Food and beverage supplier MGP Ingredients (NASDAQ: MGPI) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, but sales fell by 12.5% year on year to $106.4 million. The company’s full-year revenue guidance of $490 million at the midpoint came in 0.8% above analysts’ estimates. Its non-GAAP profit of $0.15 per share was significantly above analysts’ consensus estimates.

Is now the time to buy MGP Ingredients? Find out by accessing our full research report, it’s free.

MGP Ingredients (MGPI) Q1 CY2026 Highlights:

- Revenue: $106.4 million vs analyst estimates of $105 million (12.5% year-on-year decline, 1.4% beat)

- Adjusted EPS: $0.15 vs analyst estimates of $0.04 (significant beat)

- Adjusted EBITDA: $15.01 million vs analyst estimates of $13.66 million (14.1% margin, 9.9% beat)

- The company reconfirmed its revenue guidance for the full year of $490 million at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $1.65 at the midpoint

- EBITDA guidance for the full year is $94 million at the midpoint, above analyst estimates of $90.27 million

- Operating Margin: -163%, down from -0.6% in the same quarter last year

- Free Cash Flow Margin: 1.2%, down from 20.4% in the same quarter last year

- Market Capitalization: $431.9 million

Company Overview

Headquartered in Atchison, Kansas, MGP Ingredients (NASDAQ: MGPI) is a leading supplier of high-quality ingredients to the food and beverage industry

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $521.1 million in revenue over the past 12 months, MGP Ingredients is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

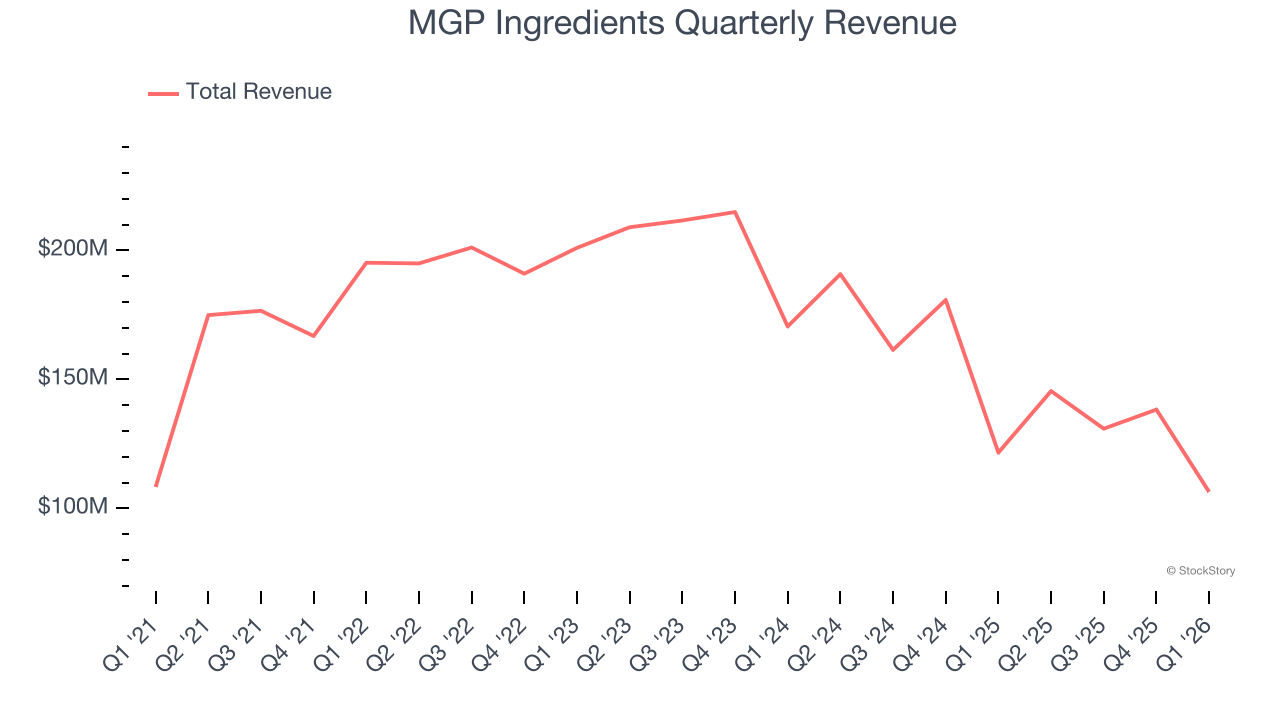

As you can see below, MGP Ingredients struggled to generate demand over the last three years. Its sales dropped by 12.9% annually, a tough starting point for our analysis.

