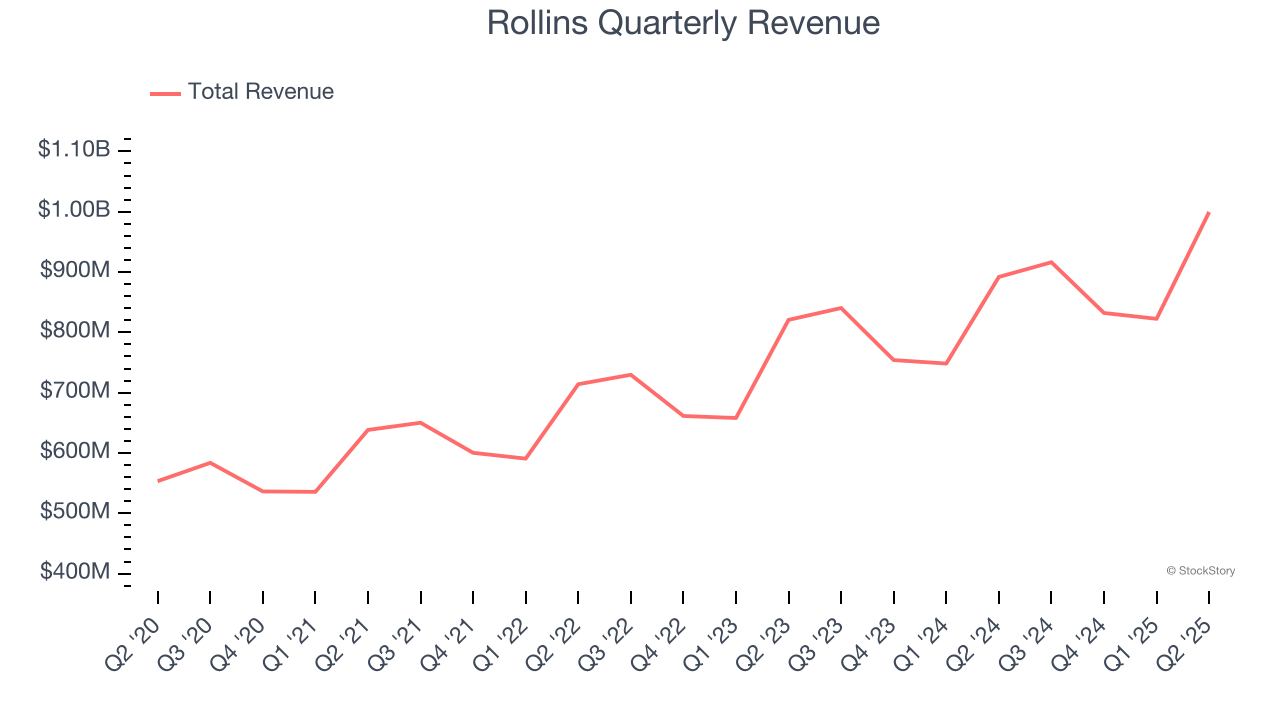

Pest control company Rollins (NYSE: ROL) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 12.1% year on year to $999.5 million. Its non-GAAP profit of $0.30 per share was in line with analysts’ consensus estimates.

Is now the time to buy Rollins? Find out by accessing our full research report, it’s free.

Rollins (ROL) Q2 CY2025 Highlights:

- Revenue: $999.5 million vs analyst estimates of $989.1 million (12.1% year-on-year growth, 1.1% beat)

- Adjusted EPS: $0.30 vs analyst estimates of $0.30 (in line)

- Adjusted EBITDA: $231.2 million vs analyst estimates of $230.7 million (23.1% margin, in line)

