Corning trades at $54.39 per share and has stayed right on track with the overall market, gaining 5.5% over the last six months. At the same time, the S&P 500 has returned 4.1%.

Is there a buying opportunity in Corning, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Corning Will Underperform?

We're cautious about Corning. Here are three reasons why we avoid GLW and a stock we'd rather own.

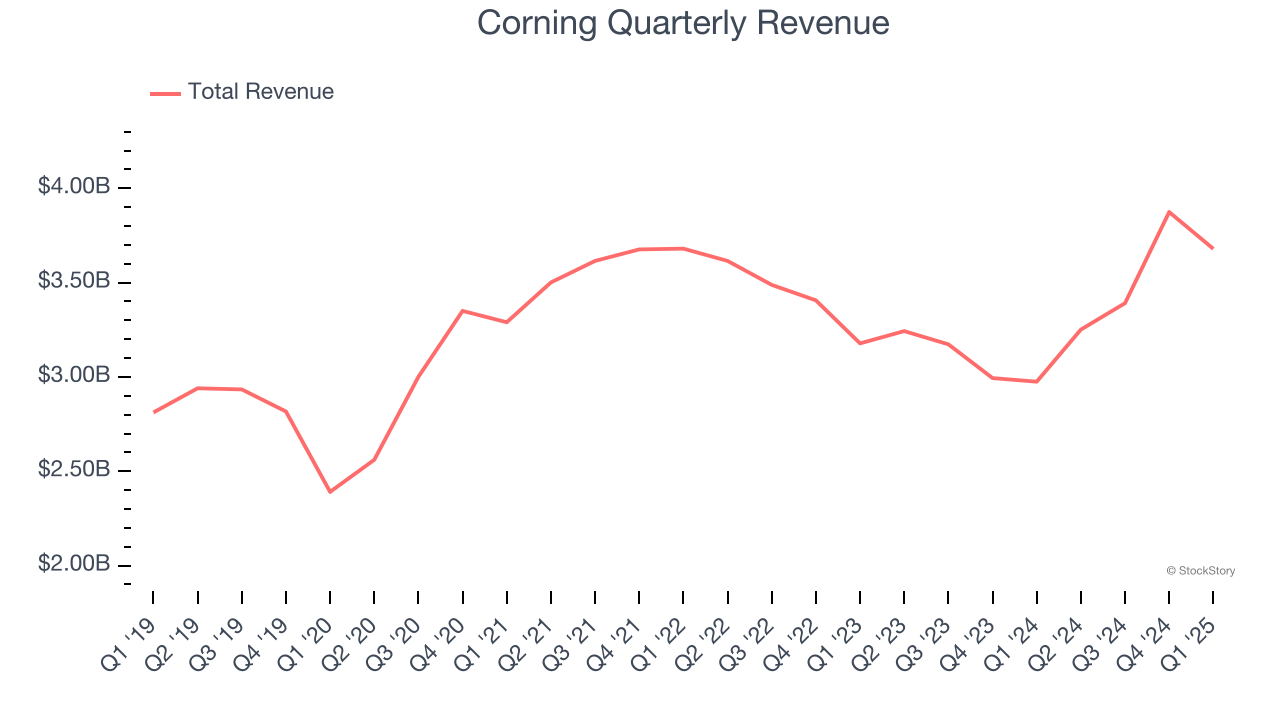

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Corning’s 5.1% annualized revenue growth over the last five years was tepid. This was below our standard for the industrials sector.

