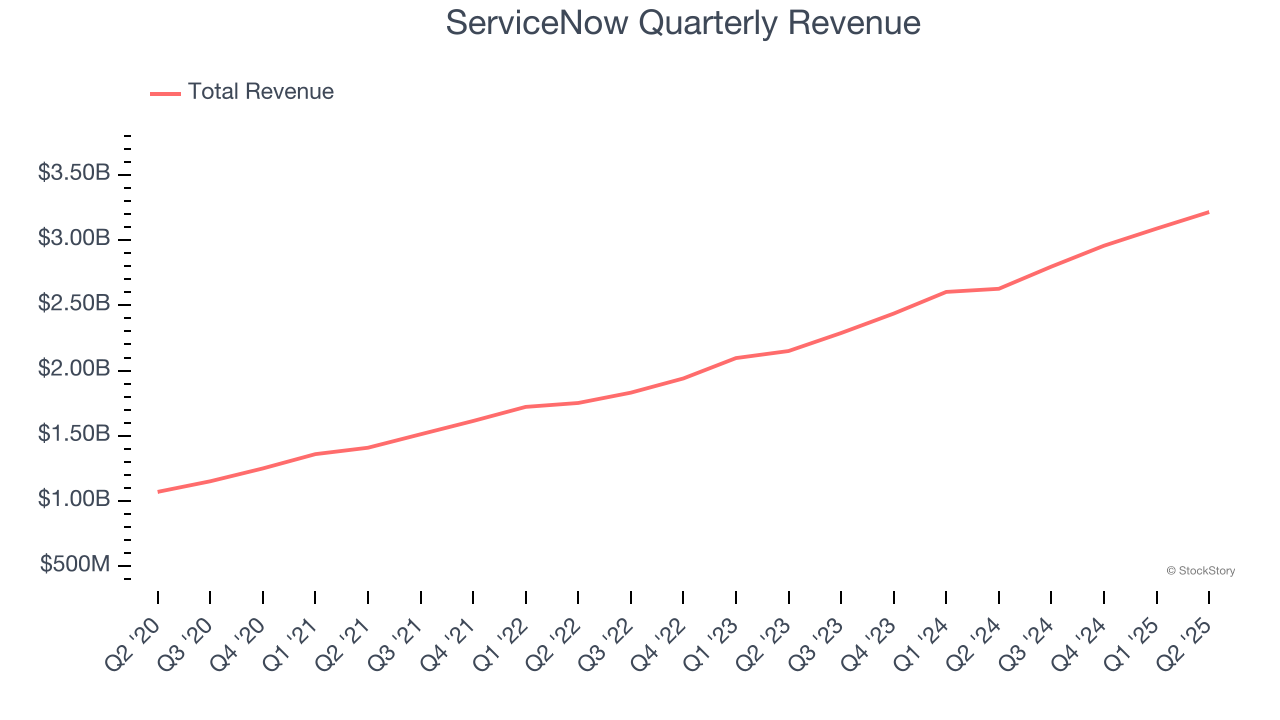

Enterprise workflow software maker ServiceNow (NYSE: NOW) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 22.4% year on year to $3.22 billion. Its non-GAAP profit of $4.09 per share was 14.6% above analysts’ consensus estimates.

Is now the time to buy ServiceNow? Find out by accessing our full research report, it’s free.

ServiceNow (NOW) Q2 CY2025 Highlights:

- Revenue: $3.22 billion vs analyst estimates of $3.12 billion (22.4% year-on-year growth, 2.9% beat)

- Adjusted EPS: $4.09 vs analyst estimates of $3.57 (14.6% beat)

- Adjusted Operating Income: $955 million vs analyst estimates of $846.5 million (29.7% margin, 12.8% beat)

- The company provided subscription revenue guidance for the full year of $12.79 billion at the midpoint (beat)

- Total RPO: $23.9 billion vs analyst estimates of $22.5 billion (6.5% beat, current RPO also beat)

- Operating Margin: 11.1%, up from 9.1% in the same quarter last year

- Free Cash Flow Margin: 16.6%, down from 47.7% in the previous quarter

- Market Capitalization: $199.6 billion

“ServiceNow’s outstanding second quarter results continue our long track record of elite level execution,” said ServiceNow Chairman and CEO Bill McDermott.

