After two weak years, real estate investment trusts (REITs) are making a comeback in 2026. Farmland REITs were up about 24% year-to-date (YTD) as of mid-February, while data-center REITs gained 22%, net lease REITs rose 15%, and self-storage REITs added roughly 14%. Lower rates are starting to make the sector more attractive again, especially for income investors. Because REITs must pay out at least 90% of their taxable income as dividends, they remain one of the market’s go-to income plays.

Some have already started rewarding shareholders, including National Retail Properties (NNN), which recently announced its 36th-straight annual dividend increase. EPR Properties (EPR) also recently raised its payout by 5%, marking its fifth-straight year of increases.

Now, Simon Property Group (SPG) — the largest retail REIT in the U.S. — is joining that list. On May 11, Simon Property Group reported first-quarter 2026 results that came in ahead of its own plan. It also announced a Q2 dividend of $2.25 per share, up by $0.15 or 7.1% from a year ago. SPG stock has surged 22% over the past 52 weeks, relatively in line with the S&P 500's ($SPX) gain of 24% and beating the Real Estate Select Sector SPDR Fund's (XLRE) gain of 4% in the same period.

With Simon Property Group recently raising its dividend, increasing full-year guidance, and holding $8.7 billion in liquidity, is this the beginning of an even longer run of increases? Let’s take a closer look.

The Numbers Behind Simon Property Group's Dividend Increase

Simon Property Group owns some of the top malls, outlet centers, and mixed-use properties in the U.S. and abroad, making money mainly by leasing space to retailers. SPG stock has also been doing well, up more than 22% in the past 12 months and more than 8% so far this year.

Even after that run, Simon Property Group still looks reasonably priced. It trades at a forward price-to-earnings (P/E) ratio of 15.1 times, well below the real estate sector average of 30 times.

The dividend is a big part of the story. Simon Property Group just declared a quarterly dividend of $2.25 per share for Q2 2026. That's a hike of $0.15 or a year-over-year (YOY) increase of 7.1%. SPG stock has a 4.4% forward annual yield, and with a forward payout ratio of 60.87%, the dividend still looks well covered. The dividend raise also marked the company’s fifth-straight year of increases.

That payout growth is being supported by solid operating results. In Q1, net income attributable to common stockholders rose to $479.6 million, or $1.48 per diluted share. That was up from $413.7 million, or $1.27 per diluted share, in the prior-year period. Real estate funds from operations (FFO), a key REIT profit measure, increased 7.5% YOY to $1.208 billion, or $3.17 per diluted share. FFO rose 9% YOY to $1.108 billion, or $2.91 per diluted share.

Domestic property net operating income (NOI) and portfolio NOI both grew 6.7%. Occupancy stayed strong at 96%, while base minimum rent per square foot increased 5.2% to $61.99, and retailer sales per square foot jumped 11.8% to $819 for the trailing 12 months ended March 31.

What Continues to Drive Growth?

Simon Property Group recently extended its $5 billion multi-currency unsecured revolving credit facility, pushing the maturity date out to June 2030 with an option to extend another year to 2031. The new deal also lowered the interest rate by 15 basis points to SOFR plus 65 basis points, thanks to support from 28 banks. That cuts borrowing costs and gives the company more financial room to work with. Simon Property Group also updated its existing $3.5 billion revolving credit facility to match the same pricing.

On the property side, Simon Property Group is putting money back into its assets. In February, the company announced a major redevelopment at Copley Place in Boston, Massachusetts, turning the old Neiman Marcus space into a multi-level luxury retail and dining area. The project will bring in Casa Tua Cucina and Estiatorio Milos, along with more luxury boutiques to be named later. That adds to recent openings like Dolce & Gabbana, expanded FENDI and Tourneau spaces, and a new LOEWE store.

Simon Property Group is also spending more than $250 million to upgrade three properties it bought in November 2025: The Mall at Green Hills in Nashville, Tennessee, Cherry Creek Shopping Center in Denver, Colorado, and International Plaza in Tampa, Florida. The Mall at Green Hills will get a full exterior makeover with two-story flagship entrances and new luxury boutiques. Cherry Creek will see modernized flagship spaces and updated architecture. Finally, International Plaza is getting a 50,000-square-foot open-air expansion as well as upgraded dining areas and a refreshed interior.

At the same time, Simon Property Group's board has approved a new $2 billion stock buyback program running through February 2028, replacing the old one and showing confidence in the company's ability to generate cash and return capital to shareholders.

What Does Wall Street Expect Next for Simon Property Group?

For the June 2026 quarter, analysts expect Simon Property Group to earn $3.15 per share, up more than 3% YOY from $3.05 a year earlier. Looking a little further out, Wall Street sees EPS of $3.30 for the September 2026 quarter, compared with $3.22 last year. That would mean another roughly 2% increase. For full-year 2026, the estimate is $13.20 per share, up from $12.73, or roughly 4% YOY growth.

