Over the past six months, Agilent’s stock price fell to $134.31. Shareholders have lost 8.2% of their capital, which is disappointing considering the S&P 500 has climbed by 8.4%. This may have investors wondering how to approach the situation.

Is now the time to buy Agilent, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Agilent Not Exciting?

Even though the stock has become cheaper, we’re sitting this one out for now. Here are three reasons why there are better opportunities than A, plus one stock we’d rather own.

1. Long-Term Revenue Growth Disappoints

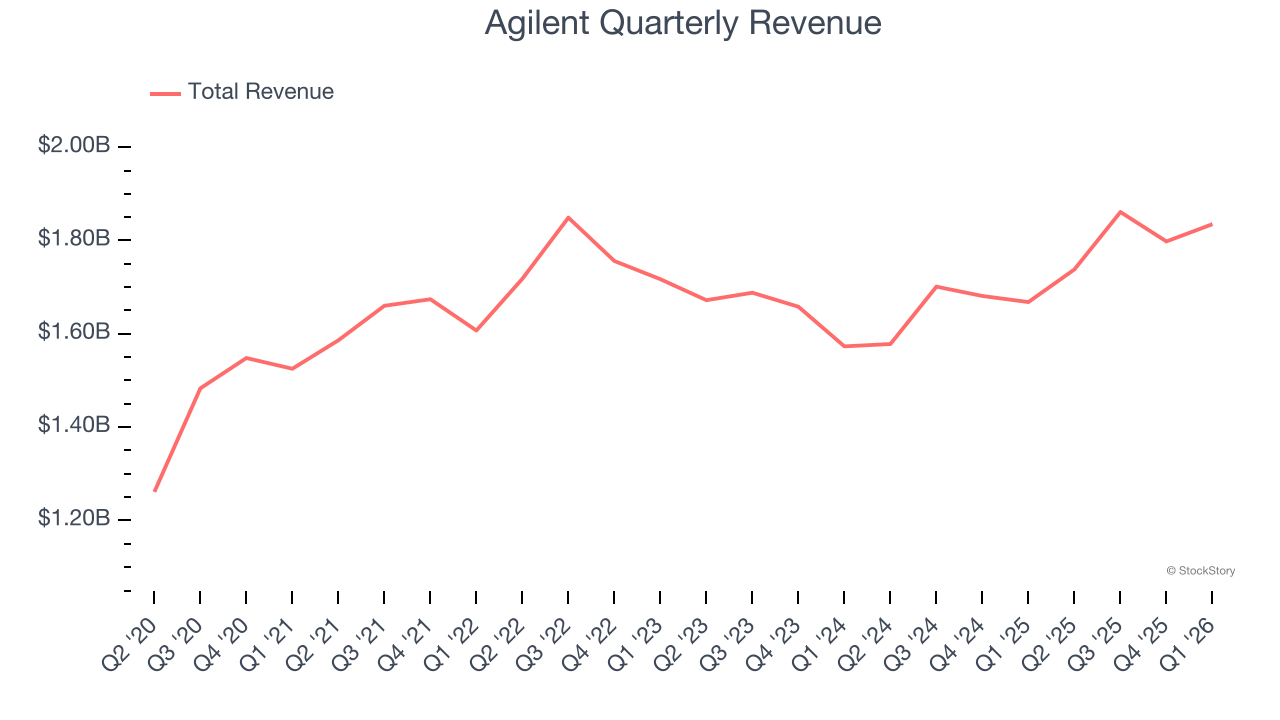

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Agilent’s sales grew at a mediocre 4.5% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector.

