Penguin Solutions has gotten torched over the last six months - since July 2025, its stock price has dropped 21.6% to $19.37 per share. This may have investors wondering how to approach the situation.

Is now the time to buy Penguin Solutions, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Penguin Solutions Will Underperform?

Even with the cheaper entry price, we're cautious about Penguin Solutions. Here are three reasons you should be careful with PENG and a stock we'd rather own.

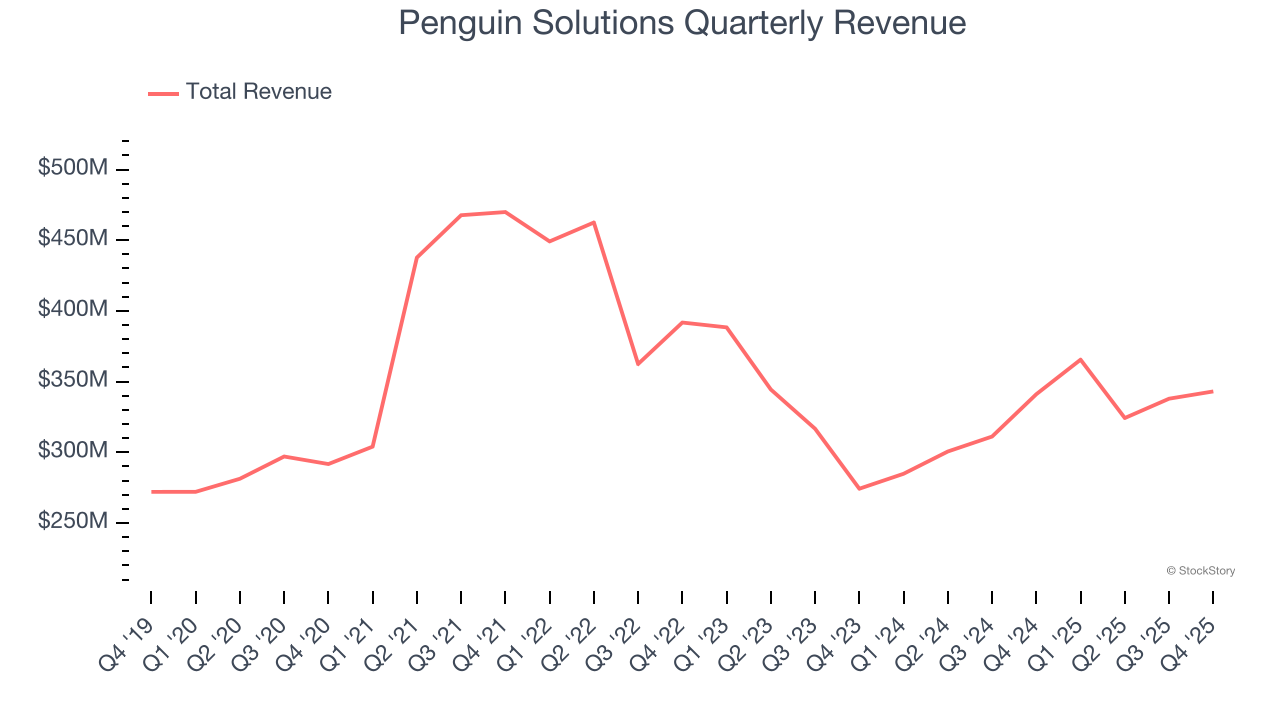

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Penguin Solutions grew its sales at a mediocre 3.7% compounded annual growth rate. This was below our standard for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

