Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Opendoor (NASDAQ: OPEN) and the best and worst performers in the consumer discretionary - real estate services industry.

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare. Real estate services companies provide brokerage, property management, appraisal, and advisory services, earning transaction-based commissions and recurring management fees. Tailwinds include long-term housing demand driven by demographic growth, technology platforms that expand market access, and commercial real estate complexity that sustains advisory needs. Headwinds are pronounced: rising interest rates directly suppress transaction volumes by reducing housing affordability and commercial deal activity. Commission-rate compression, driven by discount brokerages and regulatory changes, erodes per-transaction revenue. The industry is highly cyclical, with revenue swings amplified by leverage. PropTech (property technology) disruptors threaten traditional intermediary models.

The 14 consumer discretionary - real estate services stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.3% while next quarter’s revenue guidance was 2.3% above.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.3% since the latest earnings results.

Opendoor (NASDAQ: OPEN)

Founded by real estate guru Eric Wu, Opendoor (NASDAQ: OPEN) offers a technology-driven, convenient, and streamlined process to buy and sell homes.

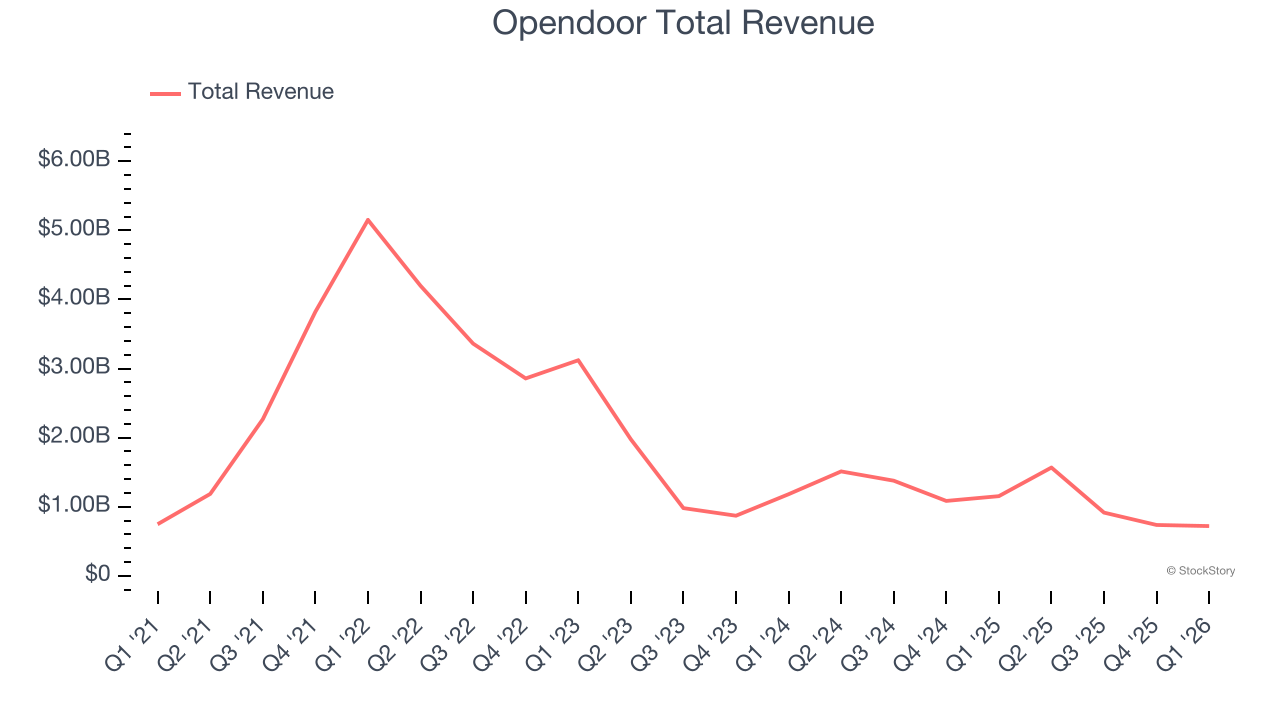

Opendoor reported revenues of $720 million, down 37.6% year on year. This print exceeded analysts’ expectations by 8.3%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ revenue estimates and EPS in line with analysts’ estimates.

“As of April 1st, Opendoor is adjusted EBITDA profitable, on a 12-month go-forward basis. The October cohort was just the start. A full quarter later, we’ve gone from a claim to a track record. Our 4Q25 and January 2026 cash acquisition cohorts have the best combination of margin, margin stability, and resale velocity of any corresponding cohort in company history (excluding the COVID-era cohorts)1. And, each of our October, November, December, and January cohorts are selling faster than any corresponding cohort since COVID. Acquisition contracts are up 2x quarter-over-quarter, back to levels we haven’t seen since 2022. Aged inventory has been cut from half the book to one-tenth while scaling volume. As a result, resale contribution margin is at its highest level in nearly two years,” said Kaz Nejatian, CEO of Opendoor.

The stock is down 19.5% since reporting and currently trades at $4.28.

Is now the time to buy Opendoor? Access our full analysis of the earnings results here, it’s free.

