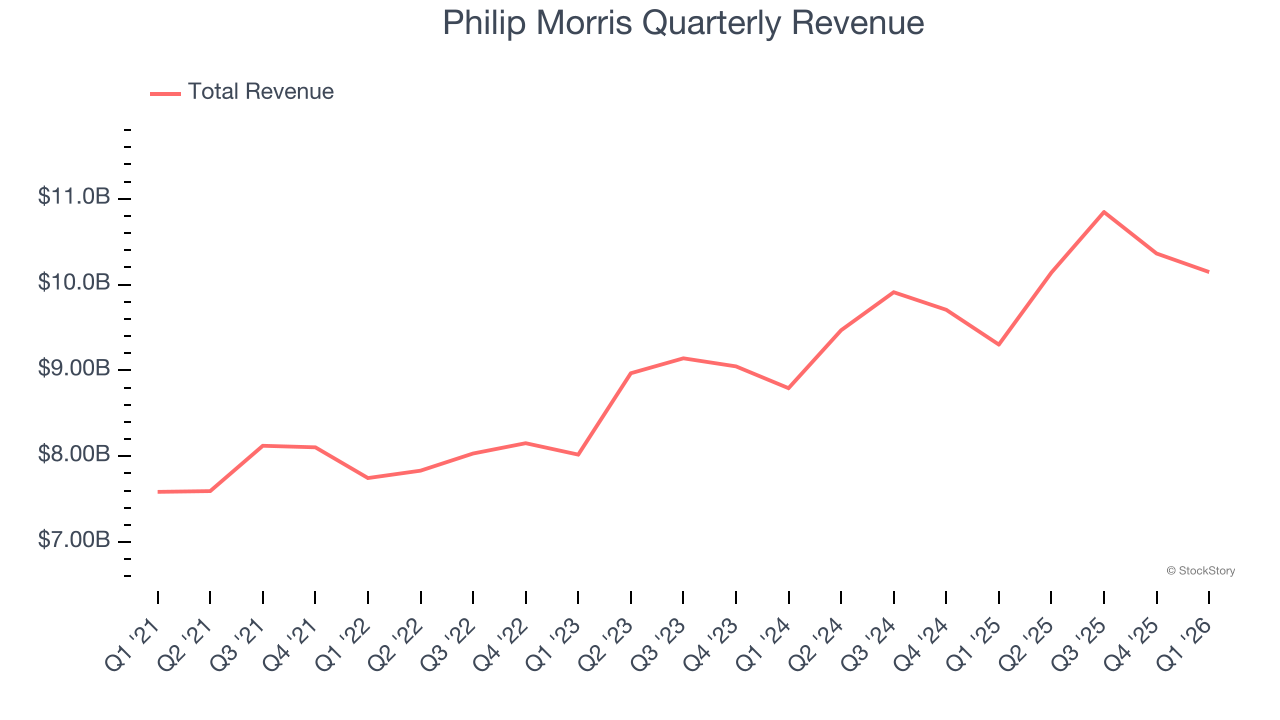

Tobacco company Philip Morris International (NYSE: PM) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 9.1% year on year to $10.15 billion. Its GAAP profit of $1.56 per share was 10.1% below analysts’ consensus estimates.

Is now the time to buy Philip Morris? Find out by accessing our full research report, it’s free.

Philip Morris (PM) Q1 CY2026 Highlights:

- Revenue: $10.15 billion vs analyst estimates of $9.98 billion (9.1% year-on-year growth, 1.7% beat)

- EPS (GAAP): $1.56 vs analyst expectations of $1.74 (10.1% miss)

- Adjusted Operating Income: $3.89 billion vs analyst estimates of $4.02 billion (38.4% margin, 3.2% miss)

- Operating Margin: 38.4%, in line with the same quarter last year

- Market Capitalization: $238.8 billion

Company Overview

Founded in 1847, Philip Morris International (NYSE: PM) manufactures and sells a wide range of tobacco and nicotine-containing products, including cigarettes, heated tobacco products, and oral nicotine pouches.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $41.49 billion in revenue over the past 12 months, Philip Morris is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have).

