As the Q2 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the custody bank industry, including Ameriprise Financial (NYSE: AMP) and its peers.

Custody banks safeguard financial assets and provide services like settlement, accounting, and regulatory compliance for institutional investors. Growth opportunities stem from increasing global assets under custody, demand for data analytics, and blockchain technology adoption for settlement efficiency. Challenges include fee pressure from large clients, substantial technology investment requirements, and competition from both traditional players and fintech firms entering the space.

The 13 custody bank stocks we track reported a mixed Q2. As a group, revenues were in line with analysts’ consensus estimates.

Thankfully, share prices of the companies have been resilient as they are up 5.2% on average since the latest earnings results.

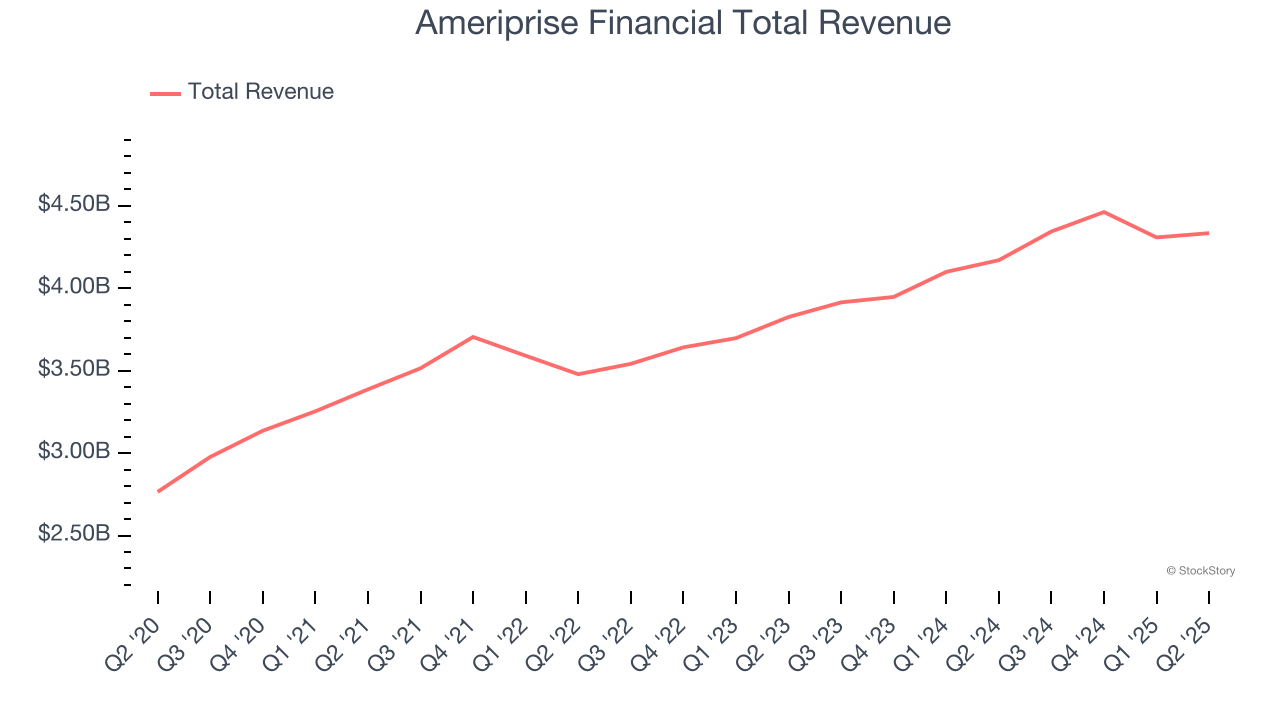

Ameriprise Financial (NYSE: AMP)

Founded in 1894 and spun off from American Express in 2005, Ameriprise Financial (NYSE: AMP) provides financial planning, wealth management, asset management, and insurance products to help individuals and institutions achieve their financial goals.

Ameriprise Financial reported revenues of $4.34 billion, up 3.9% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with a narrow beat of analysts’ EPS estimates.

Unsurprisingly, the stock is down 3.7% since reporting and currently trades at $516.63.

Is now the time to buy Ameriprise Financial? Access our full analysis of the earnings results here, it’s free.

