Shareholders of The Trade Desk would probably like to forget the past six months even happened. The stock dropped 46.6% and now trades at $19.71. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Given the weaker price action, is now the time to buy TTD? Find out in our full research report, it’s free.

Why Does The Trade Desk Spark Debate?

Built as an alternative to "walled garden" advertising ecosystems, The Trade Desk (NASDAQ: TTD) provides a cloud-based platform that helps advertisers and agencies plan, manage, and optimize digital advertising campaigns across multiple channels and devices.

Two Positive Attributes:

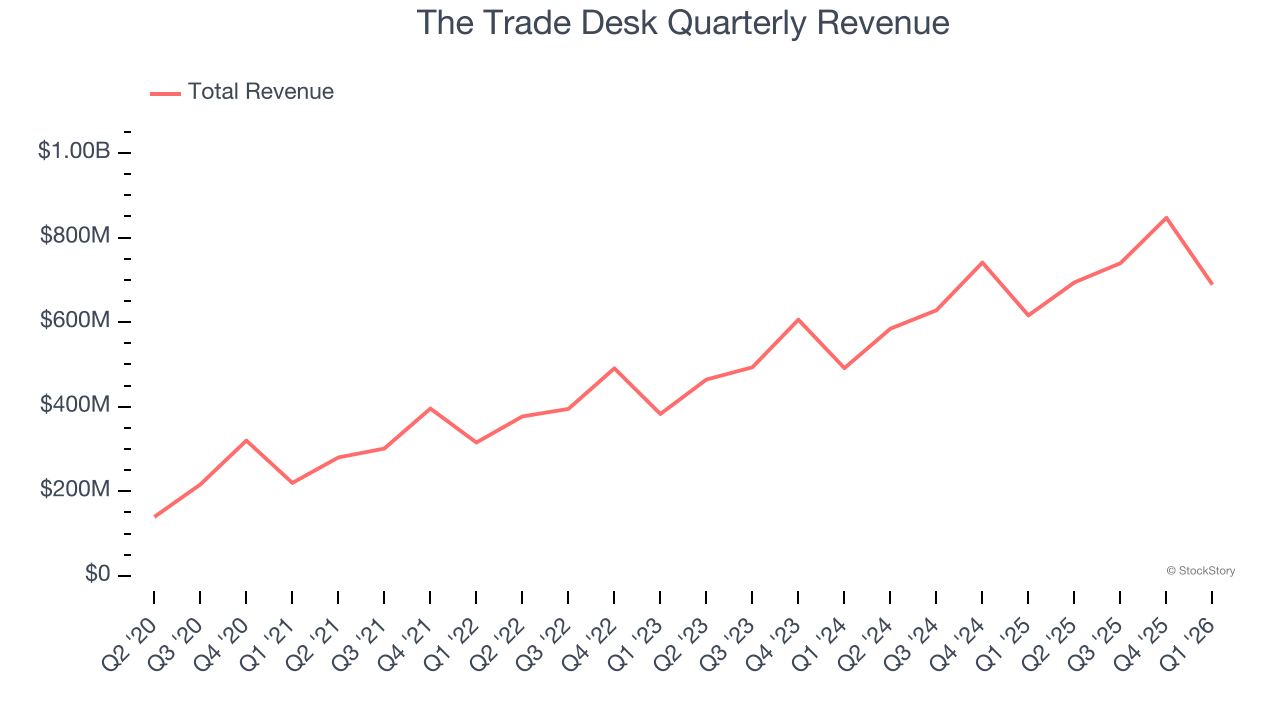

1. Skyrocketing Revenue Shows Strong Momentum

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, The Trade Desk’s sales grew at an impressive 27.1% compounded annual growth rate over the last five years. Its growth surpassed the average software company and shows its offerings resonate with customers.

2. Customer Acquisition Costs Are Recovered in Record Time

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

The Trade Desk is extremely efficient at acquiring new customers, and its CAC payback period checked in at 5.5 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

One Reason to Be Careful:

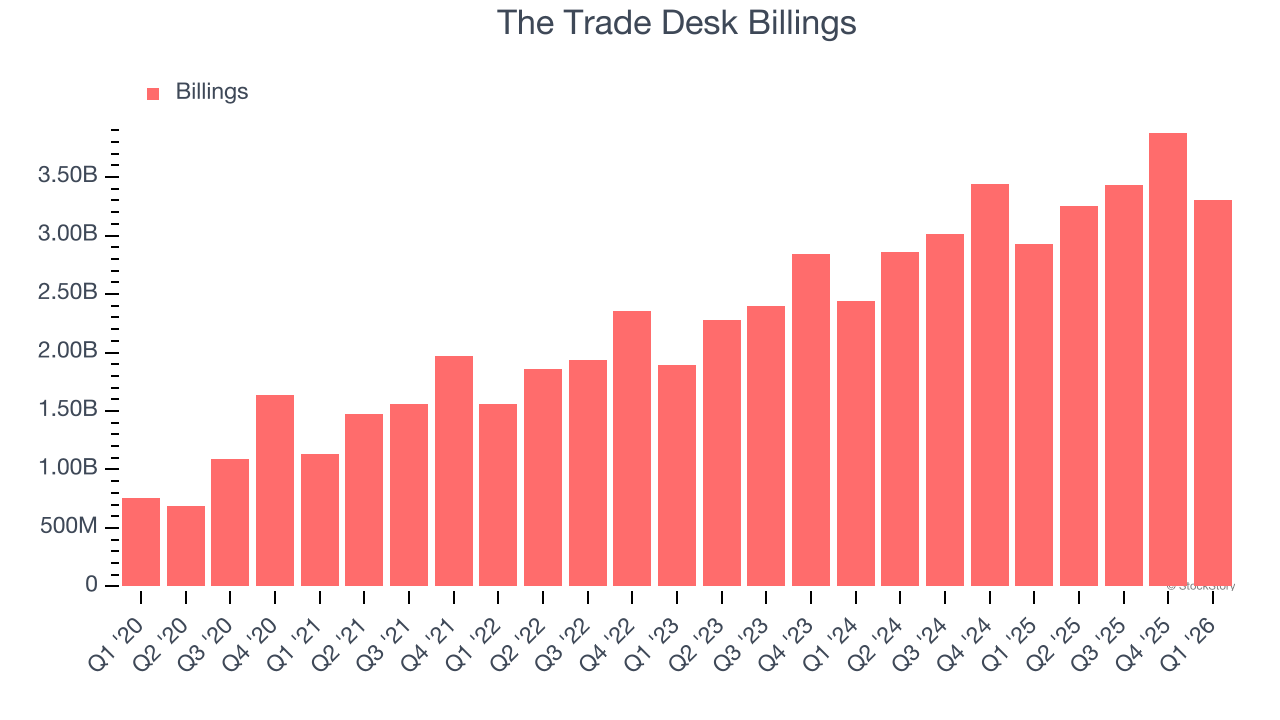

Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

The Trade Desk’s billings came in at $3.3 billion in Q1, and over the last four quarters, its year-on-year growth averaged 13.3%. This performance slightly lagged the sector and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Final Judgment

The Trade Desk’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 2.8× forward price-to-sales (or $19.71 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.