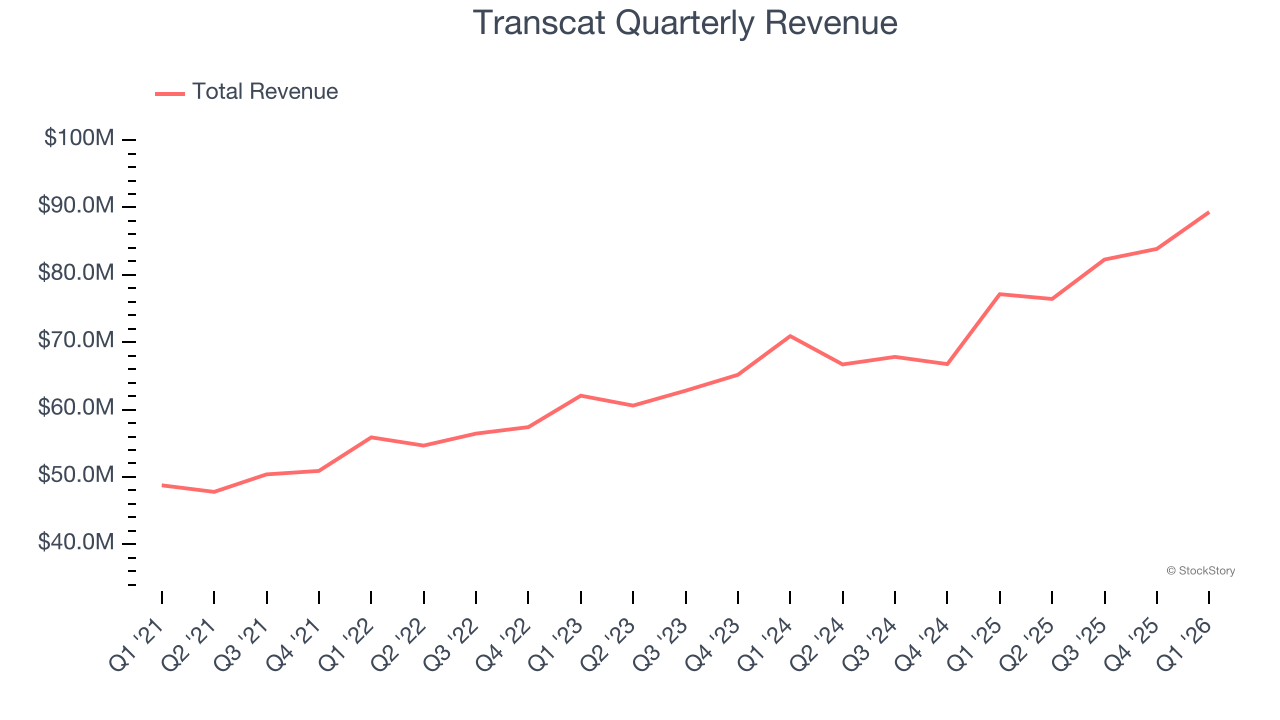

Measurement equipment distributor Transcat (NASDAQ: TRNS) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 15.8% year on year to $89.33 million. Its non-GAAP profit of $0.56 per share was in line with analysts’ consensus estimates.

Is now the time to buy Transcat? Find out by accessing our full research report, it’s free.

Transcat (TRNS) Q1 CY2026 Highlights:

- Revenue: $89.33 million vs analyst estimates of $89.79 million (15.8% year-on-year growth, 0.5% miss)

