Autoliv has been treading water for the past six months, recording a small return of 3.8% while holding steady at $122.73. The stock also fell short of the S&P 500’s 9.7% gain during that period.

Is now the time to buy Autoliv, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Autoliv Not Exciting?

We're sitting this one out for now. Here are three reasons why ALV doesn't excite us and a stock we'd rather own.

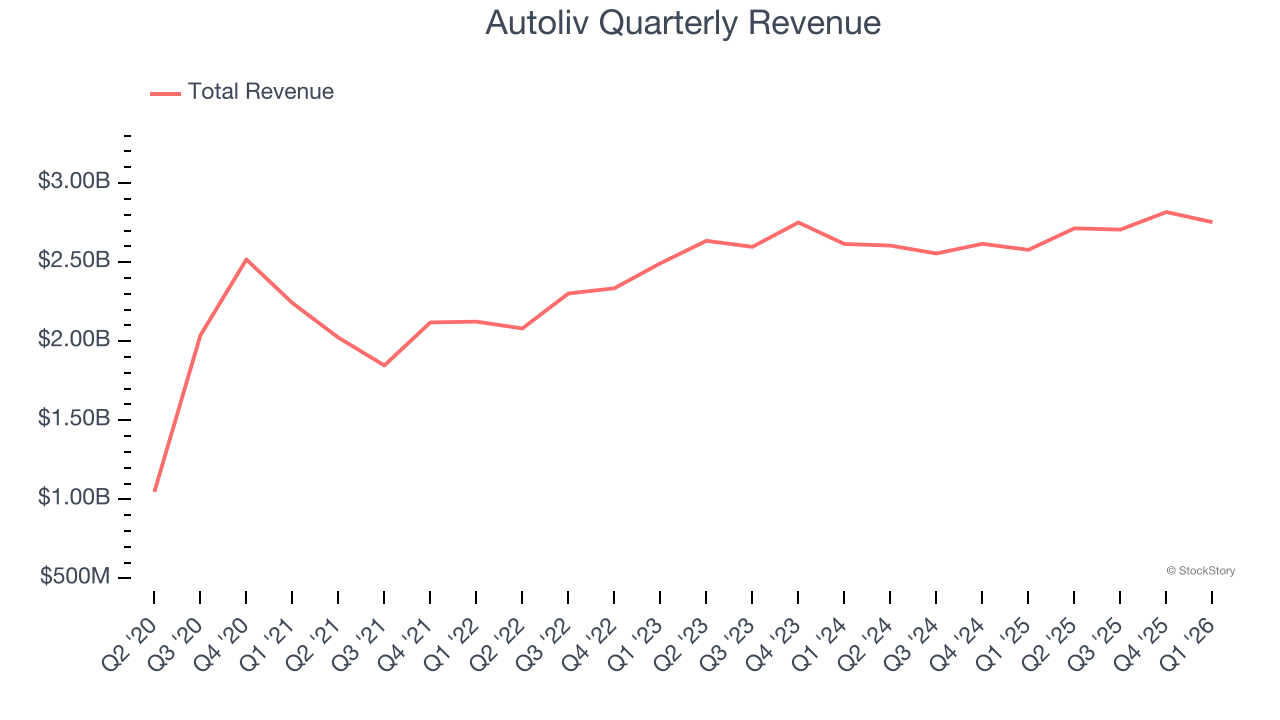

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Autoliv grew its sales at a mediocre 7% compounded annual growth rate. This was below our standard for the industrials sector.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Autoliv’s revenue to rise by 1.8%, close to its 7% annualized growth for the past five years. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

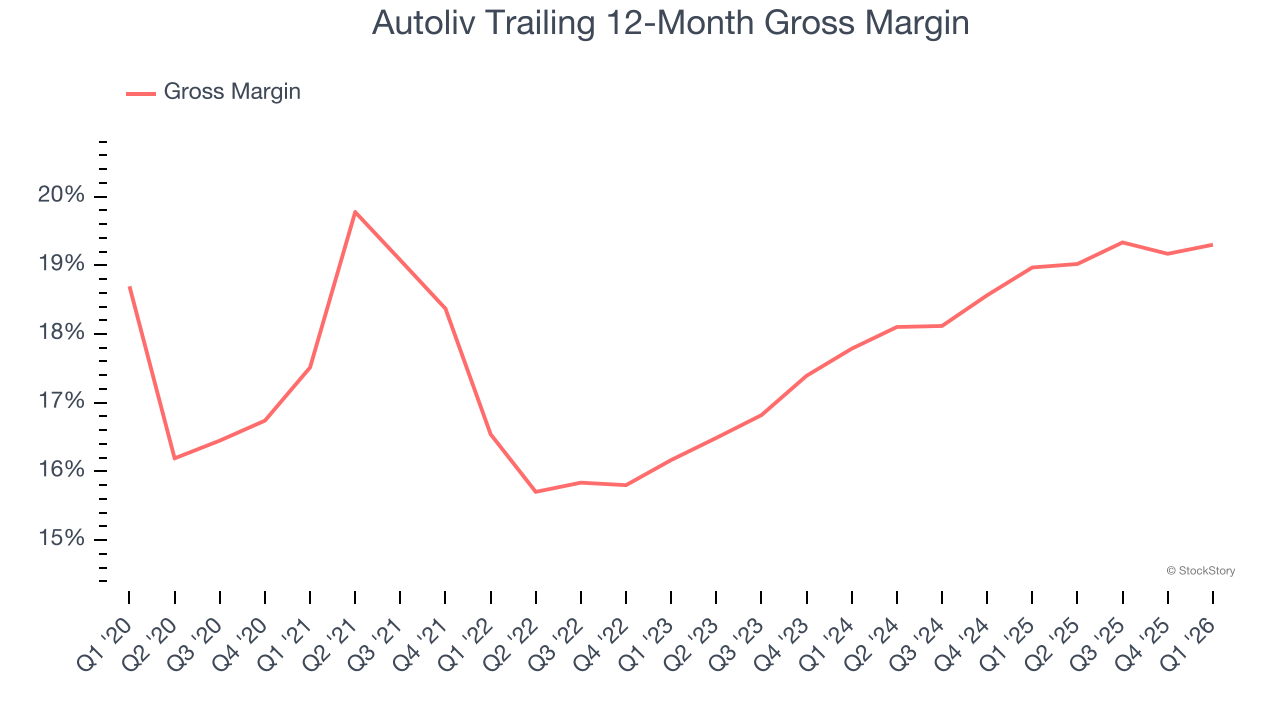

3. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Autoliv has bad unit economics for an industrials business, signaling it operates in a competitive market. This is also because it's an automobile manufacturer.

Automobile manufacturers have structurally lower profitability as they often break even on the initial sale of vehicles and instead make money on parts and servicing, which come many years later - this explains why new entrants such as Rivian, Lucid, and Nikola have negative gross margins. As you can see below, these dynamics culminated in an average 17.9% gross margin for Autoliv over the last five years.

Final Judgment

Autoliv’s business quality ultimately falls short of our standards. With its shares trailing the market in recent months, the stock trades at $122.73 per share (or a forward price-to-sales ratio of 0.8×). The market typically values companies like Autoliv based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d suggest looking at one of our top software and edge computing picks.

Stocks We Like More Than Autoliv

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.