturing sector received a significant shot of confidence on January 29, 2026, as the Census Bureau released data for November 2025 showing a robust 1.7% rise in factory orders. This increase, which met and in some segments exceeded analyst expectations, suggests that the American industrial base is entering 2026 with more momentum than many economists had predicted during the volatile fourth quarter of the previous year.

The 1.7% uptick serves as a critical indicator of business investment and consumer demand, signaling that despite high-interest rates and shifting trade policies, domestic production remains on a growth trajectory. This data has immediate implications for the broader economy, providing a "soft landing" narrative for the Federal Reserve and suggesting that the "higher-for-longer" rate environment has not yet dampened the industrial sector's appetite for expansion and modernization.

Resilient Demand in a Shifting Economic Landscape

The data released on January 29th provides a granular look at where the American economy is putting its capital. While the 1.7% headline figure for factory orders captures the general trend, the internal components of the report reveal a manufacturing sector in transition. Much of the growth was driven by a surge in durable goods, particularly in the electrical equipment and machinery sectors. The 1.7% rise in orders for electrical equipment, specifically, highlights the unrelenting demand for components supporting AI infrastructure and data center expansion—a trend that has become a cornerstone of industrial growth in the mid-2020s.

The timeline leading up to this release was marked by significant skepticism. Throughout late 2025, markets were rattled by fluctuations in transportation orders and a cooling housing market. However, the November data indicates a "rebound effect," as companies that had paused capital expenditures earlier in the year began to finalize orders to secure production slots for 2026. Stakeholders, from supply chain managers to institutional investors, have closely watched these figures for signs of a recessionary pullback that, as of this report, has yet to materialize.

Initial market reactions were telling of the current investor psyche. On the day of the release, the Dow Jones Industrial Average saw a modest lift as "old economy" industrial giants found favor. However, the gains were tempered by a cautious outlook on the Nasdaq, as investors weighed the strong industrial data against the potential for the Federal Reserve to maintain restrictive interest rates to prevent the economy from overheating.

Industrial Titans: Winners and Losers in the 2026 Cycle

The ripple effects of the 1.7% rise in factory orders are perhaps most visible in the performance of heavy machinery leaders like Caterpillar Inc. (NYSE: CAT). Caterpillar, which reported earnings on the same day as the factory orders release, has emerged as a primary beneficiary of the industrial surge. With orders for power generation equipment hitting record highs, the company’s stock reached a 52-week high, driven by the same data center demand reflected in the national factory order report. For Caterpillar, the 2026 outlook remains bright, provided they can navigate the rising costs of raw materials.

Conversely, The Boeing Company (NYSE: BA) presents a more complex picture. While the factory orders report was bolstered by a massive spike in non-defense aircraft orders, Boeing continues to grapple with production stability. For Boeing, the rise in orders is a double-edged sword: it verifies massive market demand for its 737 MAX and 787 platforms, but it also increases the pressure on a supply chain that is still recovering from years of disruption. Investors are watching to see if Boeing can convert this order momentum into actual deliveries and positive free cash flow in the 2026 fiscal year.

In the agricultural space, Deere & Company (NYSE: DE) faces a different set of challenges. Despite the general rise in factory orders, Deere has signaled that 2026 may represent the "bottom" of the current agricultural cycle. While industrial and construction demand remains high, the agricultural machinery segment is cooling. Deere is currently pivoting its strategy toward domestic manufacturing, recently announcing a $70 million facility in North Carolina, but the company remains vulnerable to potential tariff headwinds that could impact its export-heavy business model.

The Broader Significance: Reshoring and the AI Boom

The 1.7% rise in factory orders fits into a much larger trend of "reshoring" and the modernization of American manufacturing. Since the passage of the CHIPS Act and various infrastructure bills in previous years, the U.S. has seen a sustained increase in domestic factory construction. The November data suggests that these new facilities are finally coming online and placing orders for the heavy machinery and electrical components needed to begin operations. This is a structural shift in the U.S. economy, moving away from a pure service-based model back toward a more balanced industrial-and-service hybrid.

This event also highlights the "ripple effect" of the artificial intelligence boom on sectors far removed from Silicon Valley. The demand for electrical equipment and specialized cooling systems for data centers is now a primary driver of factory orders. This has created a symbiotic relationship between Big Tech and Big Industry, where the growth of the former is now fundamentally dependent on the manufacturing capacity of the latter.

Historically, a 1.7% rise in factory orders at this stage of an interest-rate cycle would be seen as an anomaly. Comparisons to the post-2008 recovery or the 2016 industrial mini-boom suggest that the current resilience is unique, likely fueled by the massive amounts of fiscal stimulus and industrial policy enacted between 2021 and 2024. However, the looming threat of new trade barriers and a potential 50% tariff on various imported components remains the "wild card" that could disrupt this momentum as 2026 progresses.

Navigating the Road Ahead: 2026 and Beyond

Looking forward, the manufacturing sector faces a "pivotal" year. In the short term, the robust order book from November provides a cushion for manufacturers, ensuring that production lines will remain busy through at least the first half of 2026. However, the strategic pivot for many companies will involve diversifying supply chains to mitigate the risk of new tariffs. We may see a "pre-ordering" frenzy in the coming months as firms attempt to lock in prices before potential new trade policies take effect.

The long-term challenge will be labor. As factory orders rise, the demand for skilled industrial workers continues to outpace supply. This may lead to an accelerated investment in robotics and AI-driven automation within the factories themselves. For investors, the opportunity lies in companies that not only produce goods but also provide the automation technology that allows factories to scale despite labor shortages.

Potential scenarios for the remainder of 2026 range from a sustained industrial "renaissance" to a sharp correction if trade tensions lead to a global slowdown. The key will be the Federal Reserve’s reaction to this strength. If the 1.7% growth in orders leads to a spike in producer prices, the central bank may be forced to delay the rate cuts that many industrial firms are counting on to fund their 2027 expansion plans.

Summary: A Sector in Transition but Growing

The November factory orders data released on January 29, 2026, confirms that the U.S. manufacturing sector is more resilient than anticipated. The 1.7% rise is a testament to the enduring demand for American-made goods, particularly in the sectors of aerospace, electrical equipment, and heavy machinery. While challenges like the "trough" in the agricultural cycle and the looming threat of tariffs persist, the underlying infrastructure for growth—driven by AI and reshoring—remains solid.

Moving forward, the market appears to be shifting its focus from "if" a recession will happen to "how" companies will manage the growth they are currently experiencing. The industrial sector is no longer just a bellwether for the economy; it is becoming a primary engine of it once again.

For investors, the coming months will require a discerning eye. Watch for the quarterly delivery numbers from Boeing and the margin reports from Caterpillar and John Deere. These will provide the real-world confirmation of whether the 1.7% rise in orders is translating into sustainable bottom-line growth or if it is being swallowed by the rising costs of a changing global trade environment.

This content is intended for informational purposes only and is not financial advice.