As you can see below, Philip Morris’s sales grew at a decent 9% compounded annual growth rate over the last three years. This shows its offerings generated slightly more demand than the average consumer staples company, a helpful starting point for our analysis.

This quarter, Philip Morris reported year-on-year revenue growth of 9.1%, and its $10.15 billion of revenue exceeded Wall Street’s estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to grow 7.1% over the next 12 months, a slight deceleration versus the last three years. We still think its growth trajectory is satisfactory given its scale and indicates the market is baking in success for its products.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Cash Is King

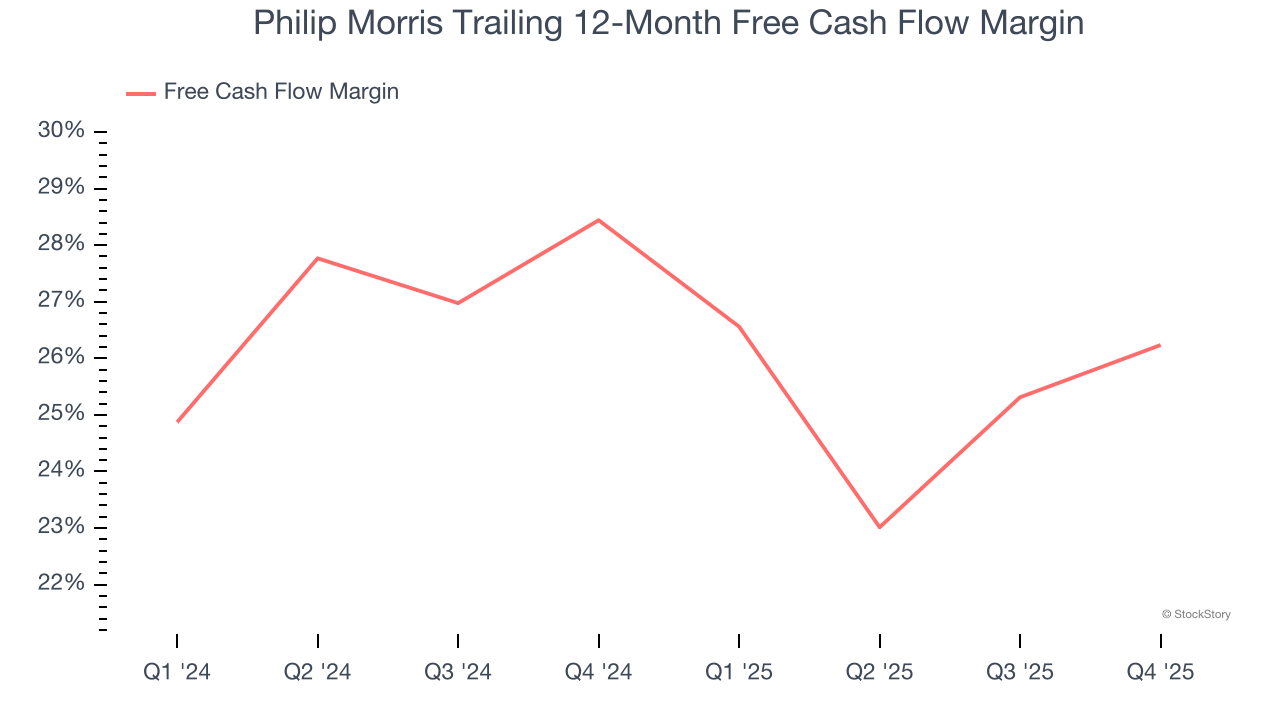

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Philip Morris has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging an eye-popping 31% over the last two years.

Key Takeaways from Philip Morris’s Q1 Results

It was encouraging to see Philip Morris beat analysts’ revenue expectations this quarter. We were also happy its gross margin narrowly outperformed Wall Street’s estimates. On the other hand, its EPS missed and its adjusted operating income fell short of Wall Street’s estimates. Overall, this quarter was mixed. The stock traded up 1.1% to $154.87 immediately following the results.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).