Over the past six months, West Pharmaceutical Services has been a great trade, beating the S&P 500 by 21.8%. Its stock price has climbed to $353.68, representing a healthy 30.1% increase. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy West Pharmaceutical Services, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is West Pharmaceutical Services Not Exciting?

We’re glad investors have benefited from the price increase, but we’re swiping left on West Pharmaceutical Services for now. Here are three reasons we avoid WST, plus one stock we’d rather own.

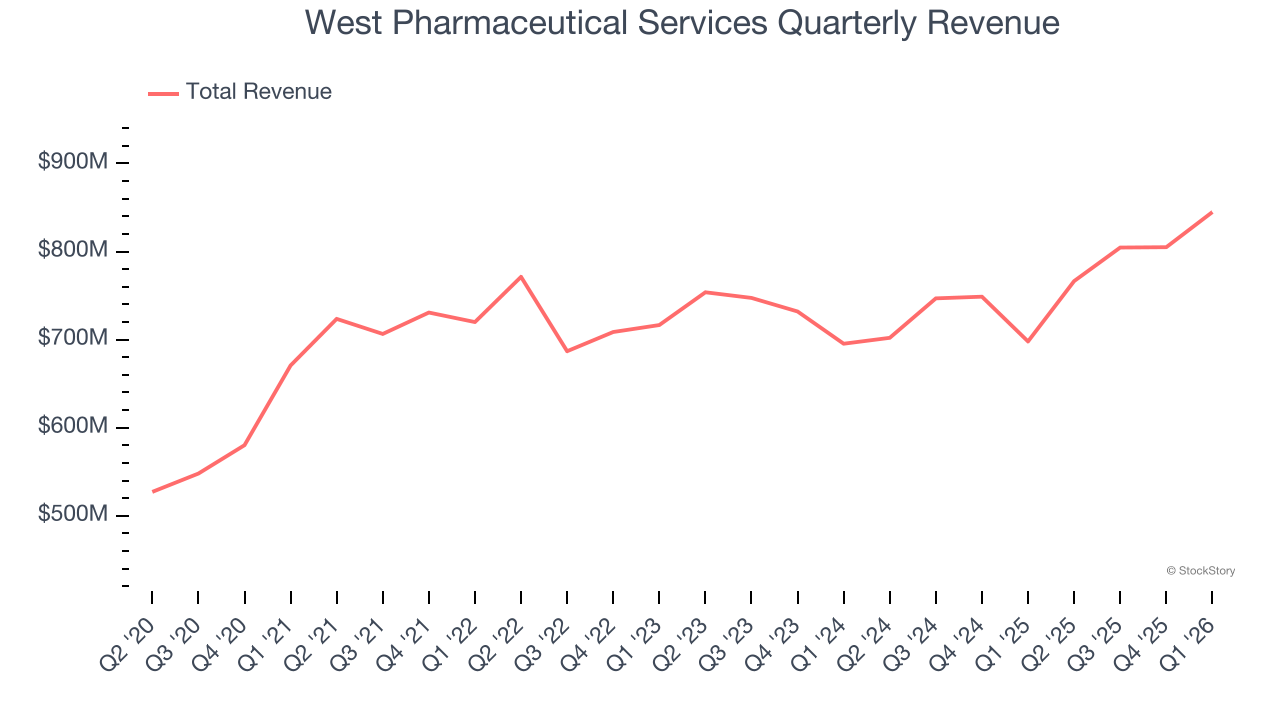

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, West Pharmaceutical Services’s sales grew at a mediocre 6.7% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector.

