GameStop trades at $27.14 per share and has stayed right on track with the overall market, gaining 21.6% over the last six months. At the same time, the S&P 500 has returned 18.6%.

Is there a buying opportunity in GameStop, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think GameStop Will Underperform?

We're swiping left on GameStop for now. Here are three reasons why GME doesn't excite us and a stock we'd rather own.

Note that our analysis is rooted in fundamentals, not meme-stock technicals.

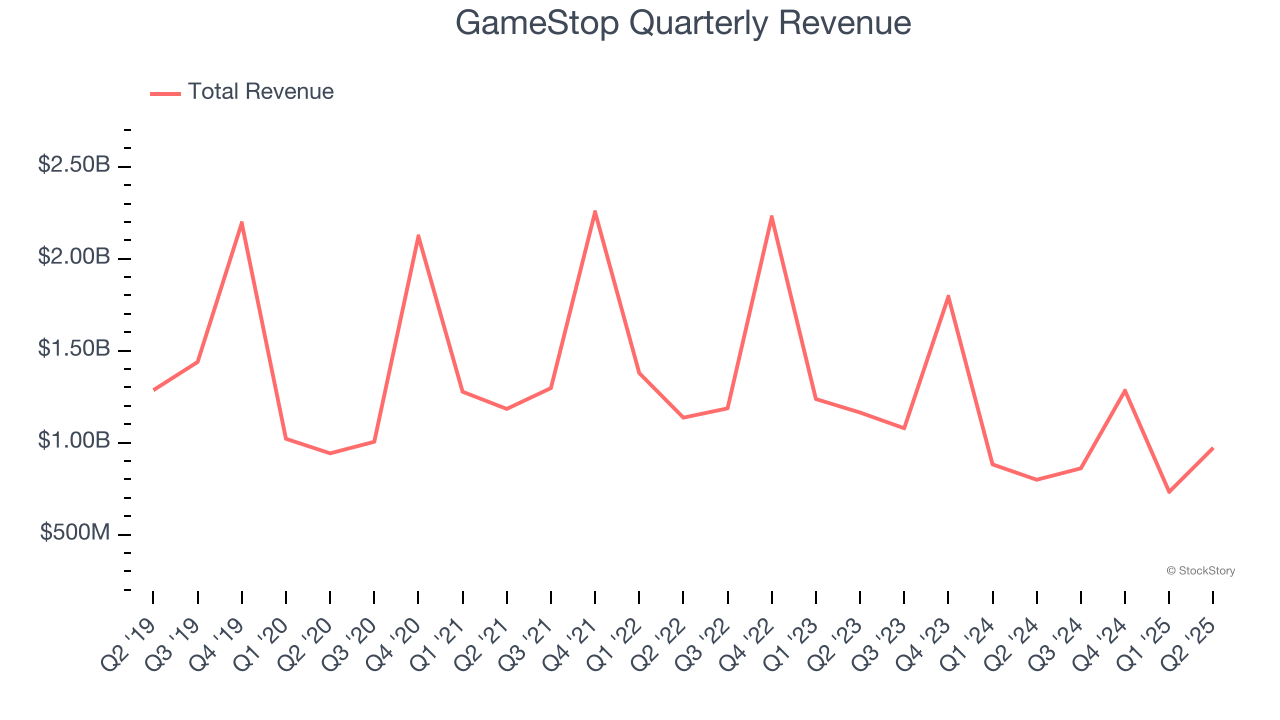

1. Revenue Spiraling Downwards

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. GameStop’s demand was weak over the last six years as its sales fell at a 11.2% annual rate. This was below our standards and signals it’s a low quality business.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect GameStop’s revenue to drop by 13.4%, a decrease from This projection is underwhelming and indicates its products will face some demand challenges.

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

GameStop’s five-year average ROIC was negative 12.6%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer retail sector.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of GameStop, we’ll be cheering from the sidelines. That said, the stock currently trades at 49.5× forward P/E (or $27.14 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.