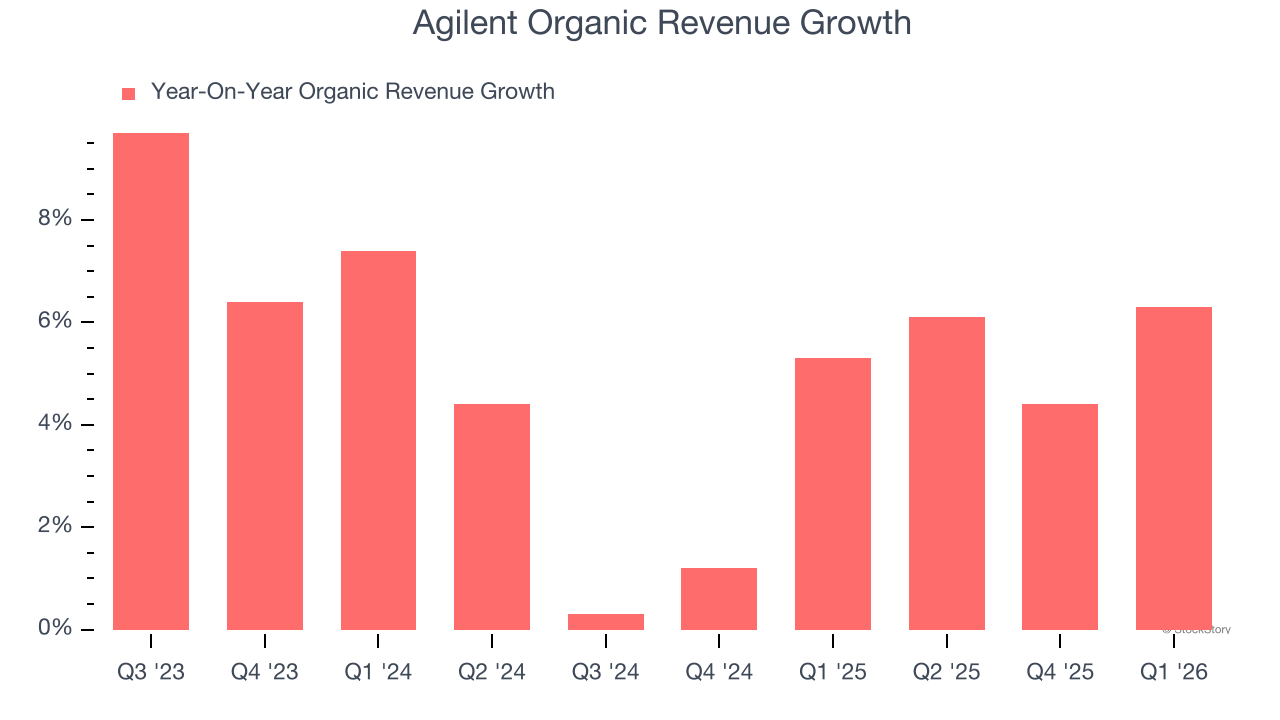

2. Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand Research Tools & Consumables companies by analyzing their organic revenue. This metric gives visibility into Agilent’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Agilent’s organic revenue averaged 4% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

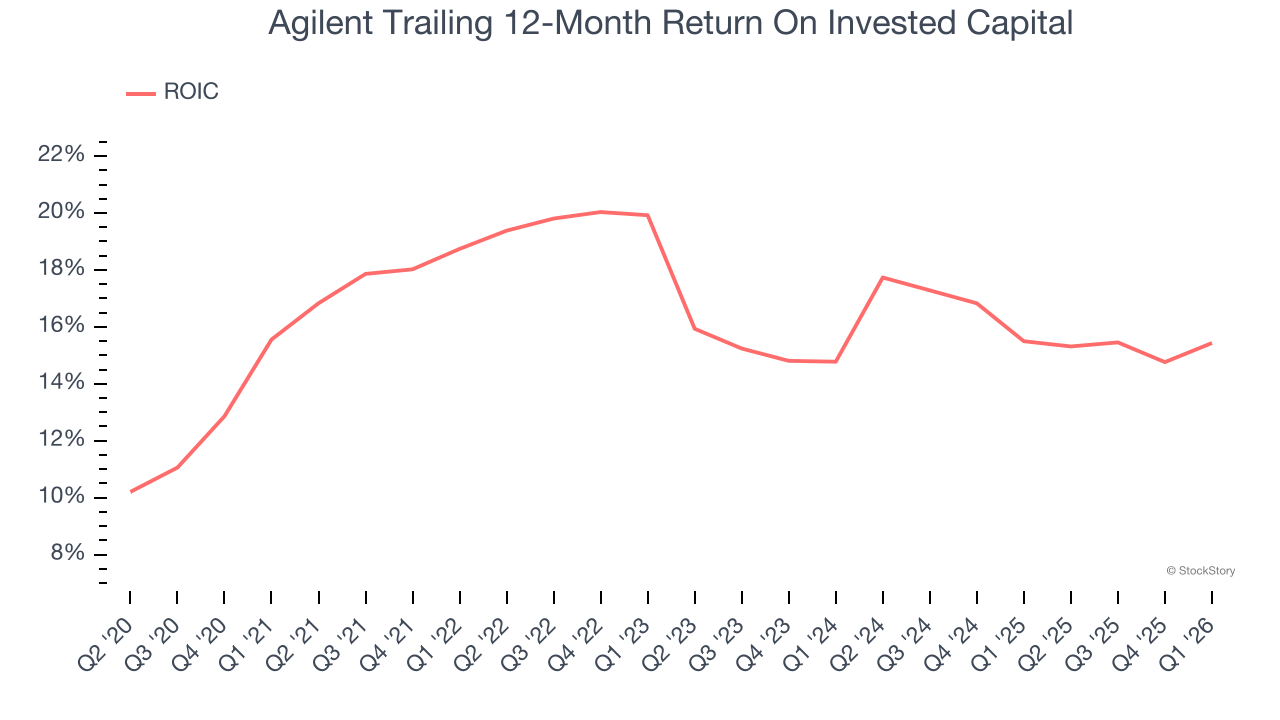

3. New Investments Fail to Bear Fruit as ROIC Declines

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

On average, Agilent’s ROIC decreased by 3.9 percentage points annually each year over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Agilent isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 21.1× forward P/E (or $134.31 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re fairly confident there are better investments elsewhere. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Agilent

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.