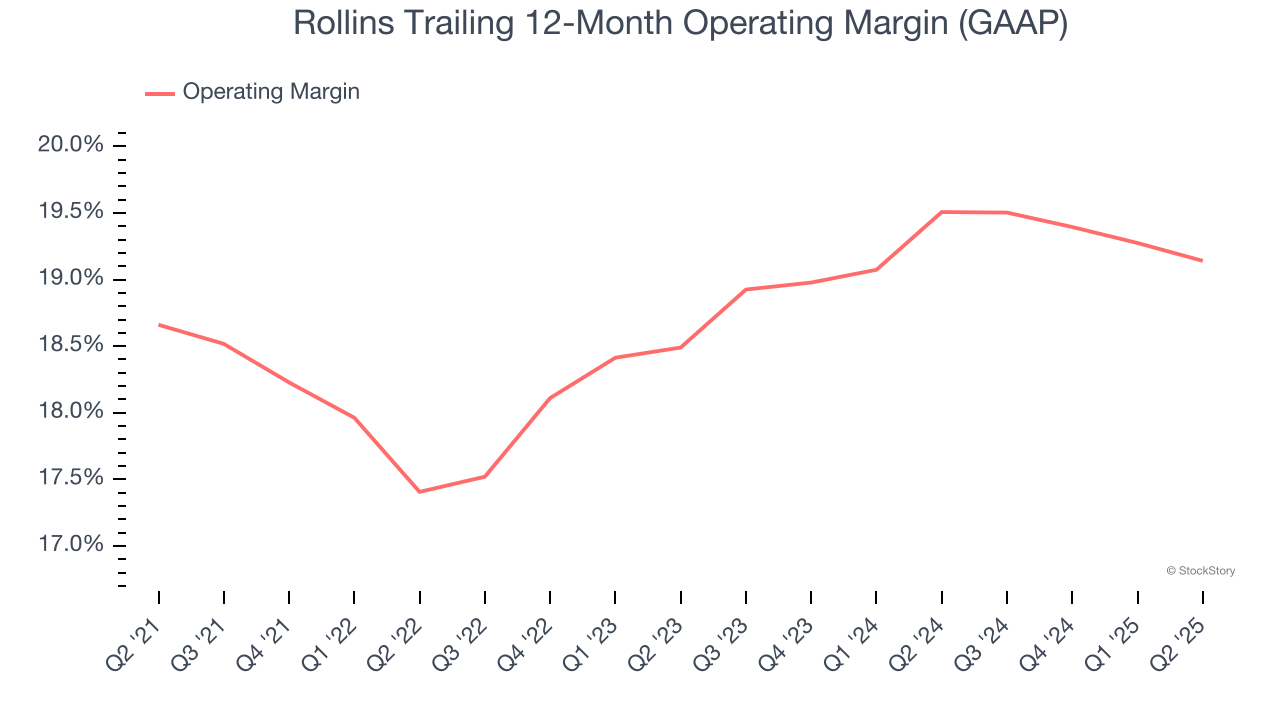

- Operating Margin: 19.8%, in line with the same quarter last year

- Free Cash Flow Margin: 16.8%, up from 15.3% in the same quarter last year

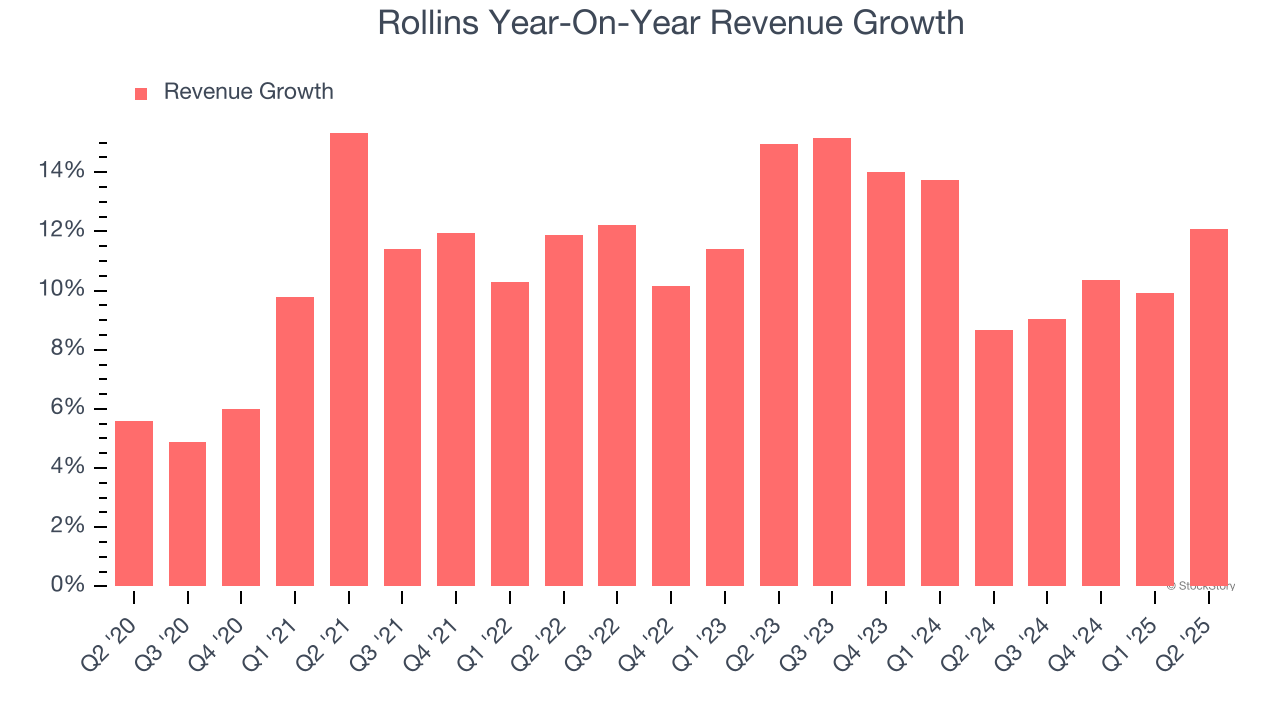

- Organic Revenue was up 7.3% year on year

- Market Capitalization: $26.9 billion

Company Overview

Operating under multiple brands like Orkin and HomeTeam Pest Defense, Rollins (NYSE: ROL) provides pest and wildlife control services to residential and commercial customers.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Rollins’s sales grew at an impressive 11.2% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Rollins’s annualized revenue growth of 11.5% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

Rollins also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Rollins’s organic revenue averaged 7.4% year-on-year growth. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Rollins reported year-on-year revenue growth of 12.1%, and its $999.5 million of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 9.8% over the next 12 months, a slight deceleration versus the last two years. Still, this projection is noteworthy and indicates the market is baking in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Rollins’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 18.7% over the last five years. This profitability was elite for an industrials business thanks to its efficient cost structure and economies of scale. This is seen in its fast historical revenue growth and healthy gross margin, which is why we look at all three data points together.

Analyzing the trend in its profitability, Rollins’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Rollins generated an operating margin profit margin of 19.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

