WESCO currently trades at $348.18 and has been a dream stock for shareholders. It’s returned 216% since May 2021, nearly tripling the S&P 500’s 77.2% gain. The company has also beaten the index over the past six months as its stock price is up 35.6% thanks to its solid quarterly results.

Is now the time to buy WESCO, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is WESCO Not Exciting?

Despite the momentum, we're cautious about WESCO. Here are three reasons we avoid WCC and a stock we'd rather own.

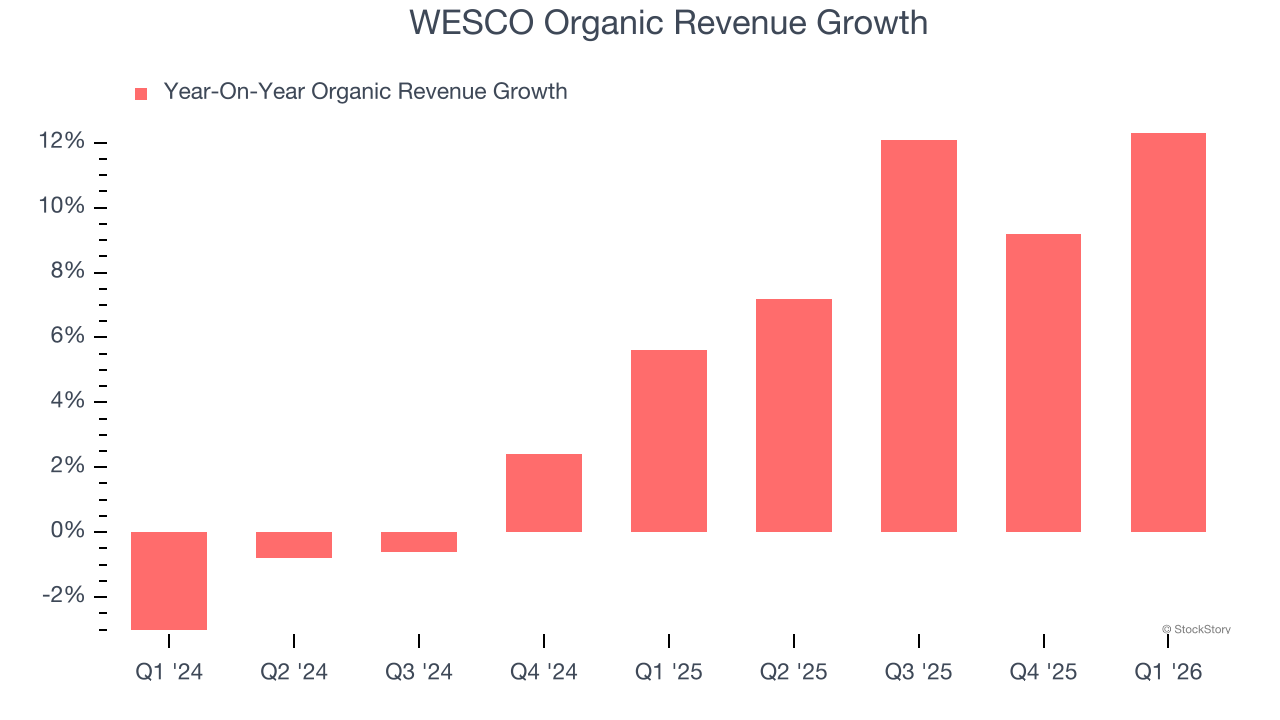

1. Slow Organic Growth Suggests Waning Demand In Core Business

In addition to reported revenue, organic revenue is a useful data point for analyzing Maintenance and Repair Distributors companies. This metric gives visibility into WESCO’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, WESCO’s organic revenue averaged 5.9% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