Best Q1: Marcus & Millichap (NYSE: MMI)

Founded in 1971, Marcus & Millichap (NYSE: MMI) specializes in commercial real estate investment sales, financing, research, and advisory services.

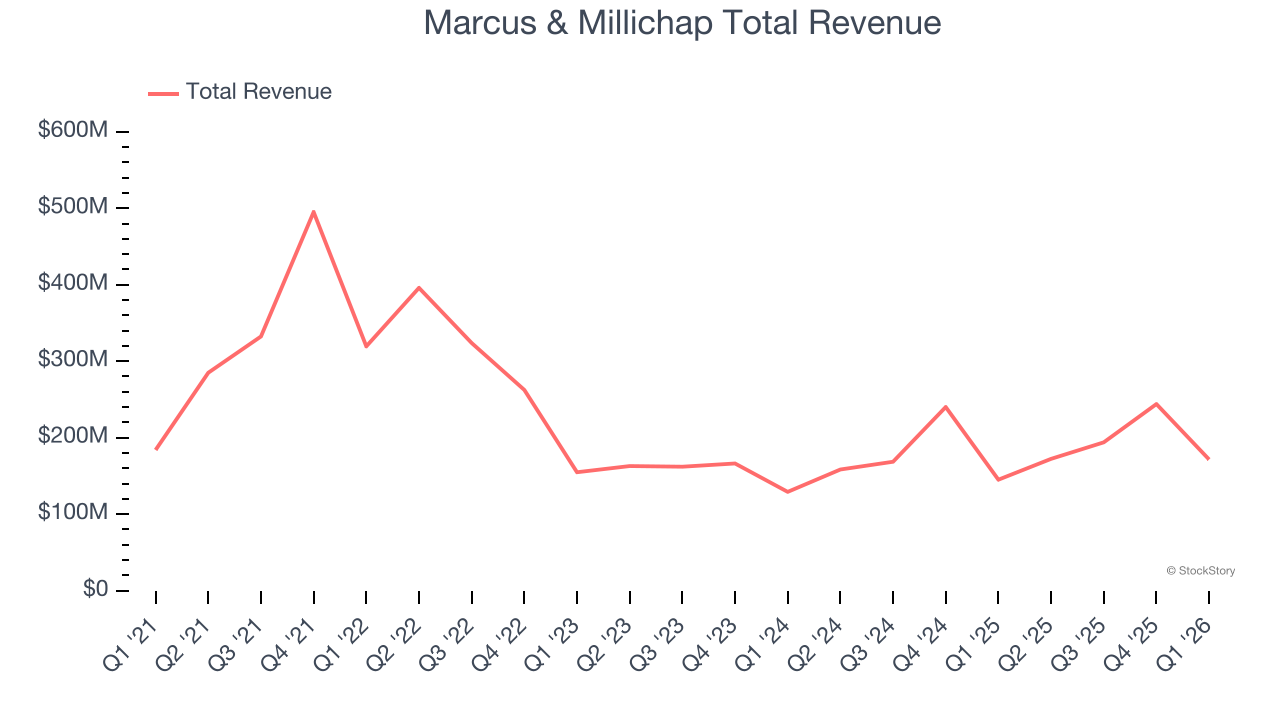

Marcus & Millichap reported revenues of $171.5 million, up 18.2% year on year, outperforming analysts’ expectations by 5.7%. The business had an exceptional quarter with a solid beat of analysts’ EBITDA estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $29.09.

Is now the time to buy Marcus & Millichap? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: RE/MAX (NYSE: RMAX)

Short for Real Estate Maximums, RE/MAX (NYSE: RMAX) operates a real estate franchise network spanning over 100 countries and territories.

RE/MAX reported revenues of $70.23 million, down 5.7% year on year, falling short of analysts’ expectations by 2.7%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income and EPS estimates.

As expected, the stock is down 16.9% since the results and currently trades at $9.20.

Read our full analysis of RE/MAX’s results here.

Newmark (NASDAQ: NMRK)

Founded in 1929, Newmark (NASDAQ: NMRK) provides commercial real estate services, including leasing advisory, global corporate services, investment sales and capital markets, property and facilities management, valuation and advisory, and consulting.

Newmark reported revenues of $846.5 million, up 27.2% year on year. This print surpassed analysts’ expectations by 13.2%. Overall, it was a very strong quarter as it also produced a solid beat of analysts’ revenue estimates and full-year revenue guidance exceeding analysts’ expectations.

Newmark pulled off the biggest analyst estimates beat and highest full-year guidance raise among its peers. The stock is down 9.3% since reporting and currently trades at $14.30.

Read our full, actionable report on Newmark here, it’s free.

Howard Hughes Holdings (NYSE: HHH)

Named after the eccentric business magnate and aviator whose legacy lives on in real estate development, Howard Hughes Holdings (NYSE: HHH) develops, owns, and manages master-planned communities and commercial properties across the United States.

Howard Hughes Holdings reported revenues of $235.9 million, up 18.4% year on year. This result missed analysts’ expectations by 0.5%. Aside from that, it was a very strong quarter as it logged a beat of analysts’ EPS estimates.

The stock is up 1.2% since reporting and currently trades at $64.30.

Read our full, actionable report on Howard Hughes Holdings here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.