What a fantastic six months it’s been for Green Plains. Shares of the company have skyrocketed 88.1%, hitting $16.54. This performance may have investors wondering how to approach the situation.

Is now the time to buy Green Plains, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Green Plains Will Underperform?

Despite the momentum, we're sitting this one out for now. Here are three reasons there are better opportunities than GPRE and a stock we'd rather own.

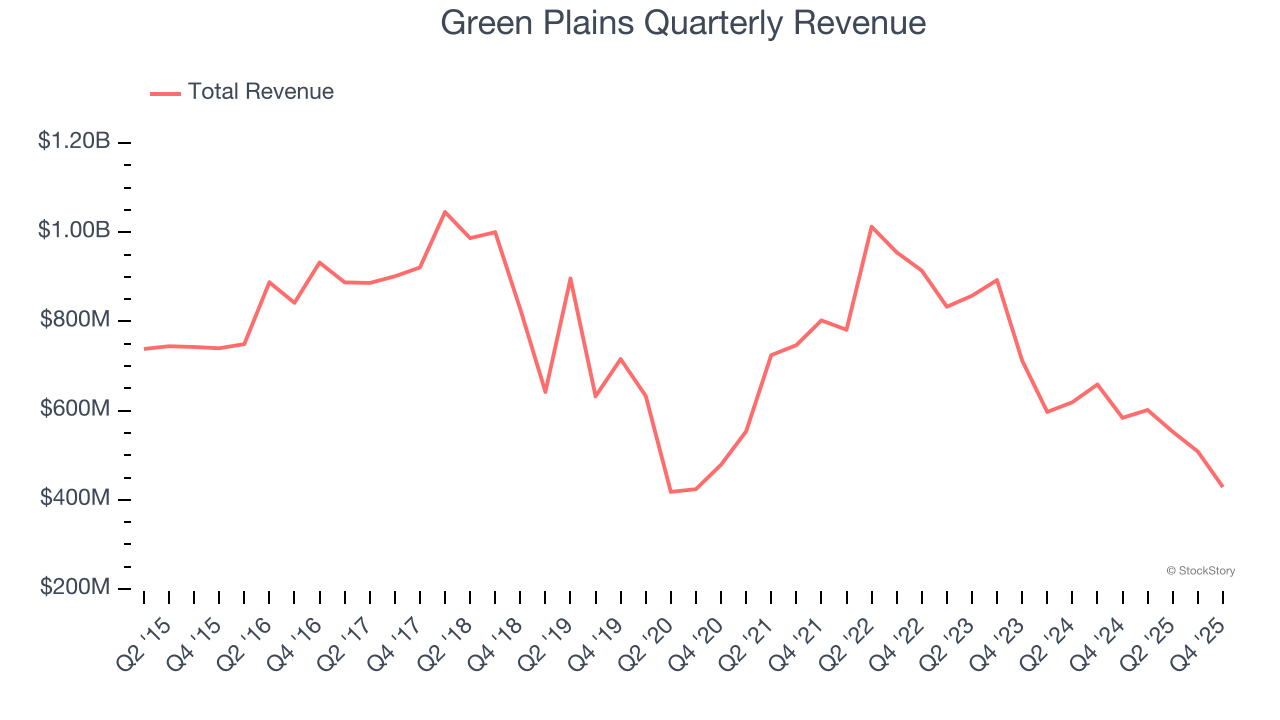

1. Long-Term Revenue Growth Disappoints

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Over the last five years, Green Plains grew its sales at a weak 1.4% compounded annual growth rate. This fell short of our benchmarks.

