Things have been getting from bad to worse for Lucid Group (LCID), which was once touted as the “next Tesla.” The stock, which lost 65% last year, has extended its dismal run into 2026 and plunged below the $10 price level yesterday, Jan. 20. Absolute price levels can be confusing at times, though, as Ford (F) shares are also not far from the $10 price level despite the company being listed for seven decades.

However, if not for the 1-for-10 reverse stock split that Lucid completed last year, the stock price would be below $1 now, making it a delisting candidate. Let's examine Lucid Motors’ outlook and analyze whether it's too late to sell the once-promising startup electric vehicle (EV) company.

Why Is Lucid Motors Stock Falling?

The fall in Lucid Motors' stock is not a 2025 or 2026 thing, and it has the dubious distinction of falling every year since going public in 2021. What has changed is the reasoning behind the crash. This time around, we have a broad-based selloff in markets amid U.S. President Donald Trump’s threats to take over Greenland.

However, beyond the broader market weakness, Lucid Motors’ interim CEO Marc Winterhoff’s remarks about seeking funding beyond Saudi Arabia’s Public Investment Fund (PIF) added fuel to the selloff. While the company has claimed that his comments were “taken out of context or misinterpreted” and that it expects continued backing from the cash-rich fund, which has poured billions of dollars into the company since announcing a $1 billion investment in 2018, the damage was done.

Notably, PIF has been nothing short of a lifesaver for Lucid, which is burning cash at an alarming rate even by the startup EV industry standards. Apart from investing directly into the cash-guzzling EV startup by participating in every stock sale since the 2021 listing. It has also opened a delayed draw term loan credit facility for Lucid and raised its size by $750 million to $2 billion in Q3 2025. Last year, the PIF virtually provided a backstop in Lucid’s convertible bond sale by entering into a privately negotiated prepaid forward transaction.

PIF Should Continue to Back Lucid Motors

The Saudi-PIF partnership is a win-win. Lucid built The Kingdom’s first car manufacturing facility and is now building the second one, which, unlike the first one, would actually build cars instead of only assembling them.

Saudi Arabia sees EVs as a key part of its strategic goals and a hedge against the expected fall in oil demand amid the EV transition. Partnering with Lucid, which, despite its massive losses, has one of the best products in the market, makes sense for the oil-rich nation. Separately, Saudi Arabia has also partnered with Foxconn (FITGF)—best known for making Apple (AAPL) iPhones—to launch its first domestic EV car brand named Ceer.

Meanwhile, contrary to fears among some, I don’t believe that PIF would give up on Lucid, at least for now. Cantor Fitzgerald also has the same opinion after its recent meeting with PIF management.