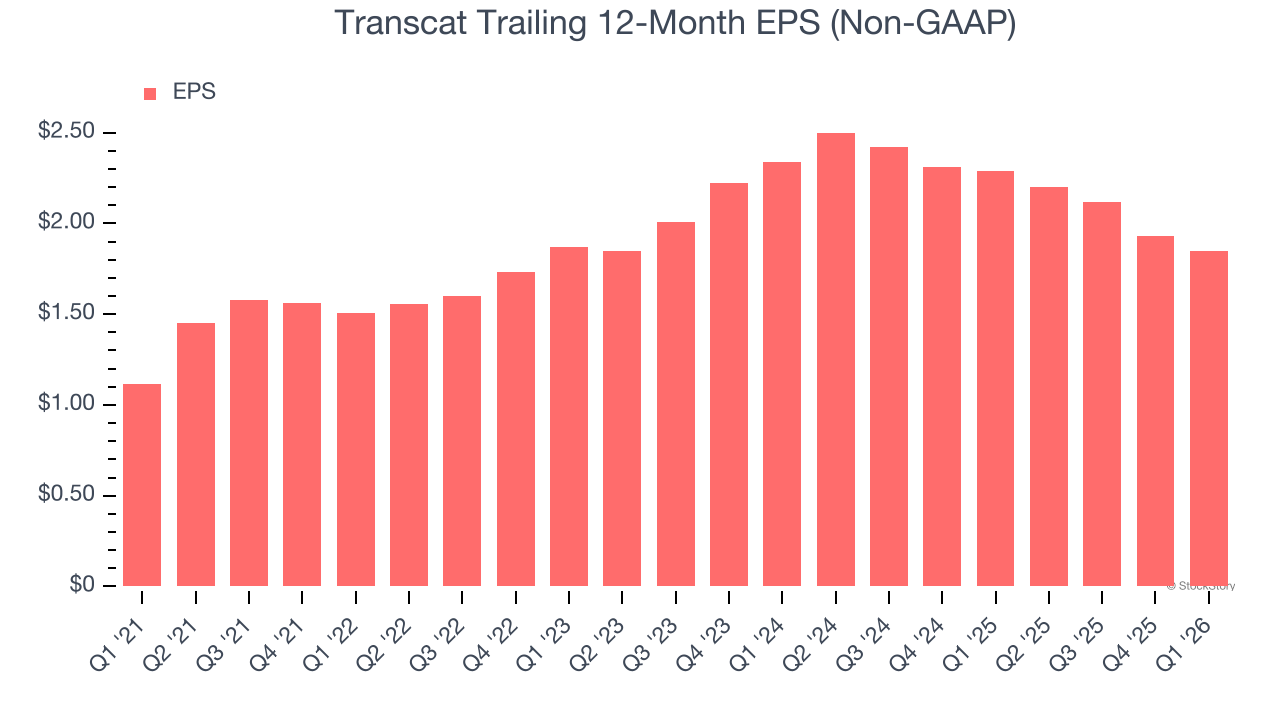

- Adjusted EPS: $0.56 vs analyst estimates of $0.56 (in line)

- Adjusted EBITDA: $14.79 million vs analyst estimates of $13.9 million (16.6% margin, 6.4% beat)

