Over the last six months, Affirm’s shares have sunk to $64.95, producing a disappointing 5.6% loss - a stark contrast to the S&P 500’s 9.7% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Affirm, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Affirm Not Exciting?

Even with the cheaper entry price, we're cautious about Affirm. Here are two reasons we avoid AFRM and a stock we'd rather own.

1. Previous Growth Initiatives Have Lost Money

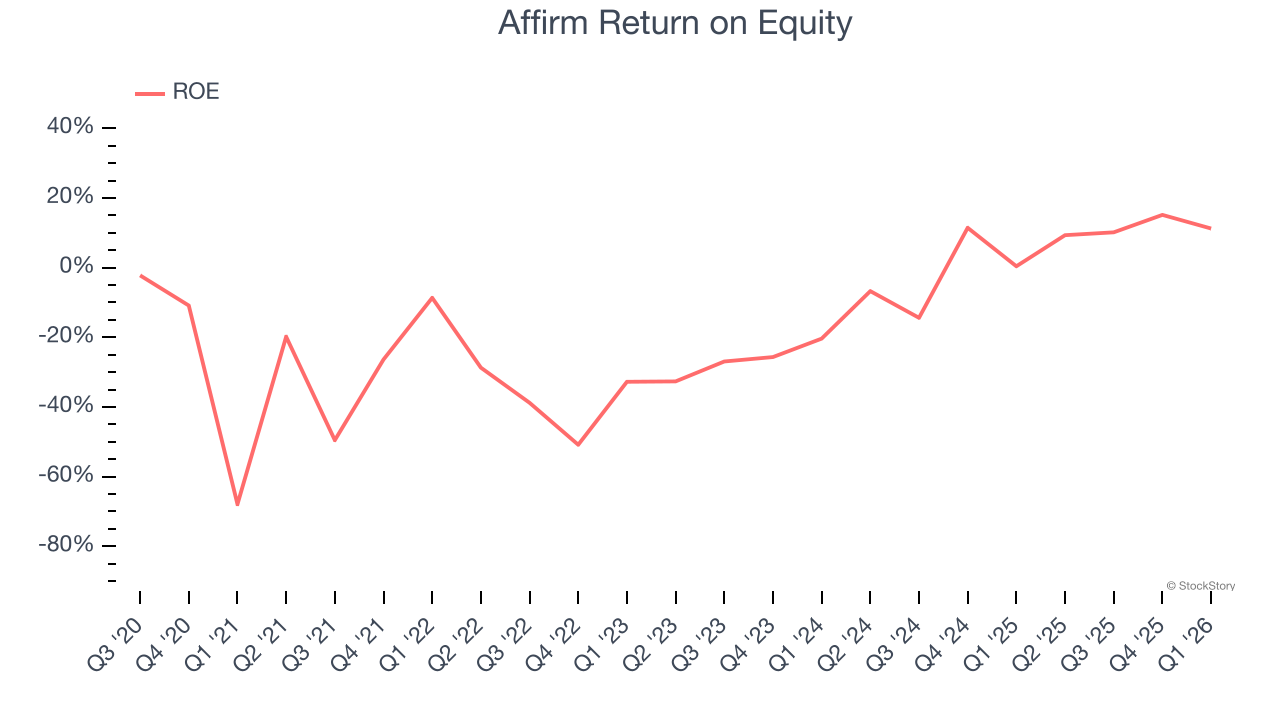

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Affirm has averaged an ROE of negative 16.2%, a bad result not only in absolute terms but also relative to the majority of firms putting up 25%+. It also shows that Affirm has little to no competitive moat.

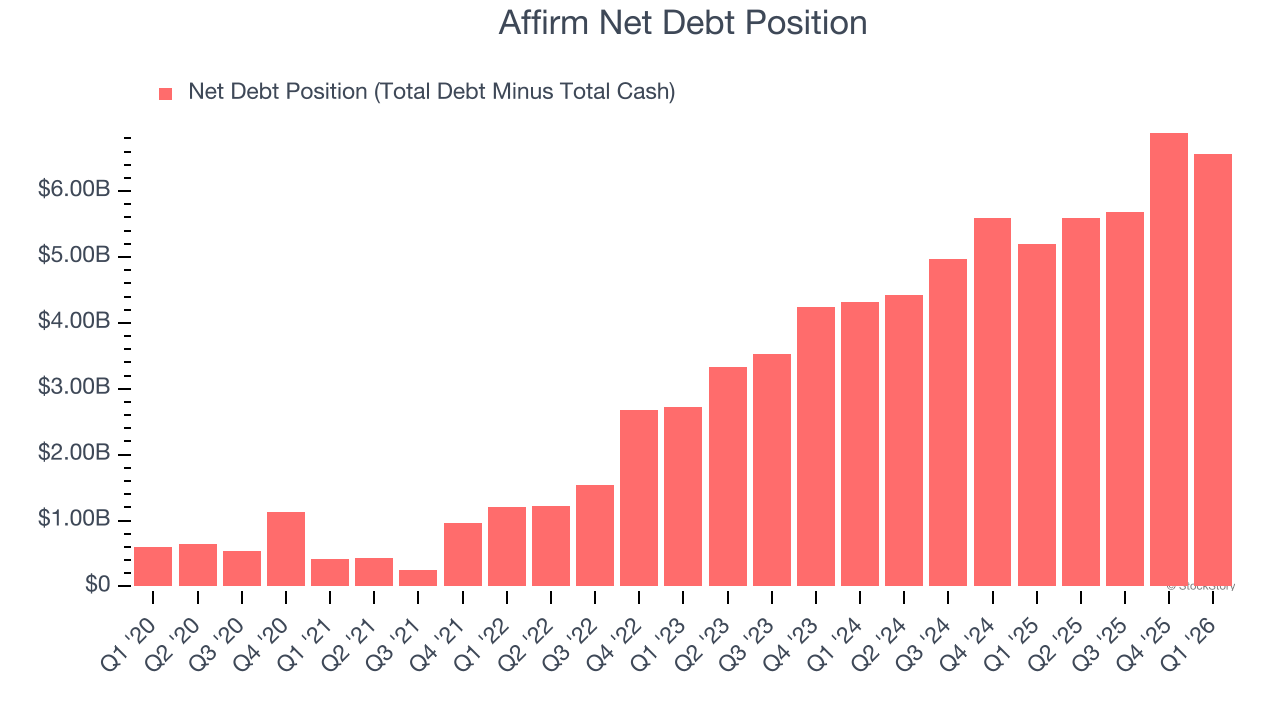

2. High Debt Levels Increase Risk

Affirm reported $2.48 billion of cash and $9.05 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $1.14 billion of EBITDA over the last 12 months, we view Affirm’s 5.8× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

Final Judgment

Affirm isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 17.1× forward P/E (or $64.95 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of Affirm

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.