This quarter, MGP Ingredients’s revenue fell by 12.5% year on year to $106.4 million but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to decline by 5.4% over the next 12 months. it’s hard to get excited about a company that is struggling with demand.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

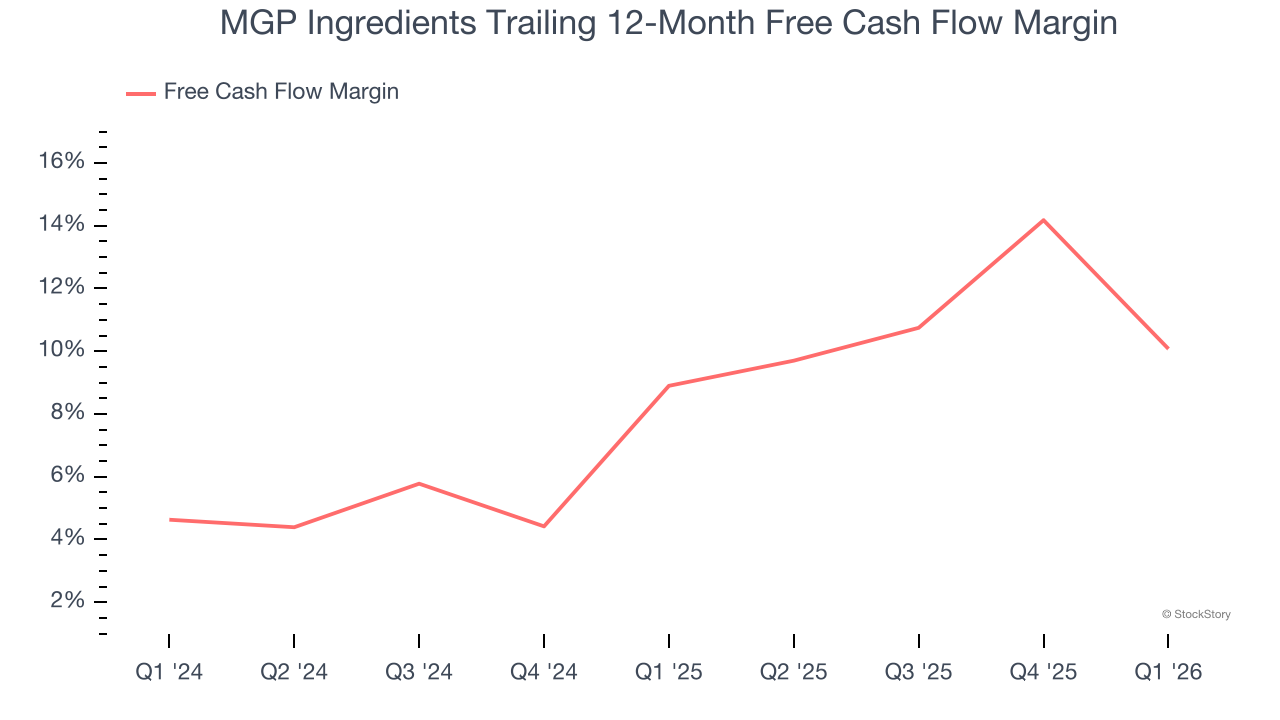

MGP Ingredients has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.4% over the last two years, quite impressive for a consumer staples business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that MGP Ingredients’s margin expanded by 1.2 percentage points over the last year. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

MGP Ingredients’s free cash flow clocked in at $1.23 million in Q1, equivalent to a 1.2% margin. The company’s cash profitability regressed as it was 19.2 percentage points lower than in the same quarter last year. This warrants extra attention because consumer staples companies typically produce more consistent and defensive performance.

Key Takeaways from MGP Ingredients’s Q1 Results

It was good to see MGP Ingredients beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its adjusted operating income missed and its gross margin fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 2.5% to $20.72 immediately after reporting.

Sure, MGP Ingredients had a solid quarter, but if we look at the bigger picture, is this stock a buy? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).