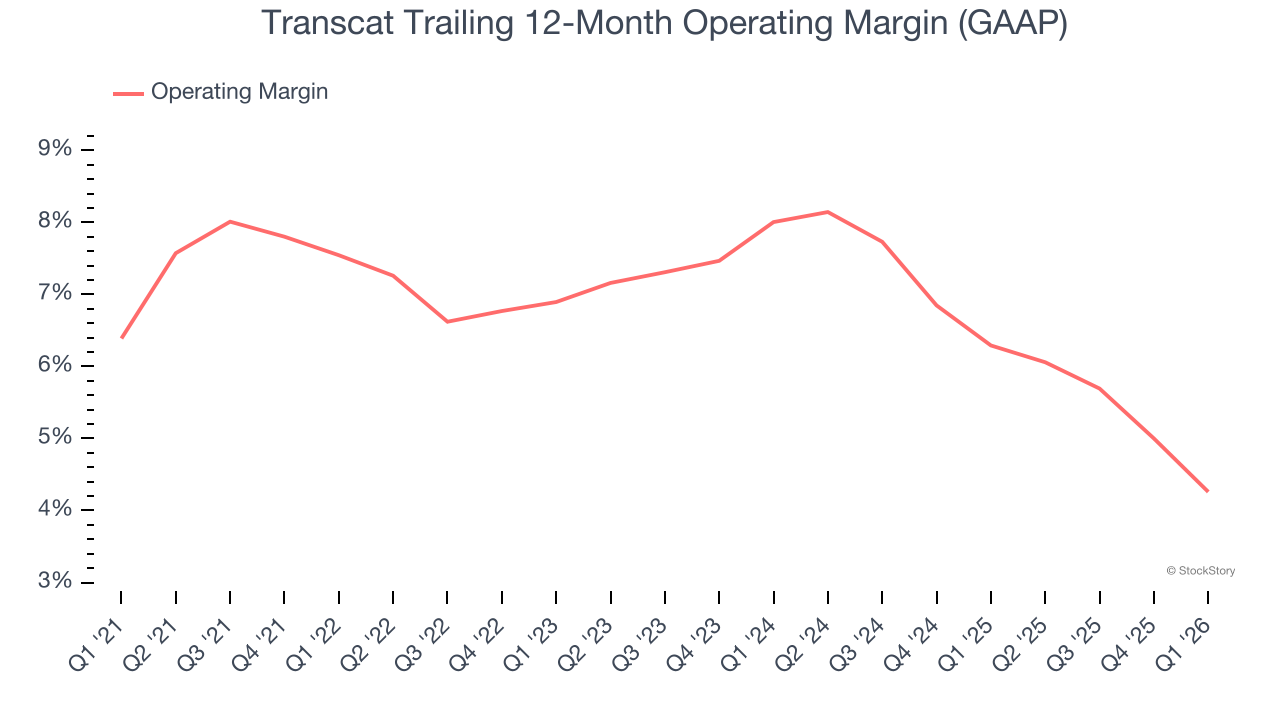

- Operating Margin: 4.8%, down from 8% in the same quarter last year

- Free Cash Flow Margin: 2.9%, down from 10.3% in the same quarter last year

- Market Capitalization: $681.4 million

“Transcat achieved robust results across both business segments in the fiscal fourth quarter, with service organic revenue* climbing 7%," said Jaime Irick, President and CEO.

Company Overview

Serving the pharmaceutical, industrial manufacturing, energy, and chemical process industries, Transcat (NASDAQ: TRNS) provides measurement instruments and supplies.

Revenue Growth

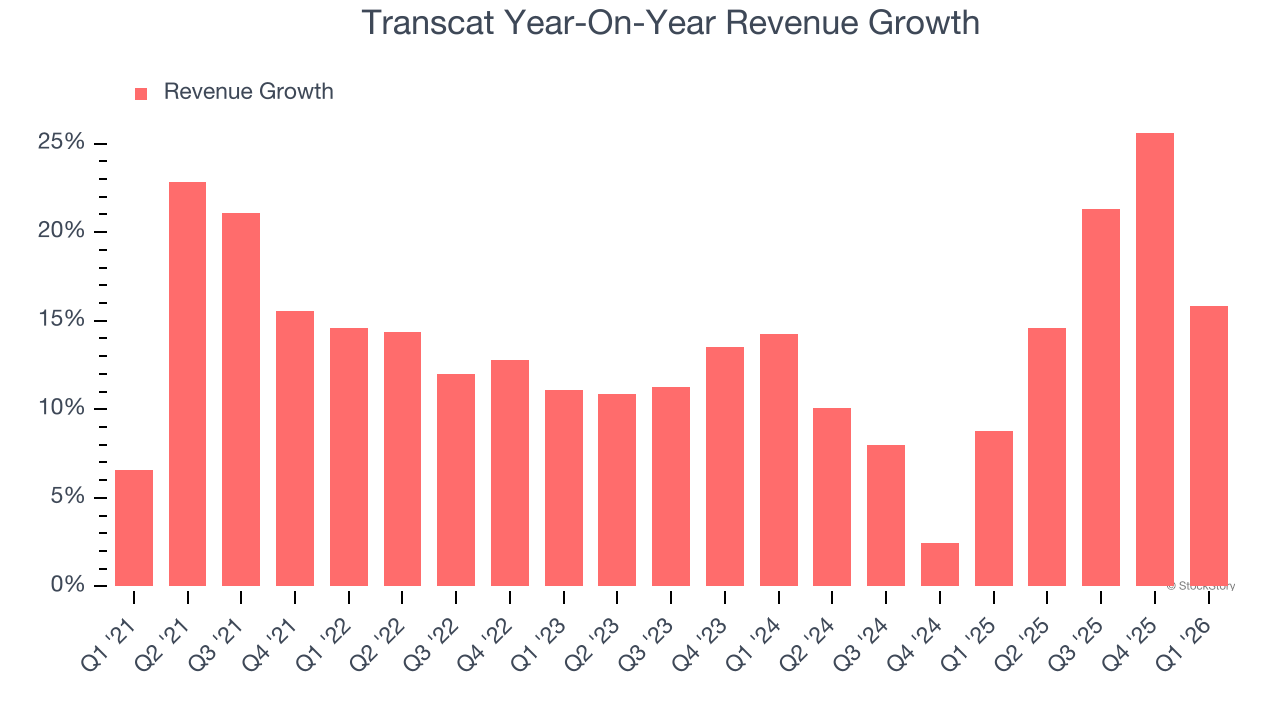

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Transcat grew its sales at an exceptional 13.9% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Transcat’s annualized revenue growth of 13.1% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Transcat’s revenue grew by 15.8% year on year to $89.33 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.7% over the next 12 months, a deceleration versus the last two years. Still, this projection is above average for the sector and implies the market is baking in some success for its newer products and services.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Transcat was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.4% was weak for an industrials business.