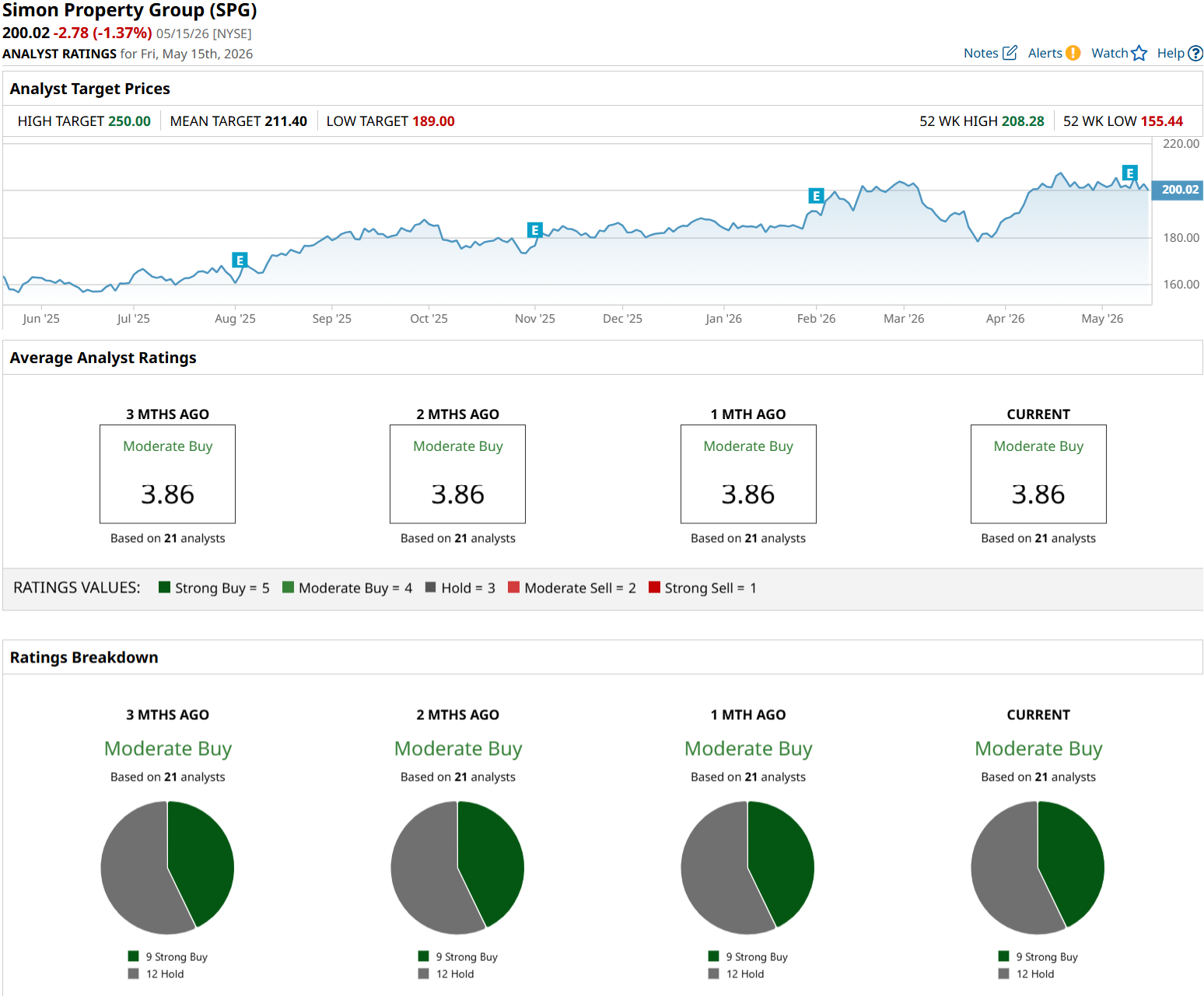

These expectations are also showing up in recent analyst calls. On May 14, Citigroup analyst Nick Joseph kept a “Hold” rating on SPG stock but raised his price target to $205 from $189 after the strong Q1 results. Before that, on May 12, Evercore ISI analyst Steve Sakwa also stuck with a “Hold” rating and lifted his target to $207 from $198 shortly after earnings.

Out of 21 analysts with coverage, SPG stock has a consensus “Moderate Buy" rating. The average price target is $211.40, which suggests about 5% potential upside from current price levels.

Conclusion

Overall, Simon Property Group looks like a high-yield REIT whose latest dividend hike is being backed by real operating strength rather than financial engineering. Rising FFO, healthy occupancy, solid rent growth, and active reinvestment across the portfolio all support the payout. Given the company’s stronger guidance, redevelopment pipeline, lower borrowing costs, and generally constructive analyst outlook, the most likely near-term path for shares appears to be modest upside rather than a breakout surge, especially after SPG stock’s recent run.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart