What a brutal six months it’s been for Itron. The stock has dropped 33.5% and now trades at a new 52-week low of $82.88, rattling many shareholders. This might have investors contemplating their next move.

Is now the time to buy Itron, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Itron Not Exciting?

Despite the more favorable entry price, we're swiping left on Itron for now. Here are three reasons we avoid ITRI and a stock we'd rather own.

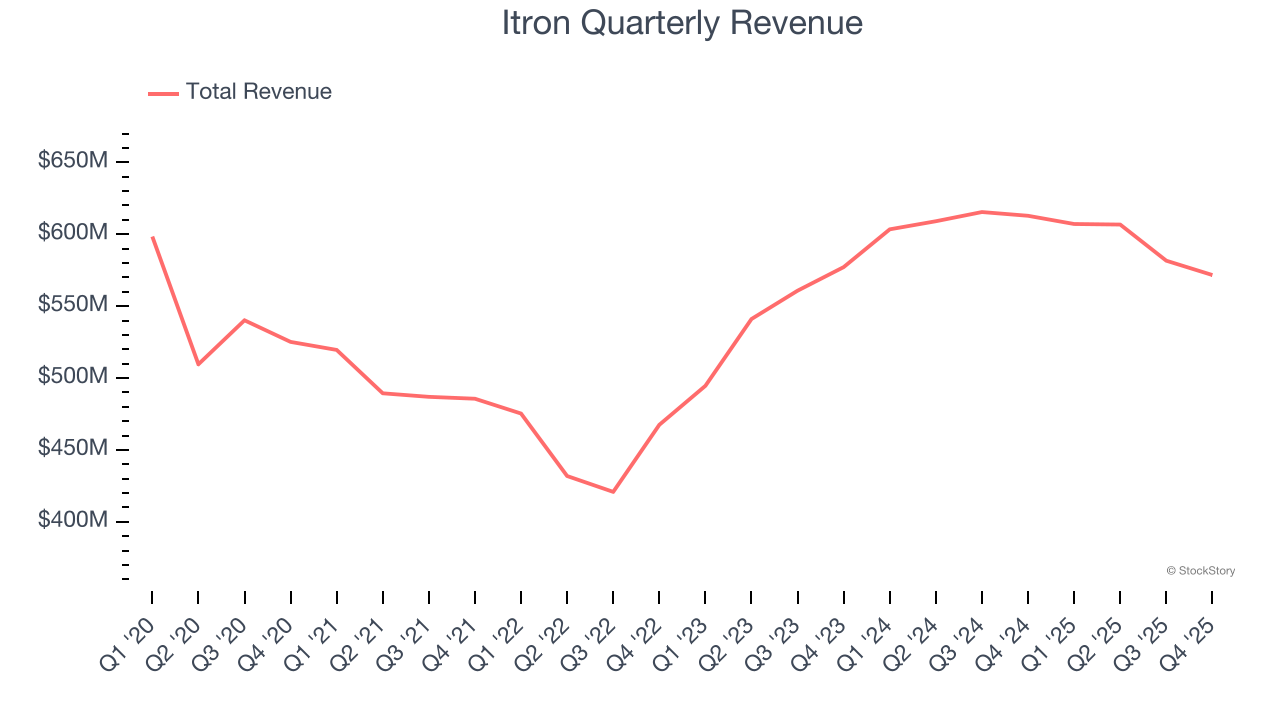

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Itron’s 1.7% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Itron’s revenue to rise by 2.1%, a slight deceleration versus its 1.7% annualized growth for the past five years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

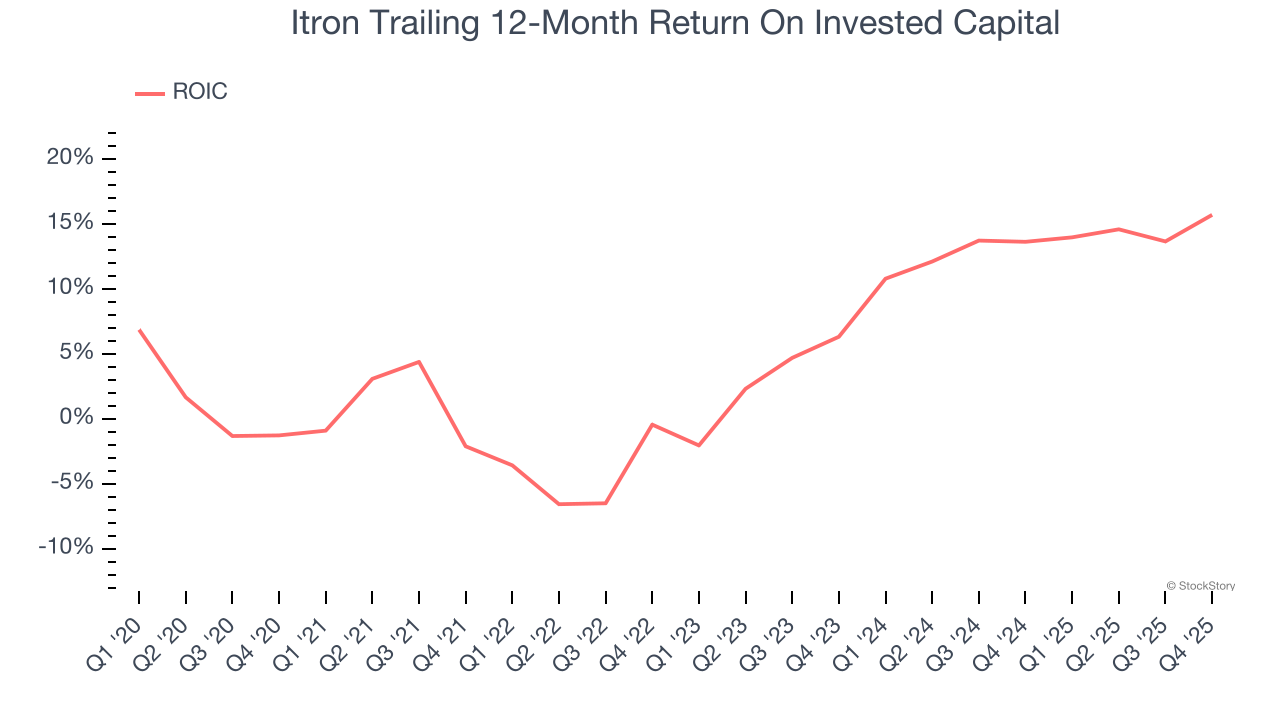

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Itron historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.6%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

Final Judgment

Itron isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 14.2× forward P/E (or $82.88 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at our favorite semiconductor picks and shovels play.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.