Looking at the trend in its profitability, Transcat’s operating margin decreased by 3.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Transcat’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Transcat generated an operating margin profit margin of 4.8%, down 3.2 percentage points year on year. Since Transcat’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

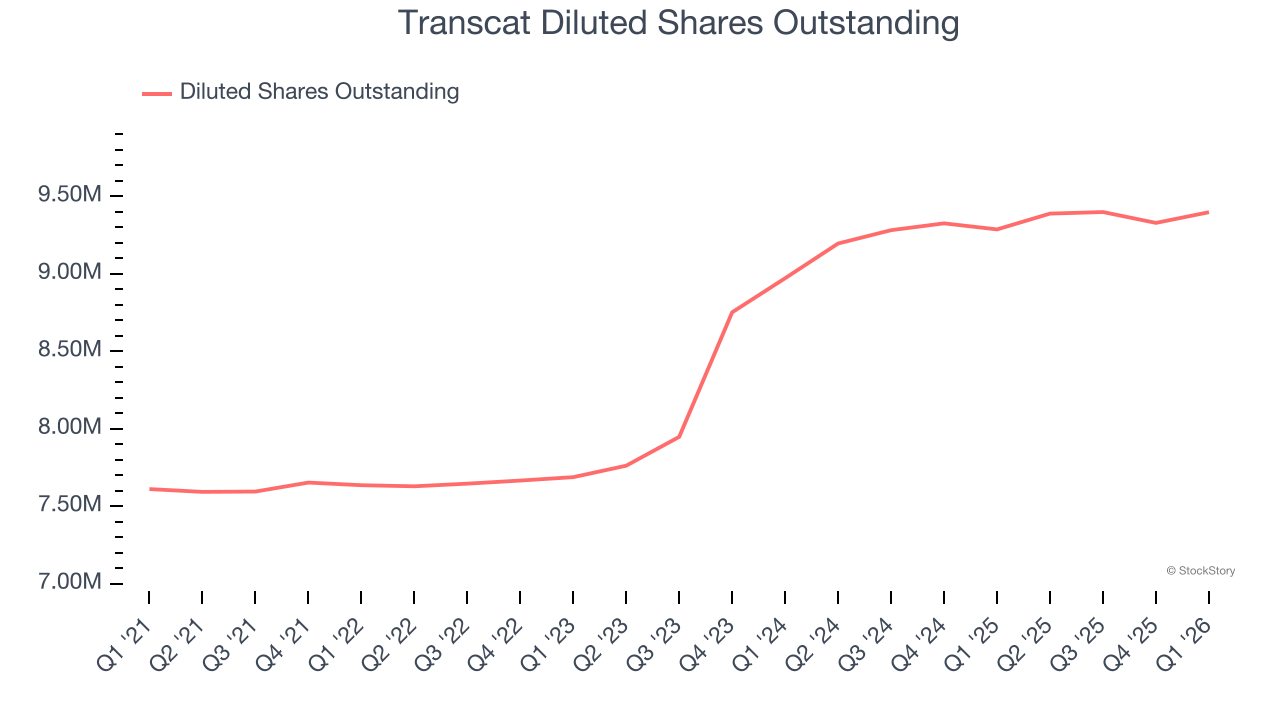

Transcat’s EPS grew at a solid 10.7% compounded annual growth rate over the last five years. However, this performance was lower than its 13.9% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

Diving into Transcat’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Transcat’s operating margin declined by 3.3 percentage points over the last five years. Its share count also grew by 23.5%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Transcat, its two-year annual EPS declines of 11.1% mark a reversal from its (seemingly) healthy five-year trend. We hope Transcat can return to earnings growth in the future.

In Q1, Transcat reported adjusted EPS of $0.56, down from $0.64 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Transcat’s full-year EPS to grow 15% from $1.85 to $2.13.

Key Takeaways from Transcat’s Q1 Results

We enjoyed seeing Transcat beat analysts’ EBITDA expectations this quarter. On the other hand, its adjusted operating income missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $76.71 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).