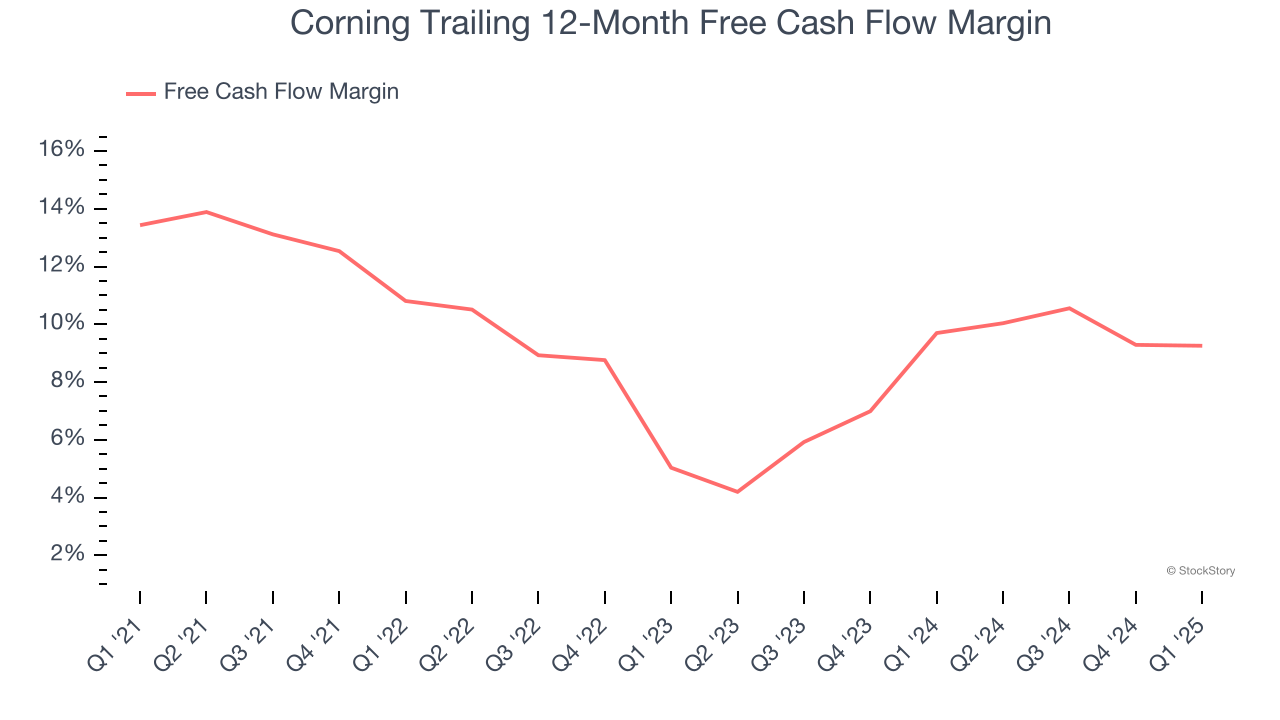

2. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Corning’s margin dropped by 4.2 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Corning’s free cash flow margin for the trailing 12 months was 9.3%.

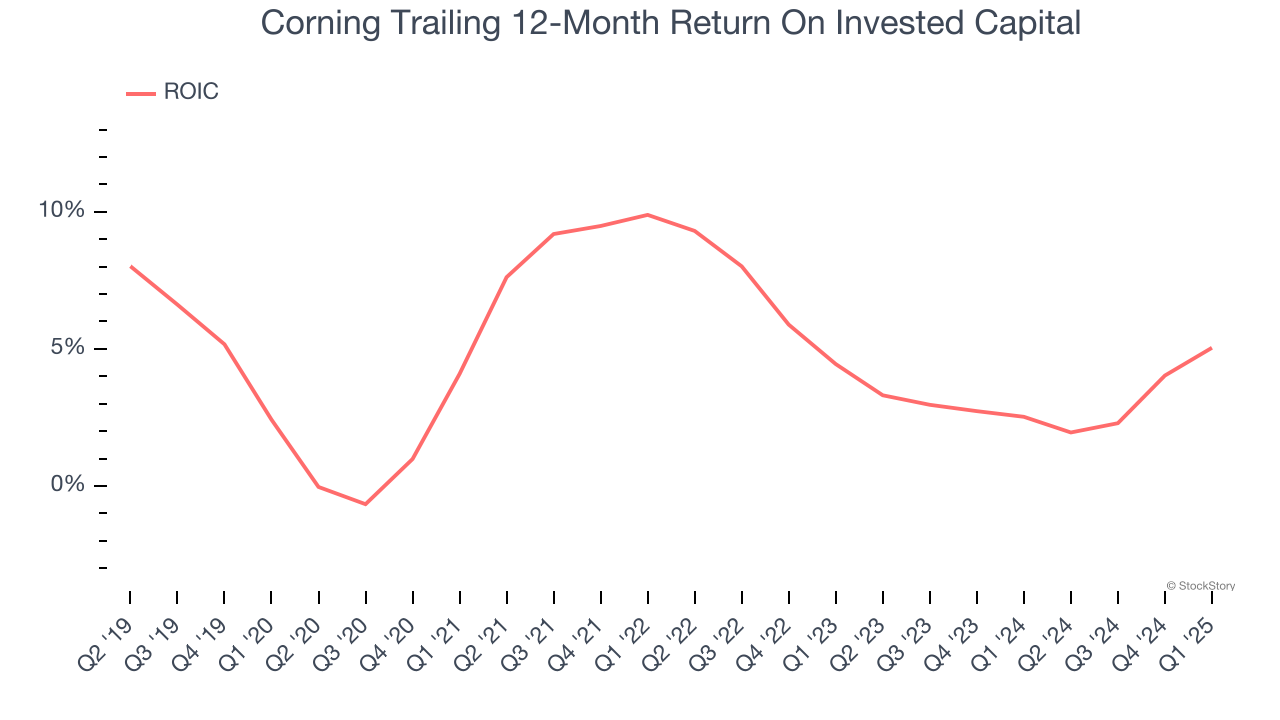

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Corning historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.2%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

Final Judgment

We see the value of companies helping their customers, but in the case of Corning, we’re out. That said, the stock currently trades at 22.6× forward P/E (or $54.39 per share). This multiple tells us a lot of good news is priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward our favorite semiconductor picks and shovels play.

Stocks We Like More Than Corning

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.