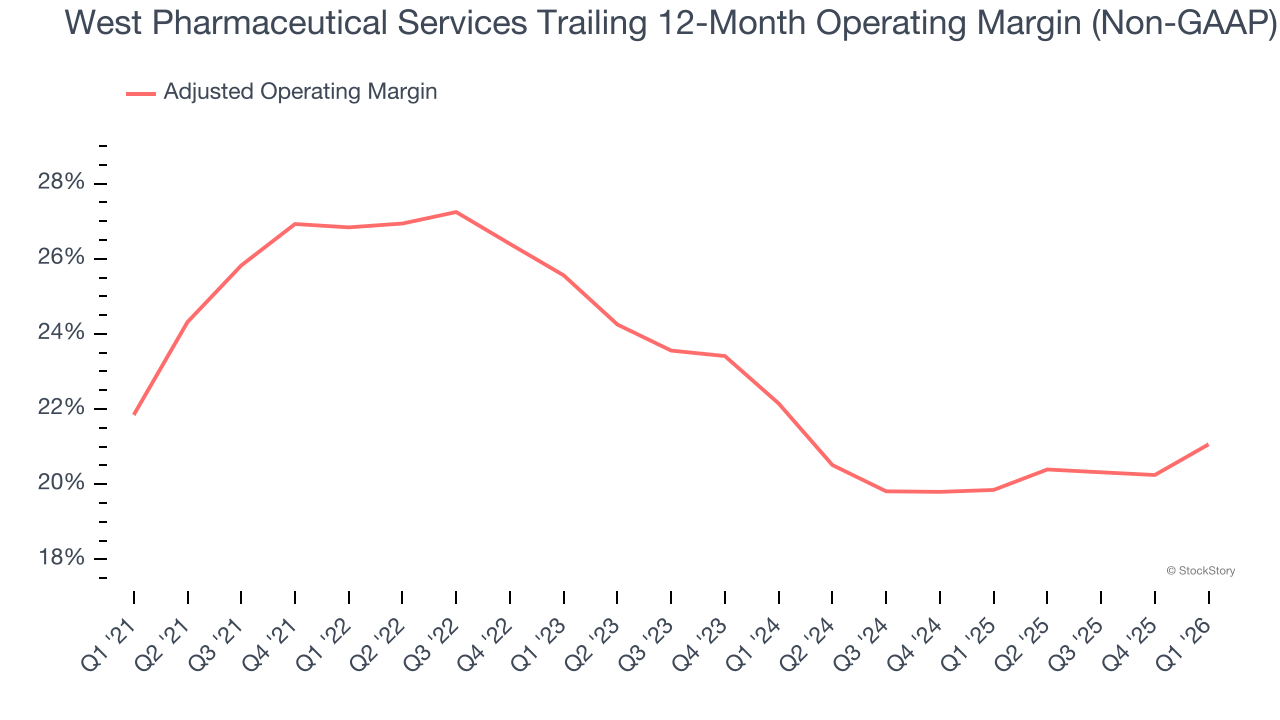

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Analyzing the trend in its profitability, West Pharmaceutical Services’s adjusted operating margin decreased by 5.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 21.1%.

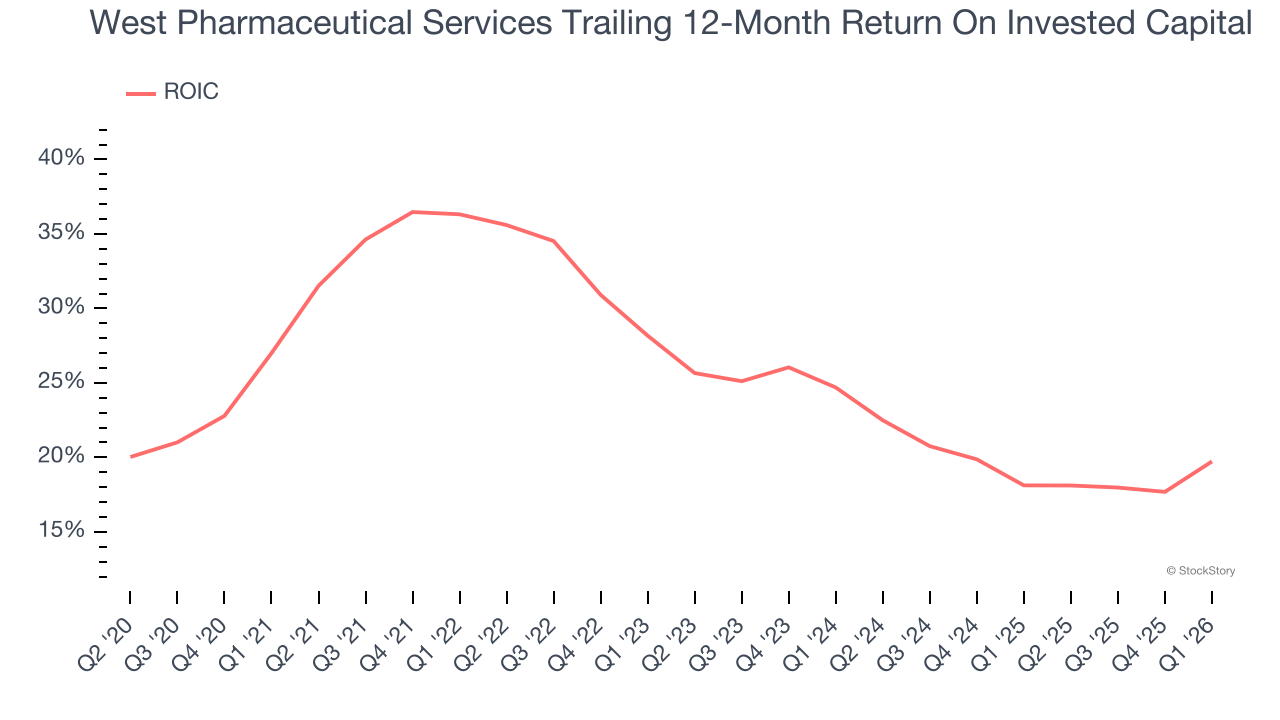

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Over the last few years, West Pharmaceutical Services’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

West Pharmaceutical Services’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 41× forward P/E (or $353.68 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. Let us point you toward the Amazon and PayPal of Latin America.

Stocks We Like More Than West Pharmaceutical Services

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.