Over the past six months, Armstrong World’s stock price fell to $157.42. Shareholders have lost 17.5% of their capital, which is disappointing considering the S&P 500 has climbed by 9.7%. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Following the drawdown, is this a buying opportunity for AWI? Find out in our full research report, it’s free.

Why Is AWI a Good Business?

Started as a two-man shop dating back to the 1860s, Armstrong (NYSE: AWI) provides ceiling and wall products to commercial and residential spaces.

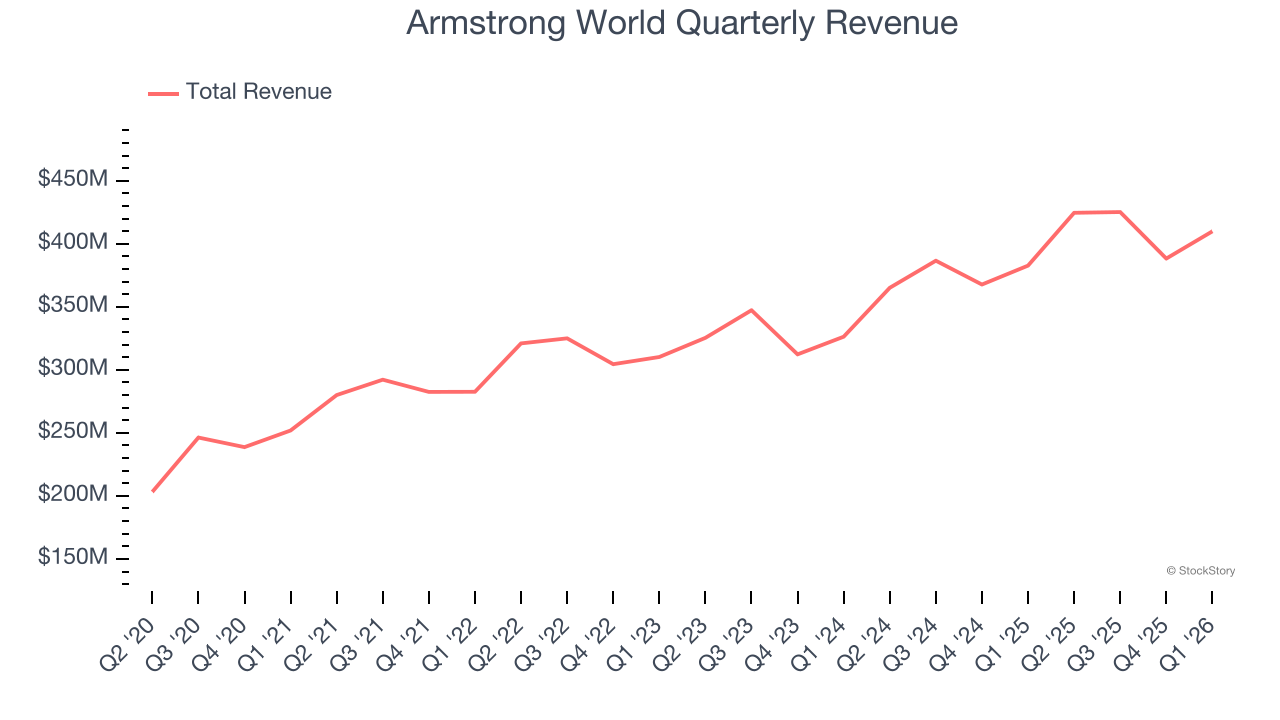

1. Skyrocketing Revenue Shows Strong Momentum

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Armstrong World’s 11.9% annualized revenue growth over the last five years was impressive. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