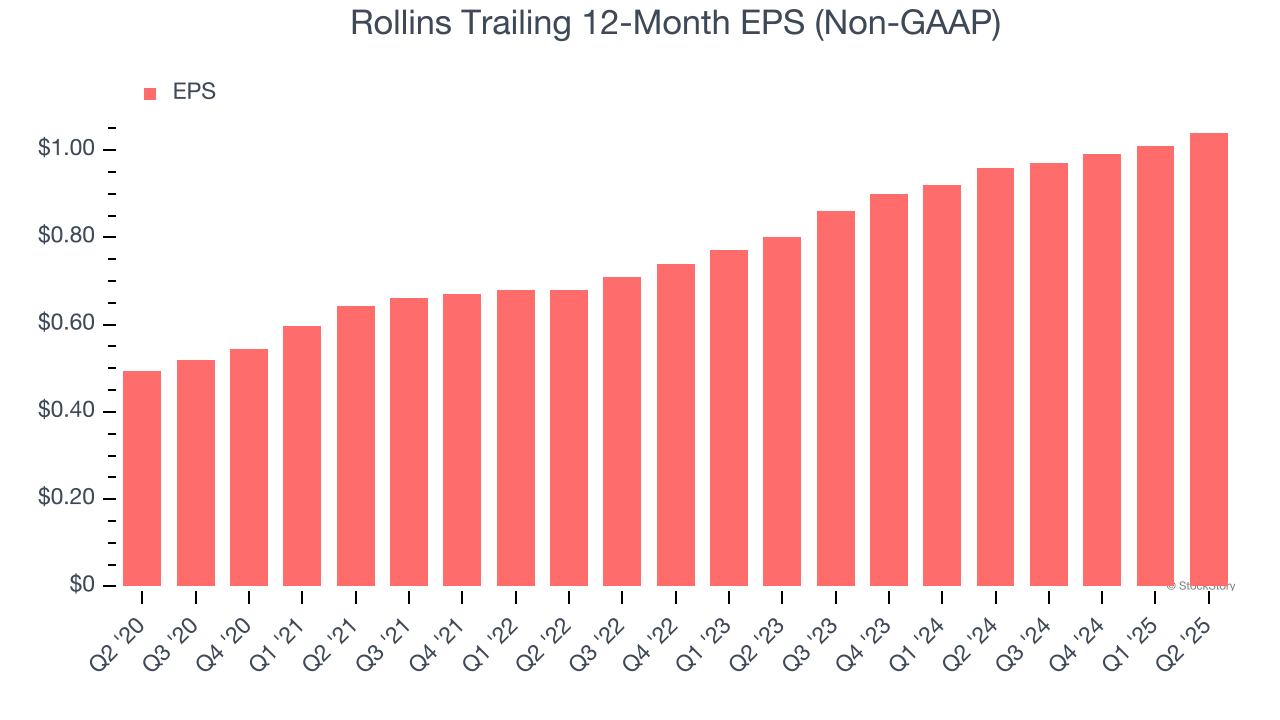

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Rollins’s EPS grew at a spectacular 16.1% compounded annual growth rate over the last five years, higher than its 11.2% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

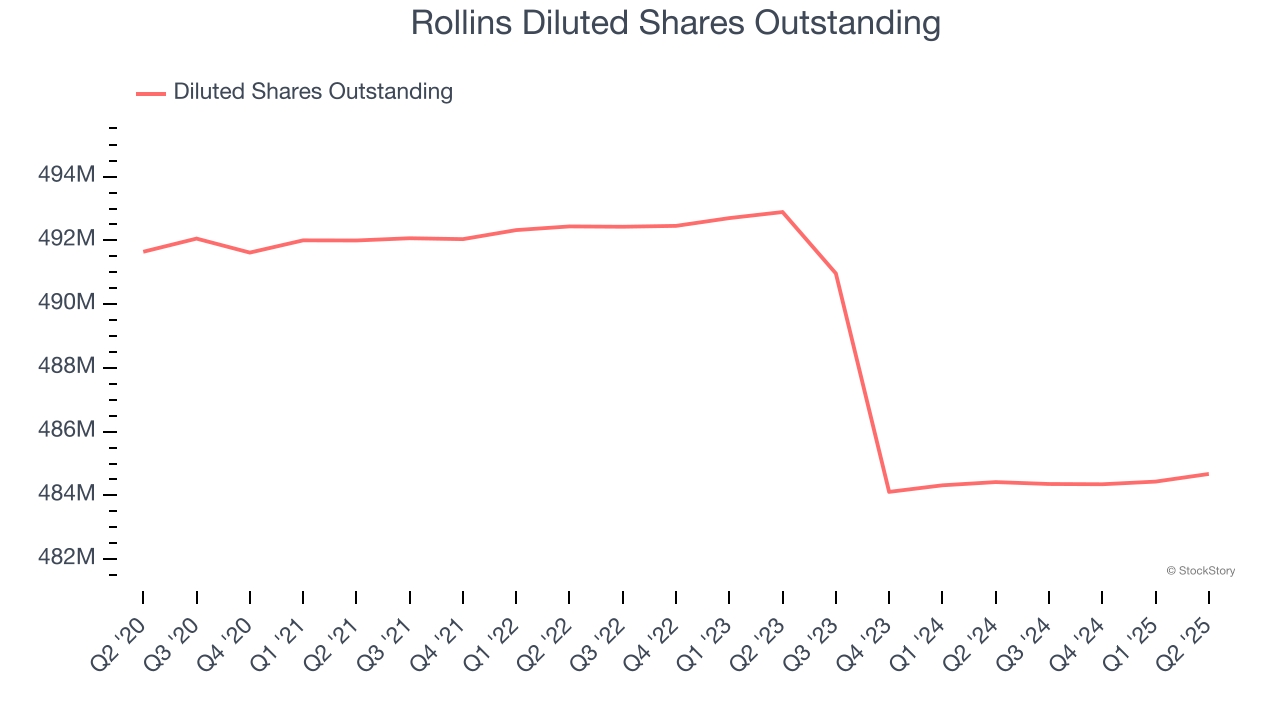

We can take a deeper look into Rollins’s earnings quality to better understand the drivers of its performance. A five-year view shows that Rollins has repurchased its stock, shrinking its share count by 1.4%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Rollins, its two-year annual EPS growth of 14% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q2, Rollins reported EPS at $0.30, up from $0.27 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Rollins’s full-year EPS of $1.04 to grow 12.2%.

Key Takeaways from Rollins’s Q2 Results

It was good to see Rollins narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS slightly missed. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 2.4% to $53.86 immediately following the results.

So do we think Rollins is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.