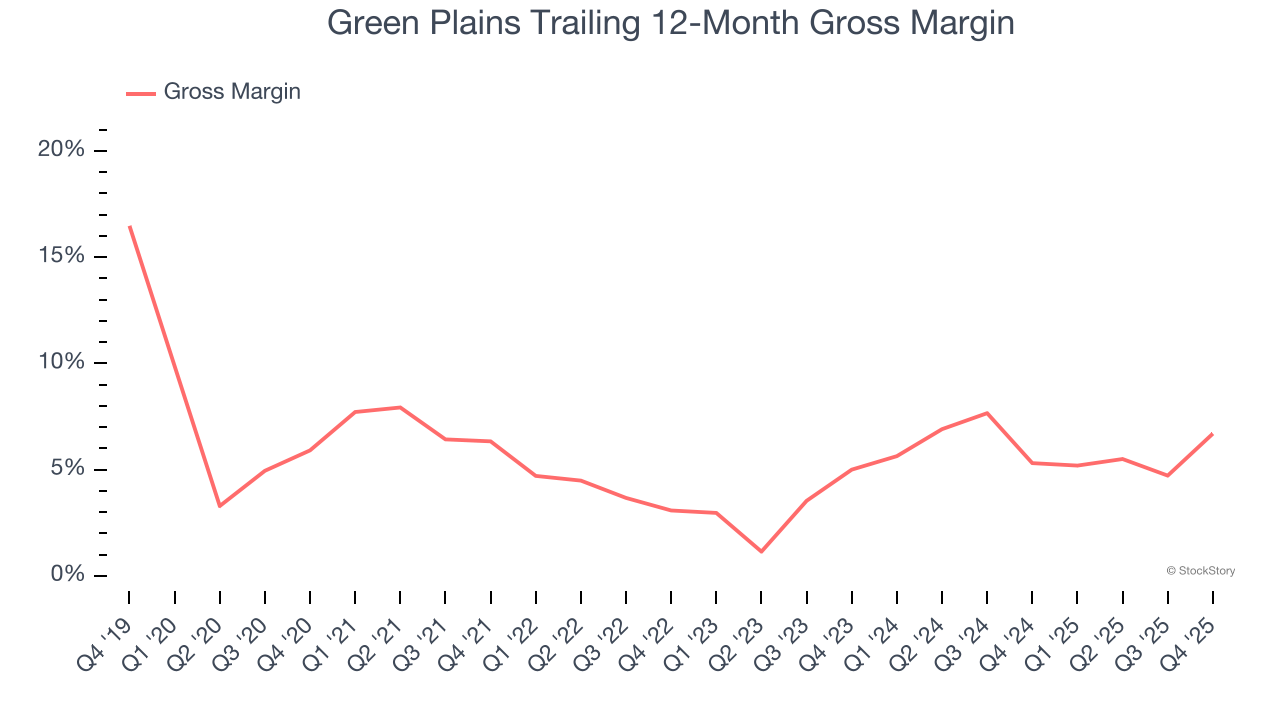

2. Low Gross Margin Reveals Weak Structural Profitability

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Green Plains, which averaged 5.1% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

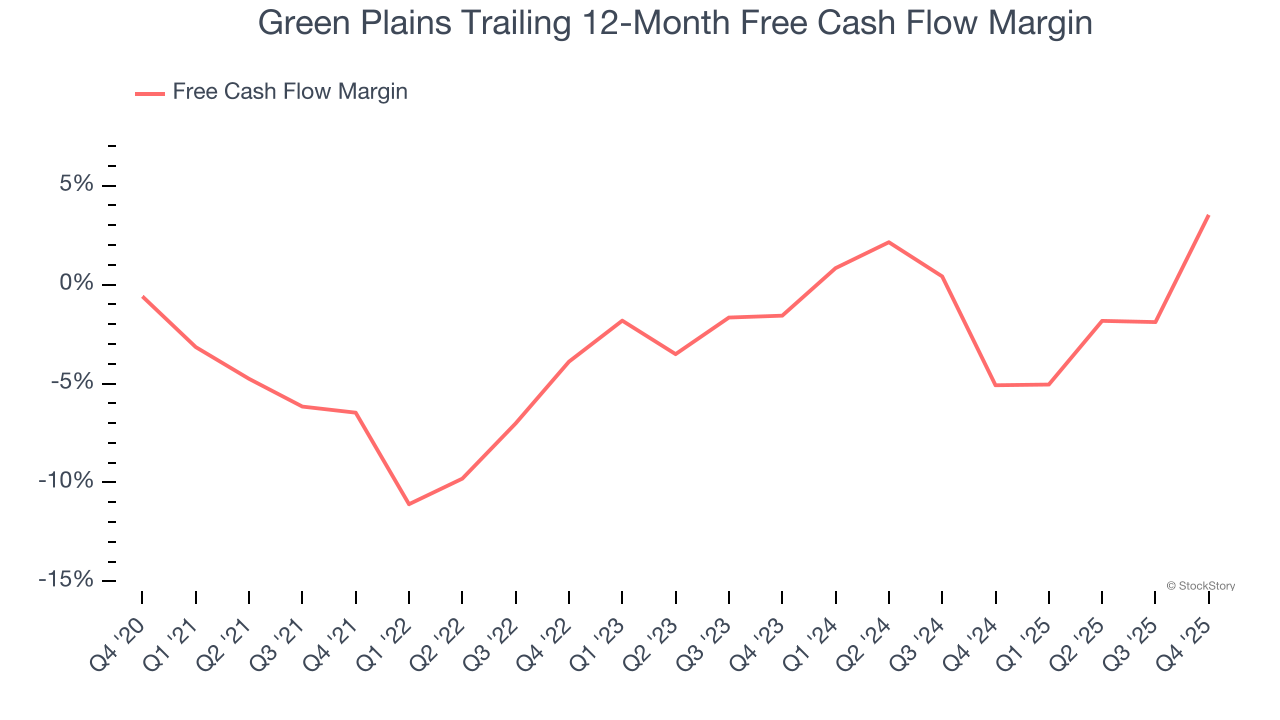

3. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Green Plains posted positive free cash flow this quarter, the broader story hasn’t been so clean. Green Plains’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 3%. This means it lit $2.99 of cash on fire for every $100 in revenue.

Final Judgment

We see the value of companies helping consumers, but in the case of Green Plains, we’re out. After the recent rally, the stock trades at 26.1× forward P/E (or $16.54 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. Let us point you toward a top digital advertising platform riding the creator economy.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.