Frontier’s 13.4% return over the past six months has outpaced the S&P 500 by 5.2%, and its stock price has climbed to $5.13 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Frontier, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Frontier Will Underperform?

Despite the momentum, we're sitting this one out for now. Here are three reasons you should be careful with ULCC and a stock we'd rather own.

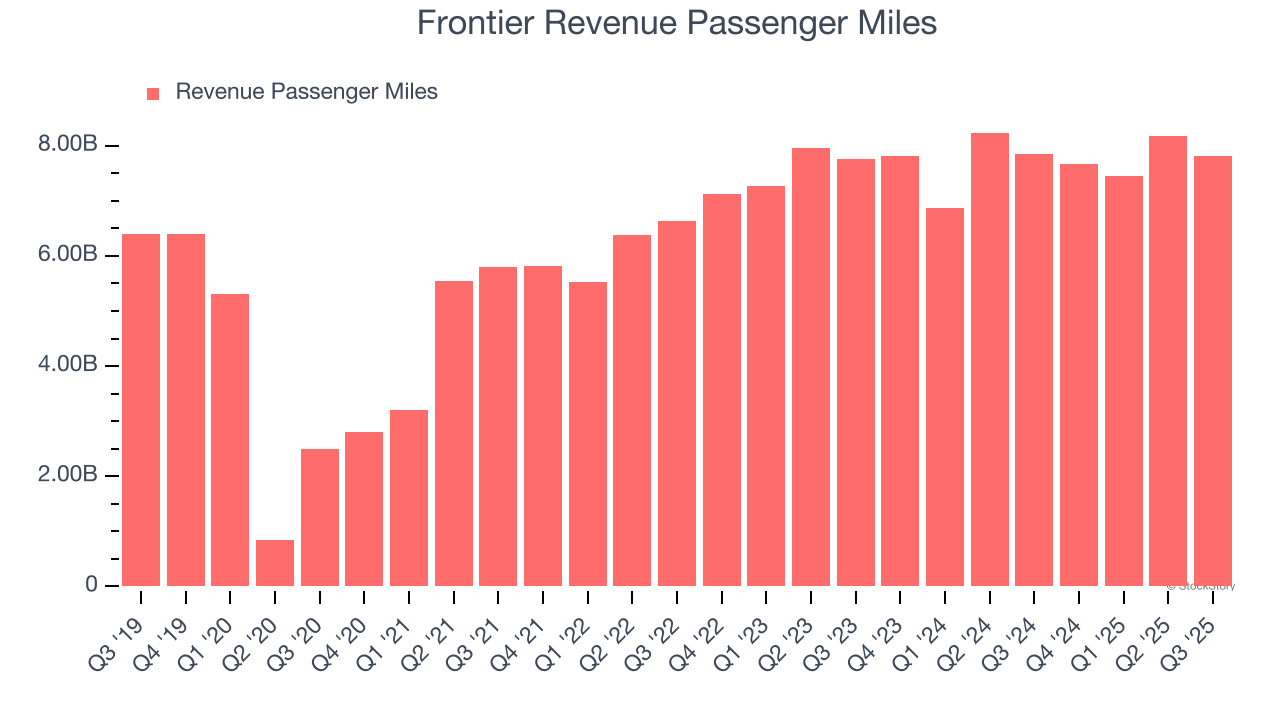

1. Weak Growth in Revenue passenger miles Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Frontier, our preferred volume metric is revenue passenger miles). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Frontier’s revenue passenger miles came in at 7.82 billion in the latest quarter, and over the last two years, averaged 1.8% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