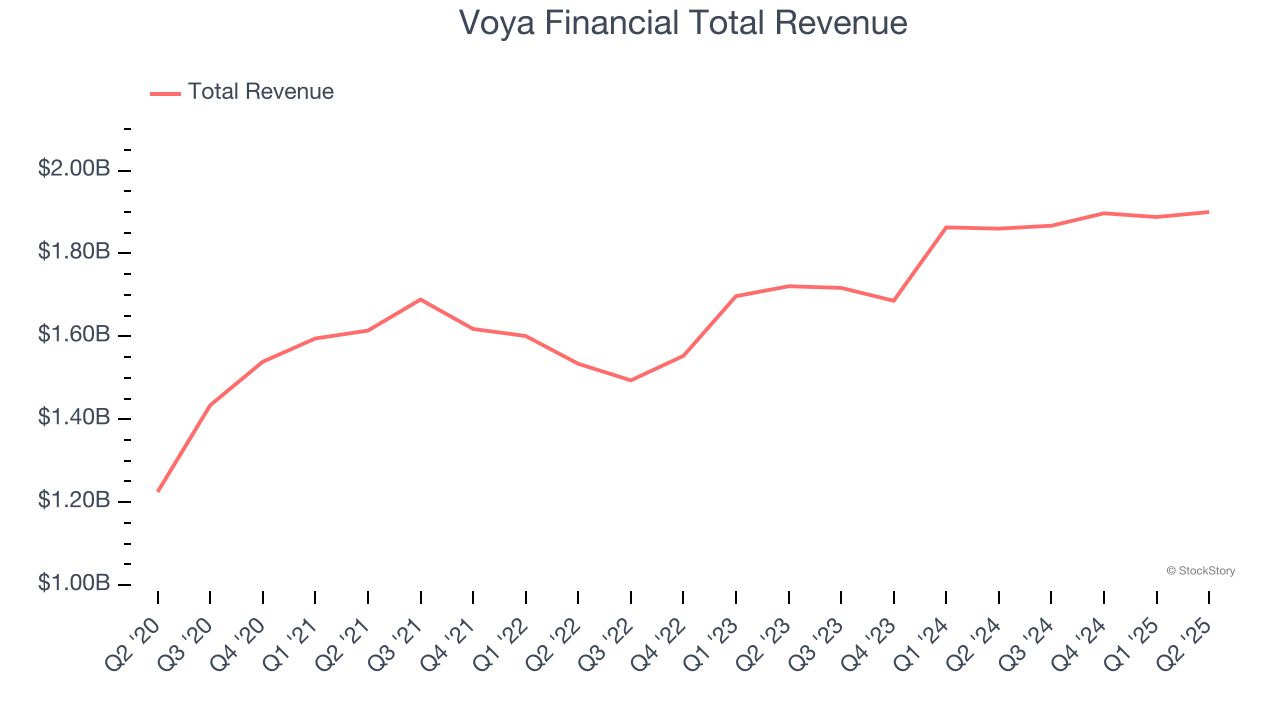

Best Q2: Voya Financial (NYSE: VOYA)

Originally spun off from Dutch financial giant ING in 2013 and rebranded with a name suggesting "voyage," Voya Financial (NYSE: VOYA) provides workplace benefits and savings solutions to U.S. employers, helping their employees achieve better financial outcomes through retirement plans and insurance products.

Voya Financial reported revenues of $1.9 billion, up 2.2% year on year, outperforming analysts’ expectations by 13.5%. The business had a stunning quarter with a beat of analysts’ EPS estimates.

Voya Financial scored the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 10.6% since reporting. It currently trades at $75.03.

Is now the time to buy Voya Financial? Access our full analysis of the earnings results here, it’s free.

Slowest Q2: Franklin Resources (NYSE: BEN)

Operating under the widely recognized Franklin Templeton brand since 1947, Franklin Resources (NYSE: BEN) is a global investment management organization that offers financial services and solutions to individuals, institutions, and wealth advisors worldwide.

Franklin Resources reported revenues of $1.59 billion, down 3.7% year on year, falling short of analysts’ expectations by 18.8%. It was a softer quarter as it posted a significant miss of analysts’ EPS estimates.

Franklin Resources delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 6.5% since the results and currently trades at $25.54.

Read our full analysis of Franklin Resources’s results here.

Northern Trust (NASDAQ: NTRS)

Founded in 1889 during Chicago's post-Great Fire rebuilding boom, Northern Trust (NASDAQ: NTRS) provides wealth management, asset servicing, and banking solutions to corporations, institutions, families, and high-net-worth individuals globally.

Northern Trust reported revenues of $2.00 billion, down 26.4% year on year. This result surpassed analysts’ expectations by 1.9%. Overall, it was a strong quarter as it also produced a beat of analysts’ EPS estimates.

Northern Trust had the slowest revenue growth among its peers. The stock is up 2.8% since reporting and currently trades at $130.06.

Read our full, actionable report on Northern Trust here, it’s free.

SEI Investments (NASDAQ: SEIC)

Founded in 1968 as Simulated Environments Inc. to train bank loan officers using computer simulations, SEI Investments (NASDAQ: SEIC) provides technology platforms, investment management, and operational solutions for financial institutions, wealth managers, and investors.

SEI Investments reported revenues of $559.6 million, up 7.8% year on year. This number came in 0.7% below analysts' expectations. More broadly, it was actually a very strong quarter as it put up a beat of analysts’ EPS estimates.

The stock is down 1.3% since reporting and currently trades at $88.85.

Read our full, actionable report on SEI Investments here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.