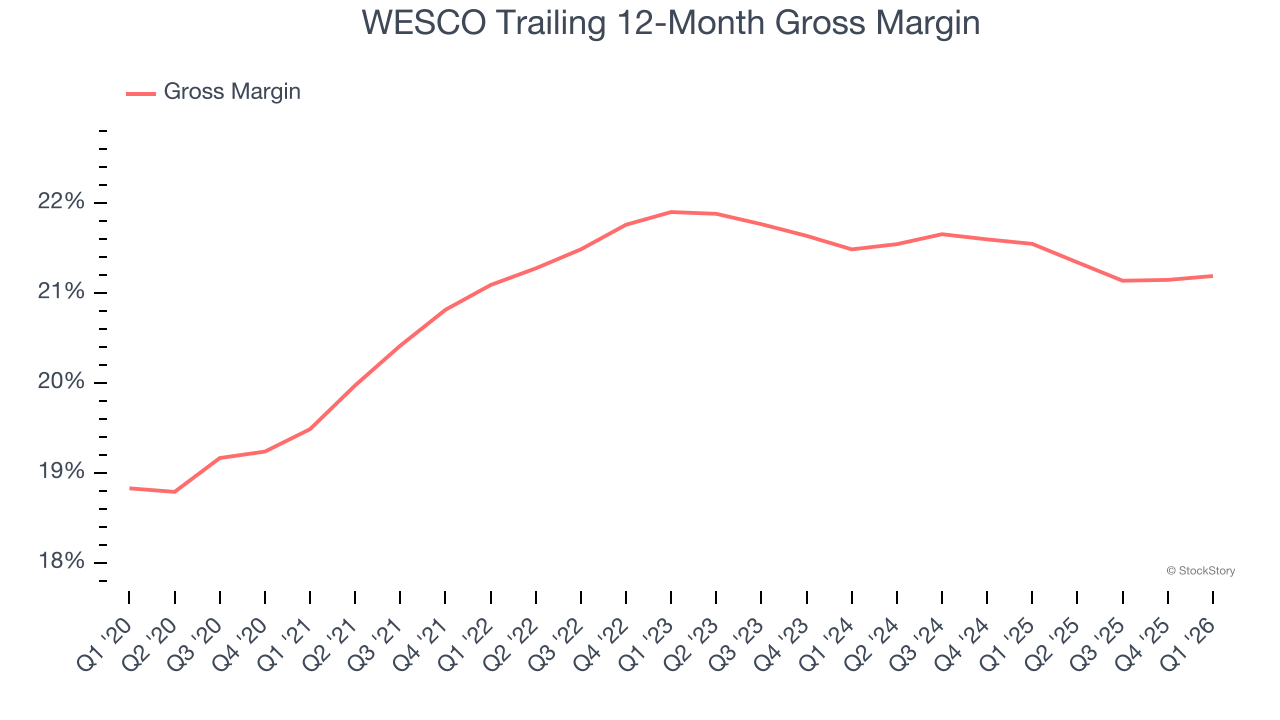

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

WESCO has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 21.4% gross margin over the last five years. Said differently, WESCO had to pay a chunky $78.55 to its suppliers for every $100 in revenue.

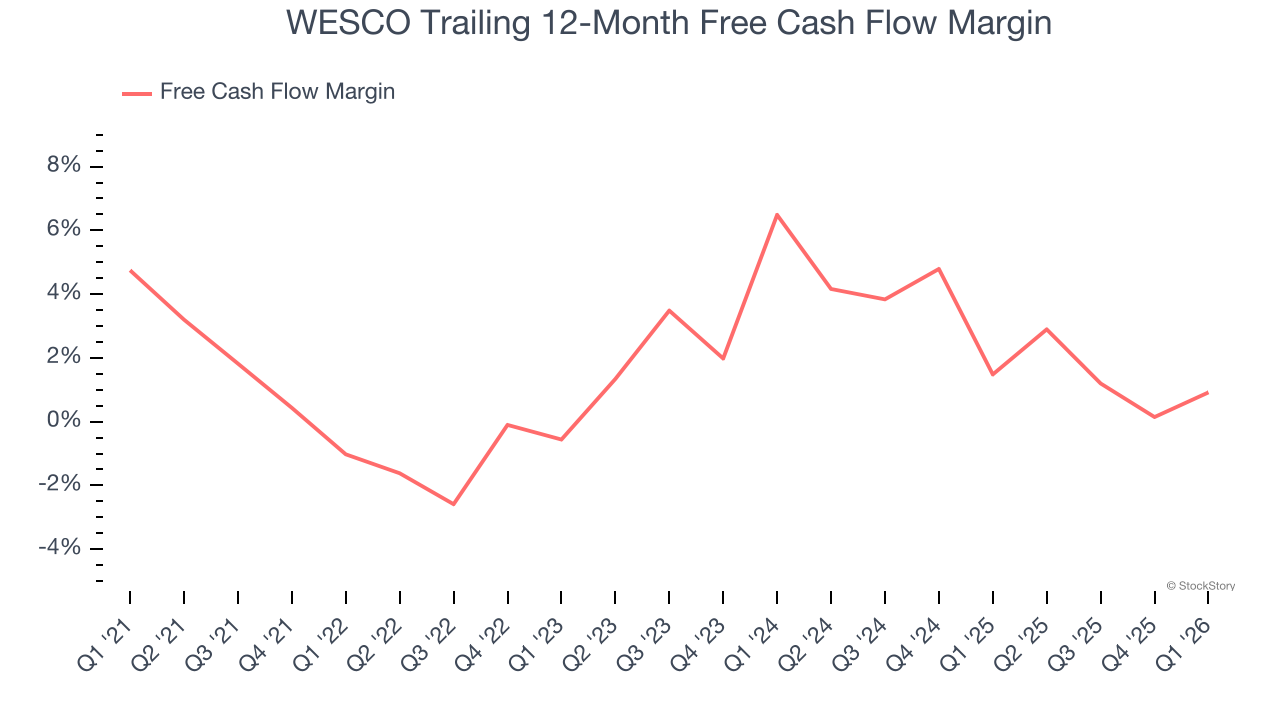

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

WESCO has shown poor cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.5%, below what we’d expect for an industrials business.

Final Judgment

WESCO isn’t a terrible business, but it isn’t one of our picks. With its shares outperforming the market lately, the stock trades at 21.7× forward P/E (or $348.18 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.