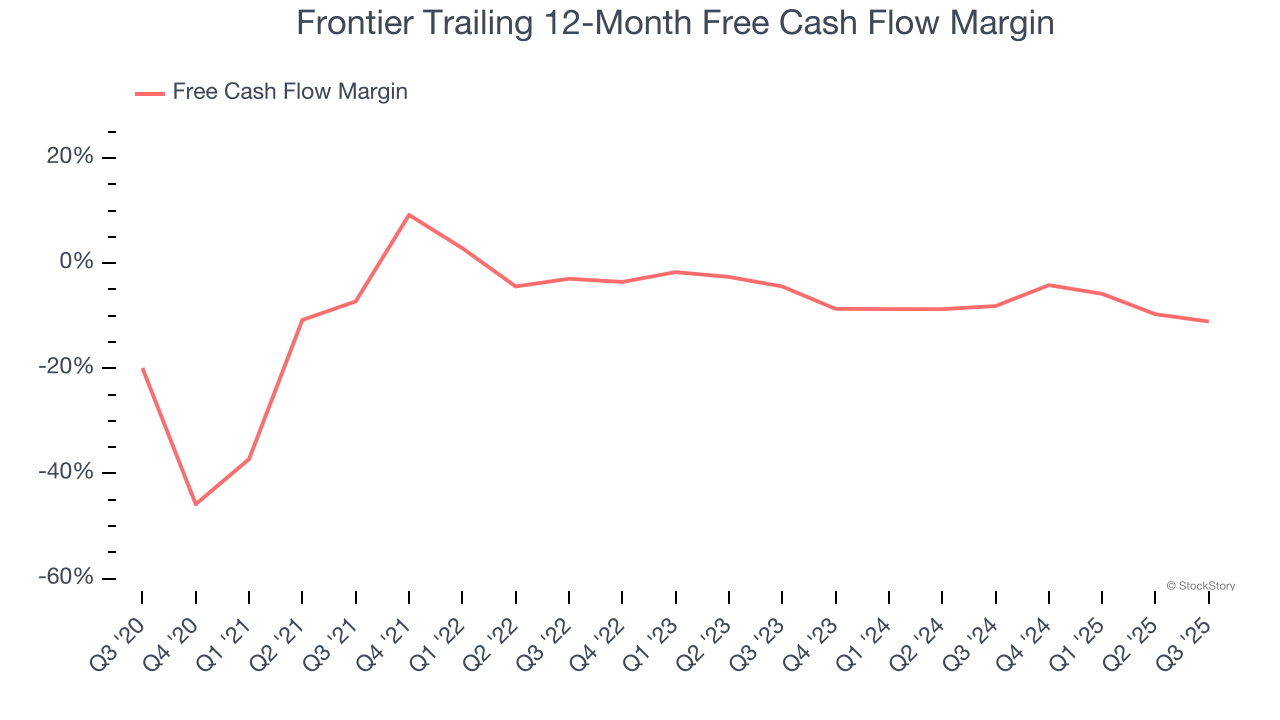

2. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the last two years, Frontier’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 9.6%, meaning it lit $9.64 of cash on fire for every $100 in revenue.

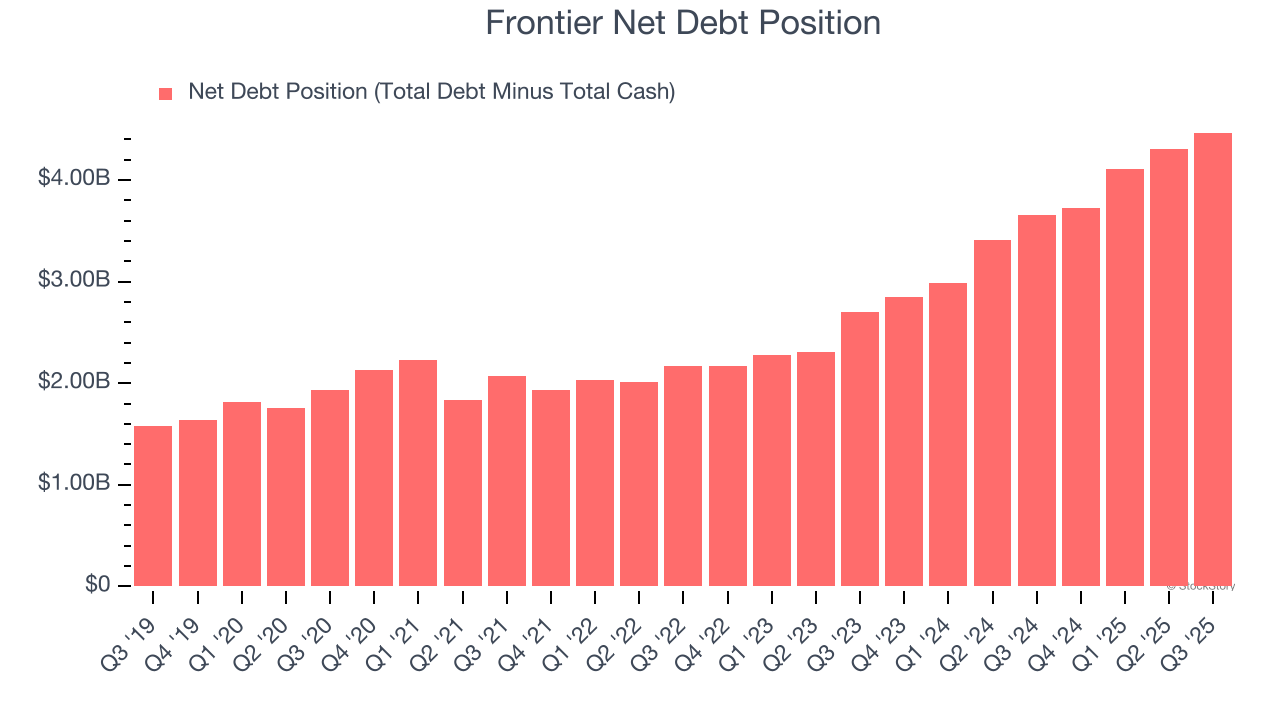

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Frontier burned through $414 million of cash over the last year, and its $5.03 billion of debt exceeds the $566 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Frontier’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Frontier until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Frontier, we’ll be cheering from the sidelines. With its shares beating the market recently, the stock trades at 6.1× forward EV-to-EBITDA (or $5.13 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. Let us point you toward the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Frontier

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.