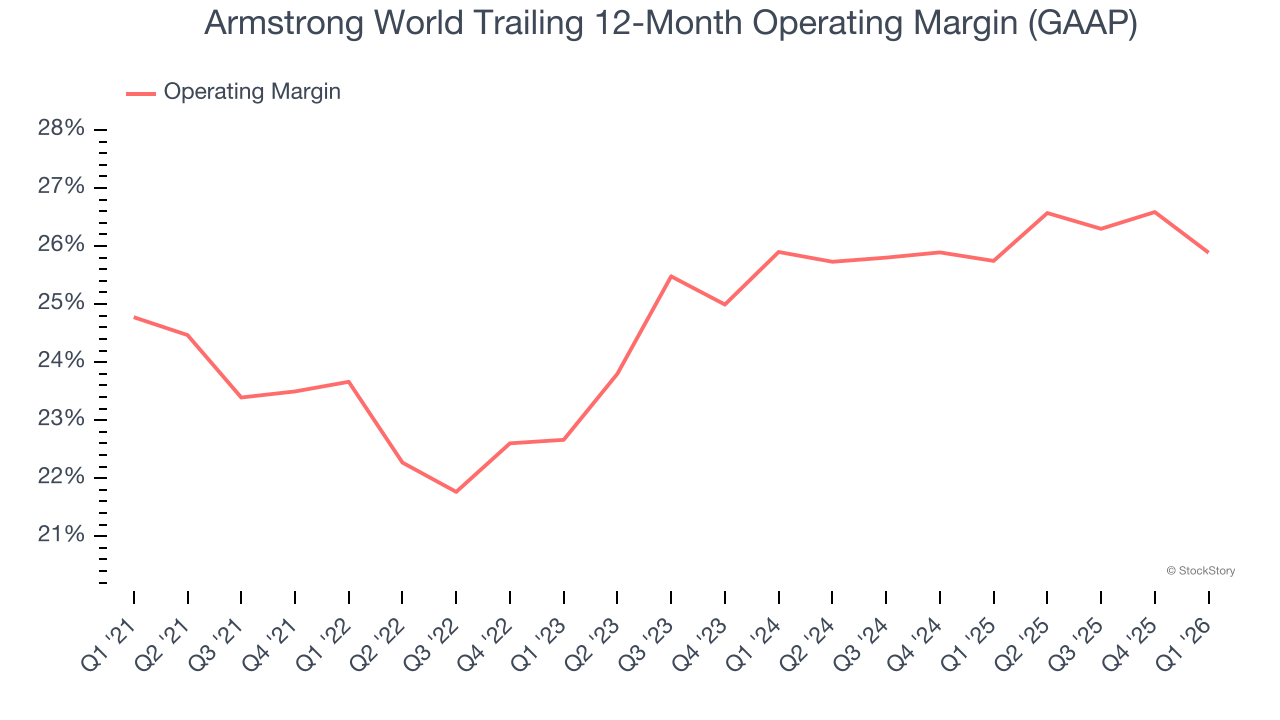

2. Operating Margin Reveals a Well-Run Organization

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Armstrong World has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 24.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

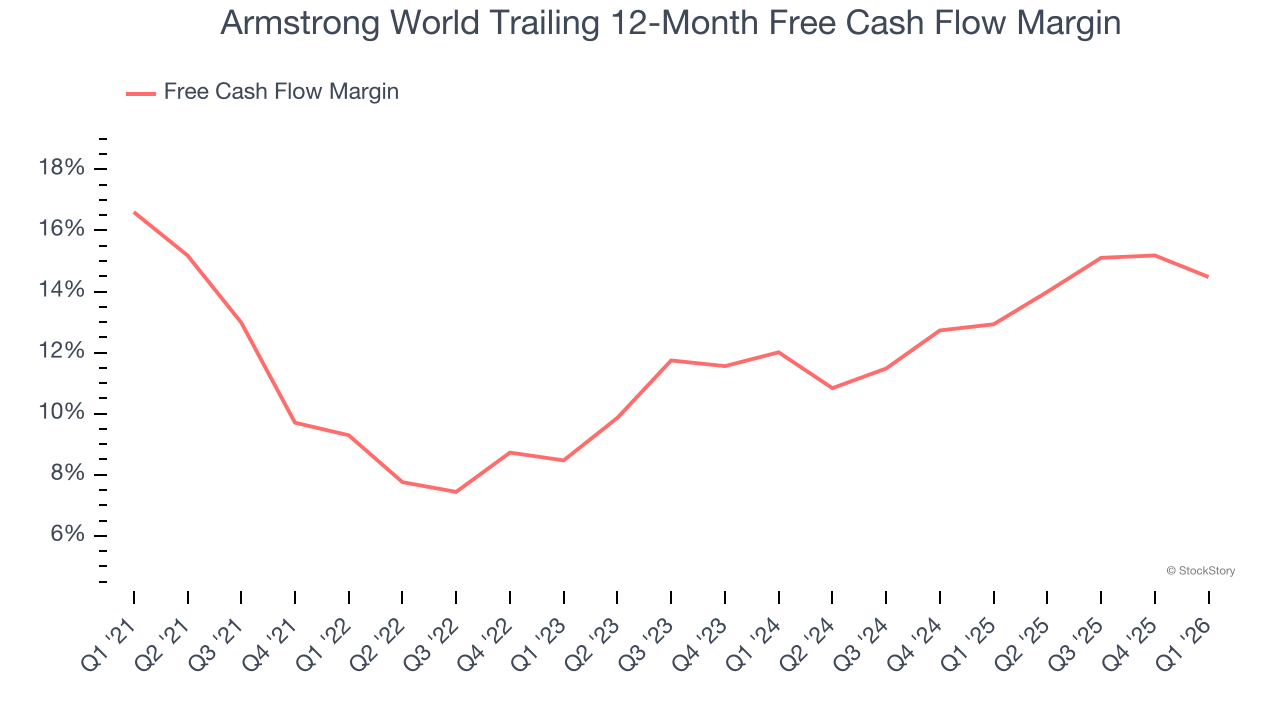

3. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Armstrong World’s margin expanded by 5.2 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Armstrong World’s free cash flow margin for the trailing 12 months was 14.5%.

Final Judgment

These are just a few reasons why Armstrong World ranks near the top of our list. After the recent drawdown, the stock trades at 18.2× forward P/E (or $157.42 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Armstrong World

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.