Company Overview

Founded by Fred Luddy, who coded the company's initial prototype on a flight from San Francisco to London, ServiceNow (NYSE: NOW) is a software provider helping companies automate workflows across IT, HR, and customer service.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, ServiceNow’s 22.2% annualized revenue growth over the last three years was decent. Its growth was slightly above the average software company and shows its offerings resonate with customers.

This quarter, ServiceNow reported robust year-on-year revenue growth of 22.4%, and its $3.22 billion of revenue topped Wall Street estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to grow 17.8% over the next 12 months, a deceleration versus the last three years. We still think its growth trajectory is attractive given its scale and implies the market sees success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

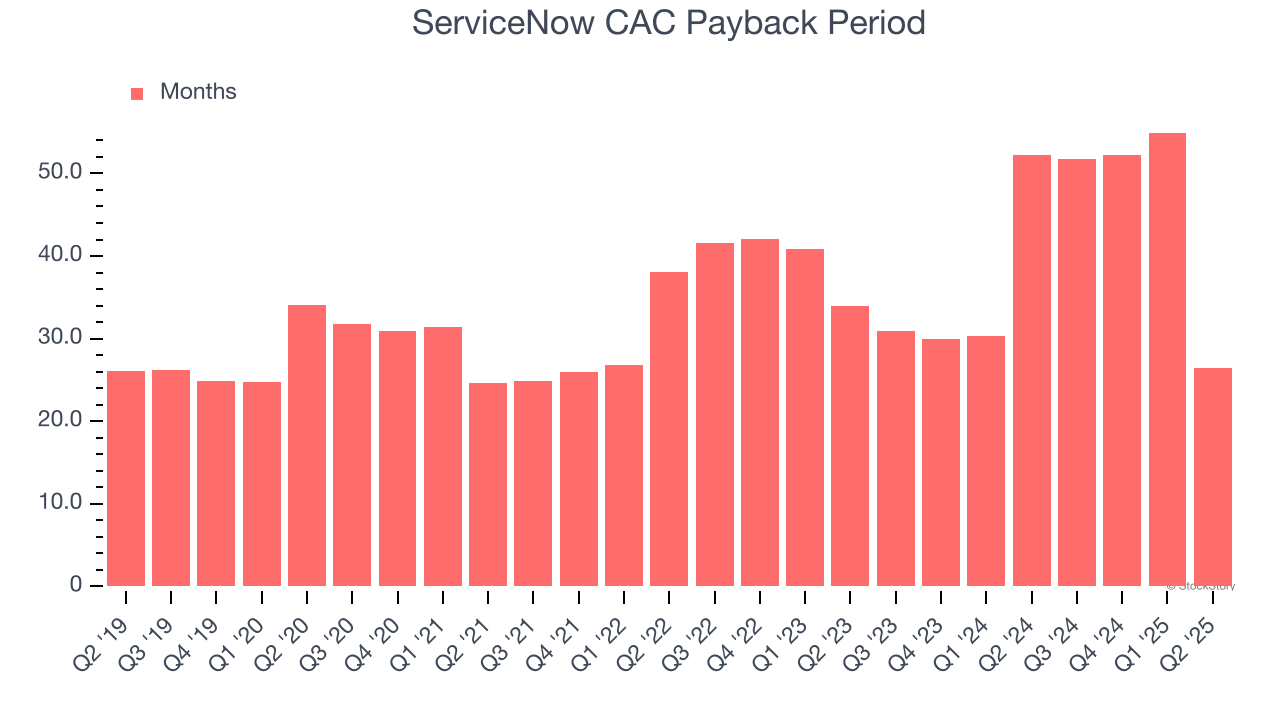

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

ServiceNow is very efficient at acquiring new customers, and its CAC payback period checked in at 26.5 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation due to its scale. These dynamics give ServiceNow more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from ServiceNow’s Q2 Results

It was encouraging to see ServiceNow beat analysts’ revenue expectations this quarter. RPO or remaining performance obligations, which is a leading indicator of future revenue, also beat handily. Moving down to margins, the company achieved more operating leverage than expected and beat on the operating profit line by a more convincing amount than its revenue beat. Looking ahead, full-year subscription revenue was encouraging and ahead of Wall Street's estimates. Overall, this print was very strong with little to pick on, showing that enterprise demand for digitization is healthy and ServiceNow's offerings are resonating. The stock traded up 6.4% to $1,017 immediately after reporting.

Indeed, ServiceNow had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.