LCID Stock Forecast

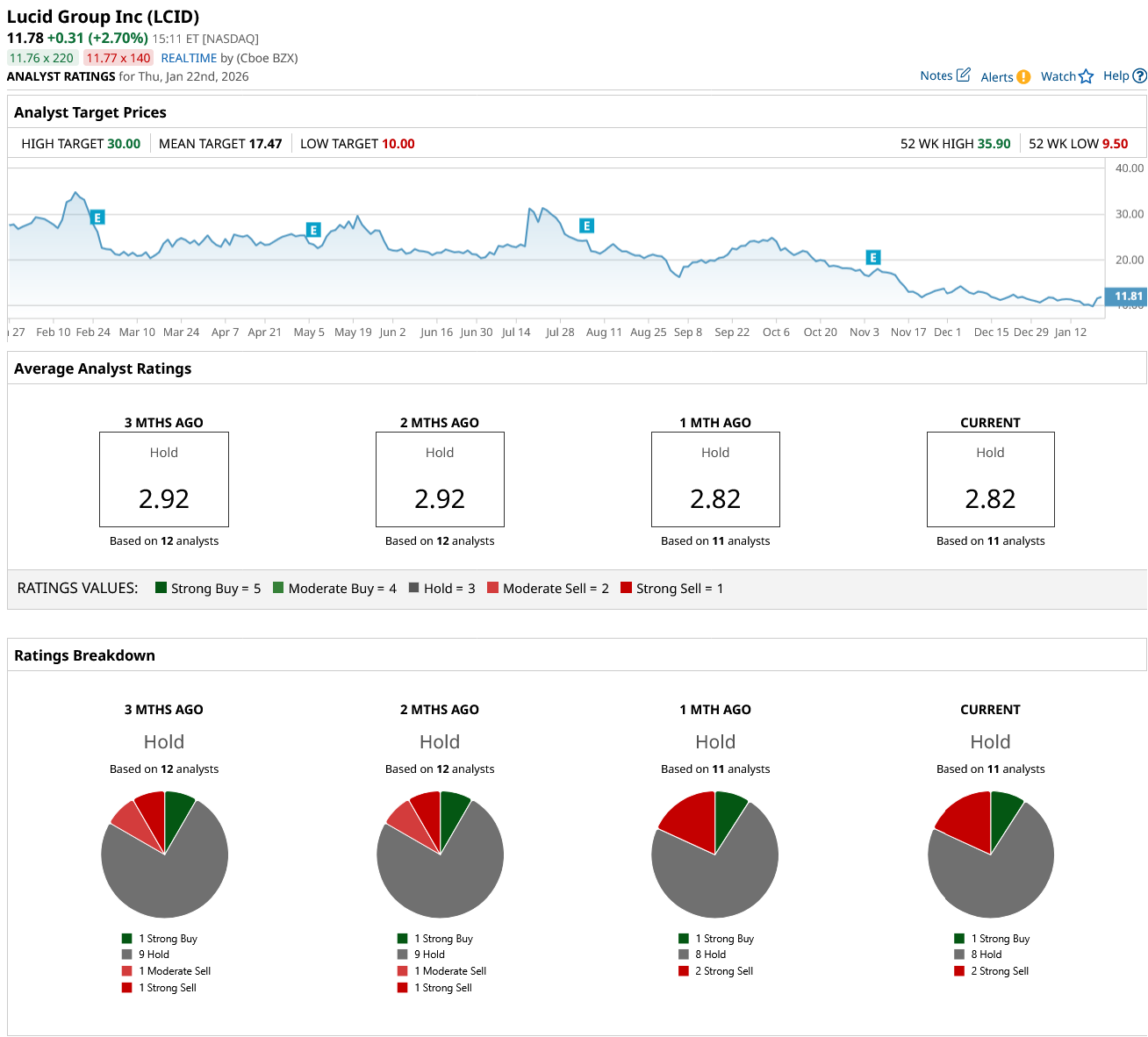

The sell-side analyst community is overall quite bearish on LCID stock, and it only has one “Strong Buy” rating from the 11 analysts polled by Barchart. Eight analysts rate the stock as a “Hold” or some equivalent, and the remaining two as a “Strong Sell.”

Meanwhile, amid the recent crash, Lucid trades just above its Street-low target price of $10, while the mean target price of $17.47 is nearly 50% higher. The Street-high target price of $30 implies the stock almost tripling from these levels.

Is It Too Late to Sell LCID Stock?

Lucid had almost everything a startup EV company would have wanted—a quality product that has consistently received rave reviews from analysts and backing from a fund with real deep pockets whose strategic interests converge with the company.

However, despite the head start, Lucid Motors’ sales have failed to take off materially. While the tepid sales of the Air sedan could be partially blamed on apathy towards sedans in general, even the sales of the Gravity SUV haven’t really been all that impressive.

Lucid is next working on a midsize platform, which would be priced below $50,000. However, the competition in that space might only intensify with several companies looking to launch affordable models. This includes the R2 platform from Rivian (RIVN) and the sub-$30,000 vehicle that Ford has promised.

To sum it up, the operating environment is not expected to improve for Lucid Motors anytime soon, especially as demand for EVs in the U.S. appears weak. Exports from the upcoming Saudi factory could be one driver for the company, but it would need to compete with Chinese companies in the global markets—something even Tesla (TSLA) is struggling with.

Lucid Motors’ market cap has now plunged to just about $3 billion, which, despite all the company’s troubles, is not expensive. Markets appear to have given up on Lucid, as reflected in these depressed valuations. I expect some upward traction in Lucid shares this year, with the Q4 2025 earnings in February and the Investor Day in March being two key near-term triggers. I would also be watching out for new partnerships of the kind Lucid Motors previously announced with Aston Martin and Uber (UBER).

Overall, I would argue that while Lucid Motors faces some serious headwinds, it is a bit too late to exit the stock and would continue to stay put in the company for now.

On the date of publication, Mohit Oberoi had a position in: LCID , RIVN , F , TSLA , AAPL . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart