What a brutal six months it’s been for Universal Health Services. The stock has dropped 35.3% and now trades at $158, rattling many shareholders. This may have investors wondering how to approach the situation.

Is now the time to buy Universal Health Services, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Universal Health Services Not Exciting?

Even though the stock has become cheaper, we're sitting this one out for now. Here are two reasons you should be careful with UHS and a stock we'd rather own.

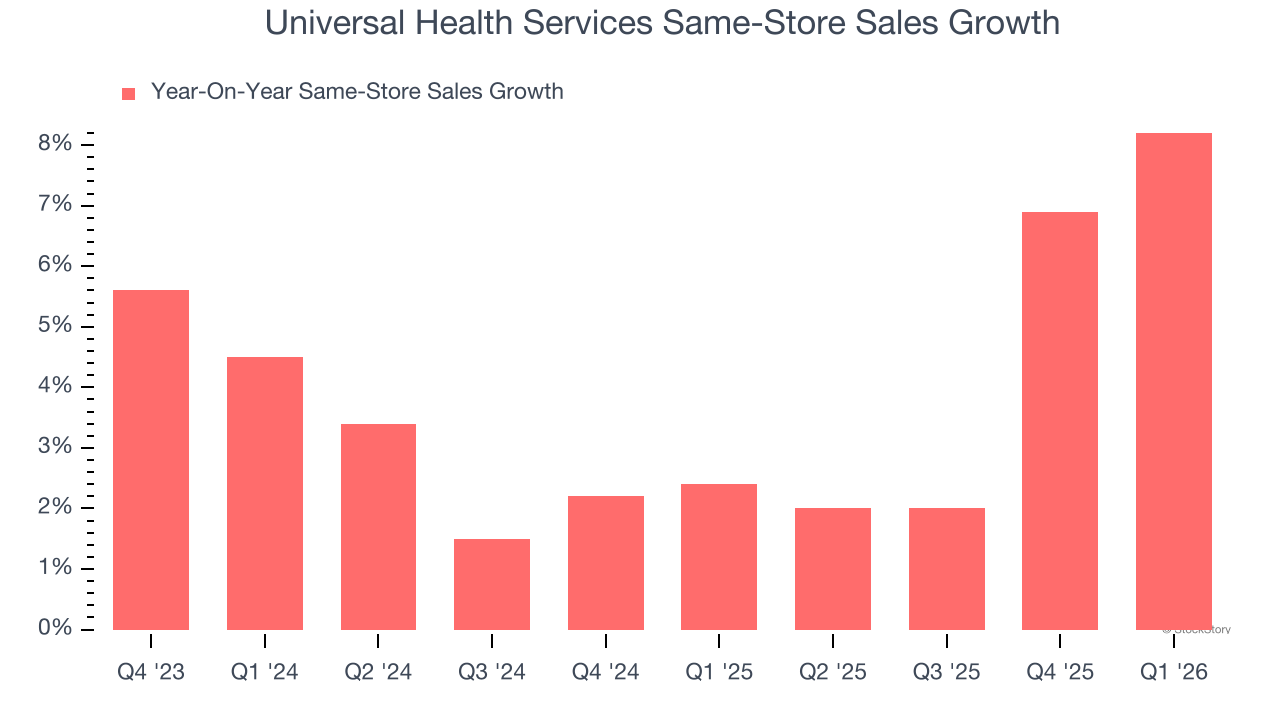

1. Same-Store Sales Falling Behind Peers

In addition to reported revenue, same-store sales are a useful data point for analyzing Hospital Chains companies. This metric measures the change in sales at brick-and-mortar locations that have existed for at least a year, giving visibility into Universal Health Services’s underlying demand characteristics.

Over the last two years, Universal Health Services’s same-store sales averaged 3.6% year-on-year growth. This performance slightly lagged the sector and suggests it might have to change its strategy or pricing, which can disrupt operations.

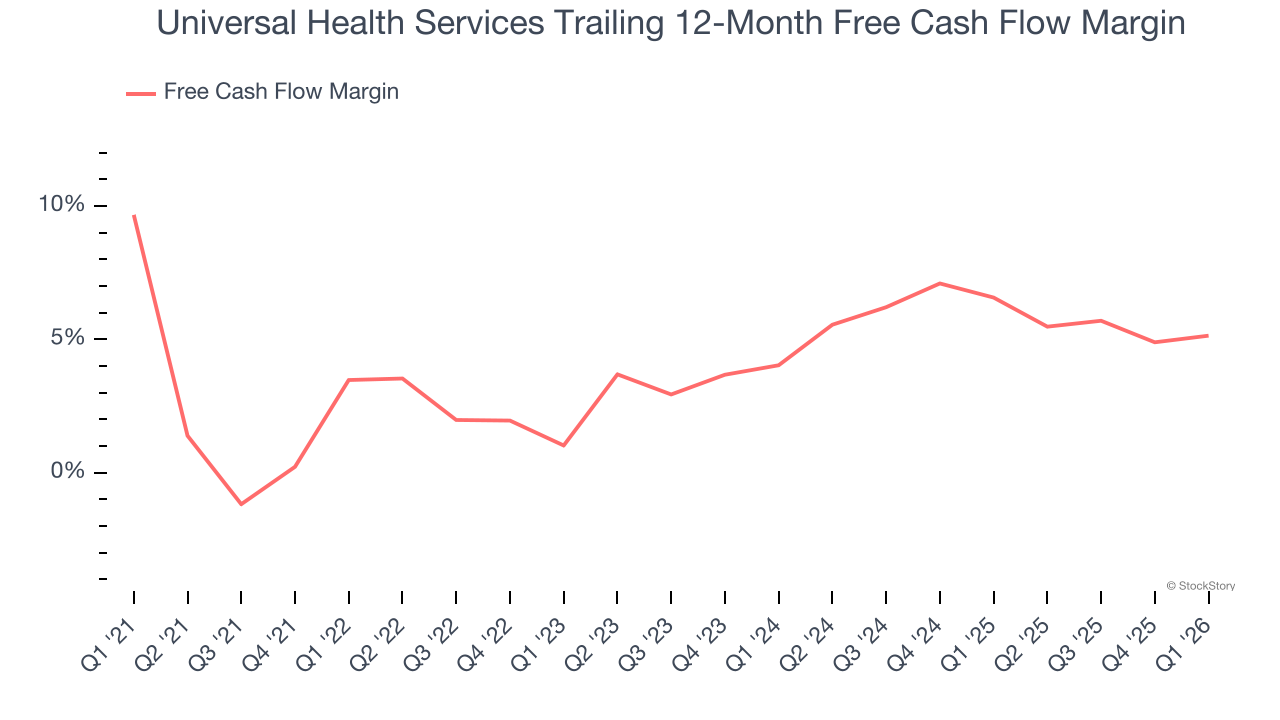

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Universal Health Services has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.2%, below what we’d expect for a healthcare business.

Final Judgment

Universal Health Services isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 6.6× forward P/E (or $158 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. Let us point you toward the most dominant software business in the world.

Stocks We Like More Than Universal Health Services

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.