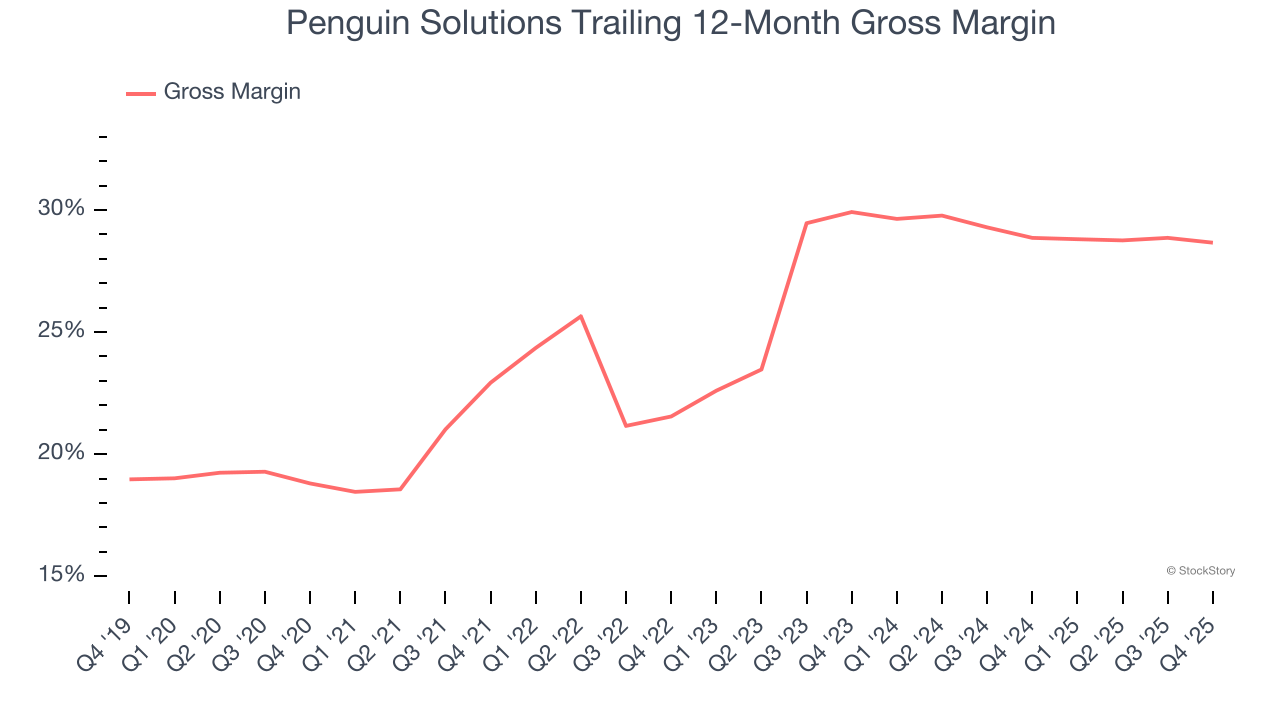

2. Low Gross Margin Reveals Weak Structural Profitability

In the semiconductor industry, a company’s gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Penguin Solutions’s gross margin is one of the worst in the semiconductor industry, signaling it operates in a competitive market and lacks pricing power. As you can see below, it averaged a 28.8% gross margin over the last two years. That means Penguin Solutions paid its suppliers a lot of money ($71.25 for every $100 in revenue) to run its business.

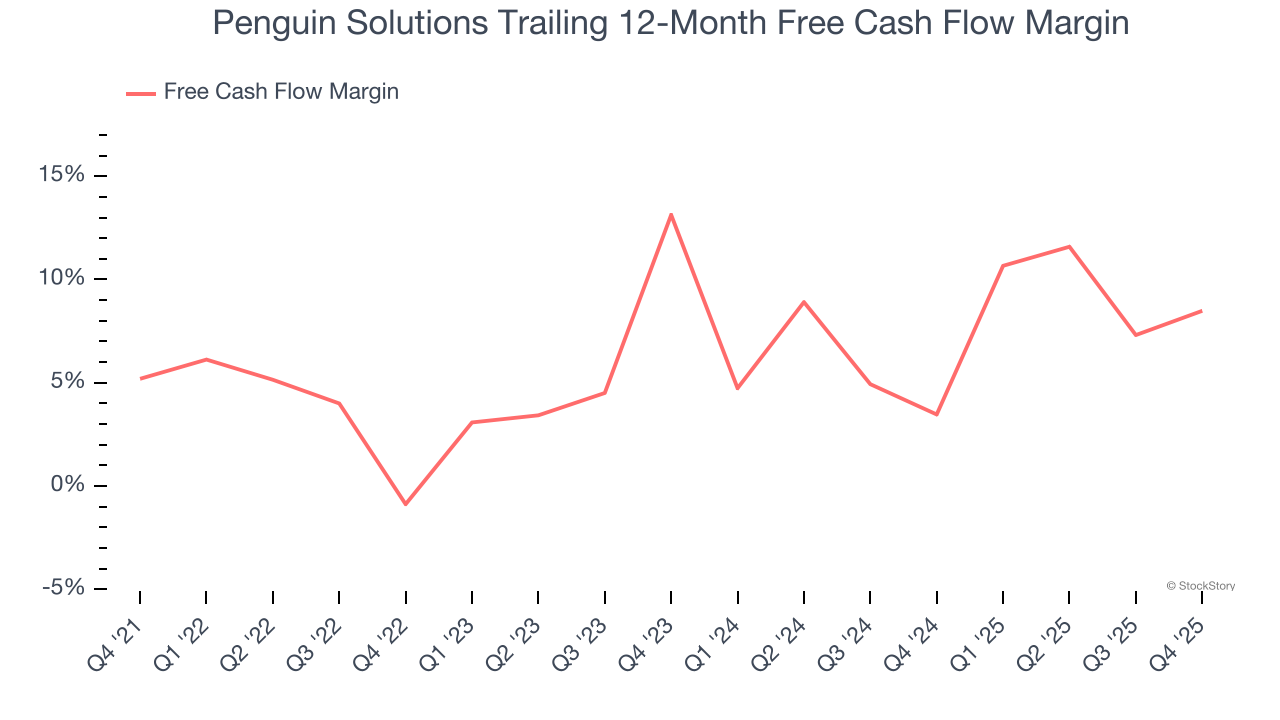

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Penguin Solutions has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 6.1%, lousy for a semiconductor business.

Final Judgment

We cheer for all companies solving complex technology issues, but in the case of Penguin Solutions, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 9× forward P/E (or $19.37 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d suggest looking at the Amazon and PayPal of Latin America.

Stocks We Like More Than Penguin Solutions

Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.