What a brutal six months it’s been for DraftKings. The stock has dropped 24.3% and now trades at $26.47, rattling many shareholders. This may have investors wondering how to approach the situation.

Is now the time to buy DraftKings, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think DraftKings Will Underperform?

Despite the more favorable entry price, we’re swiping left on DraftKings for now. Here are three reasons why there are better opportunities than DKNG, plus one stock we’d rather own.

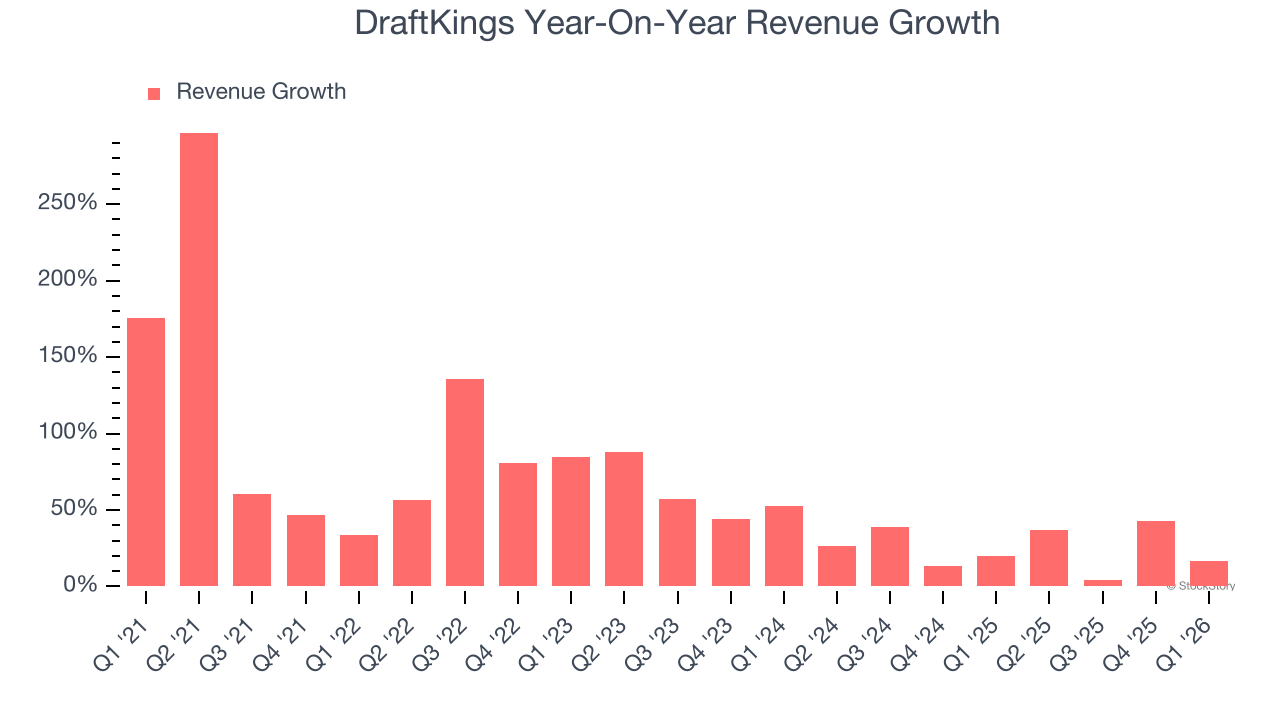

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. DraftKings’s recent performance shows its demand has slowed as its annualized revenue growth of 24.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

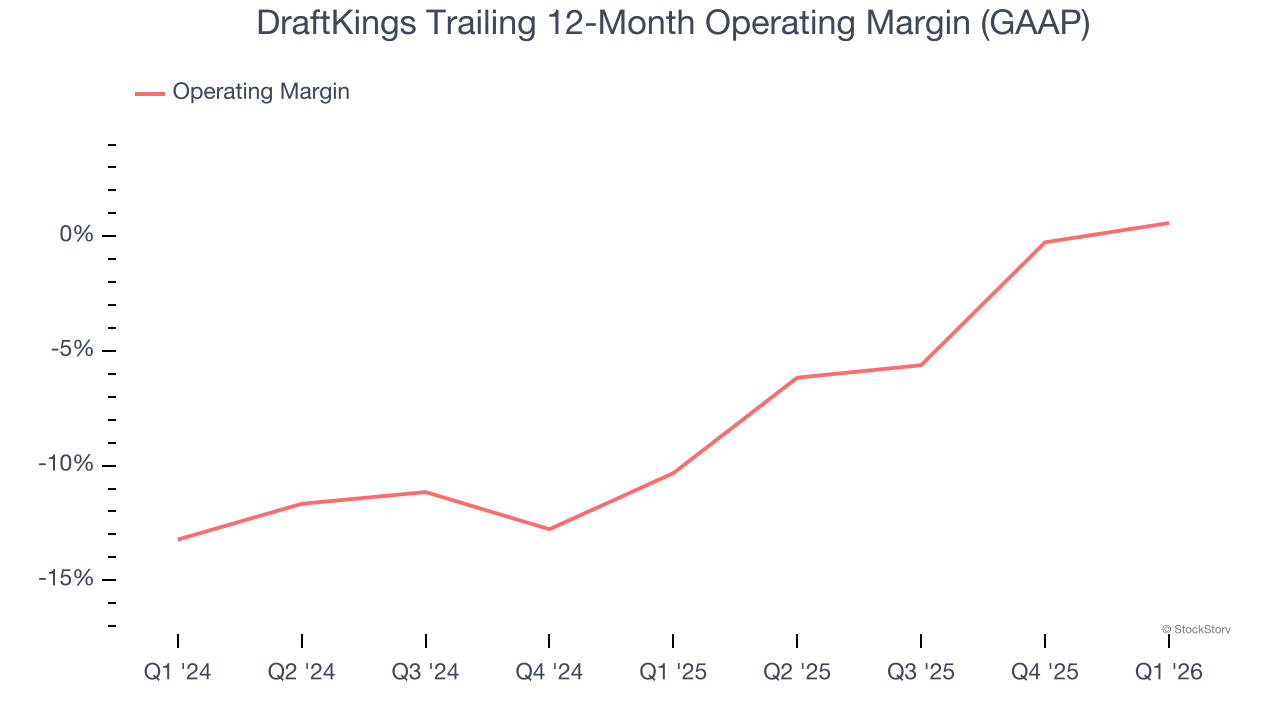

2. Operating Losses Sound the Alarm

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

DraftKings’s operating margin has risen over the last 12 months, but it still averaged negative 4.3% over the last two years. This is due to its large expense base and inefficient cost structure.

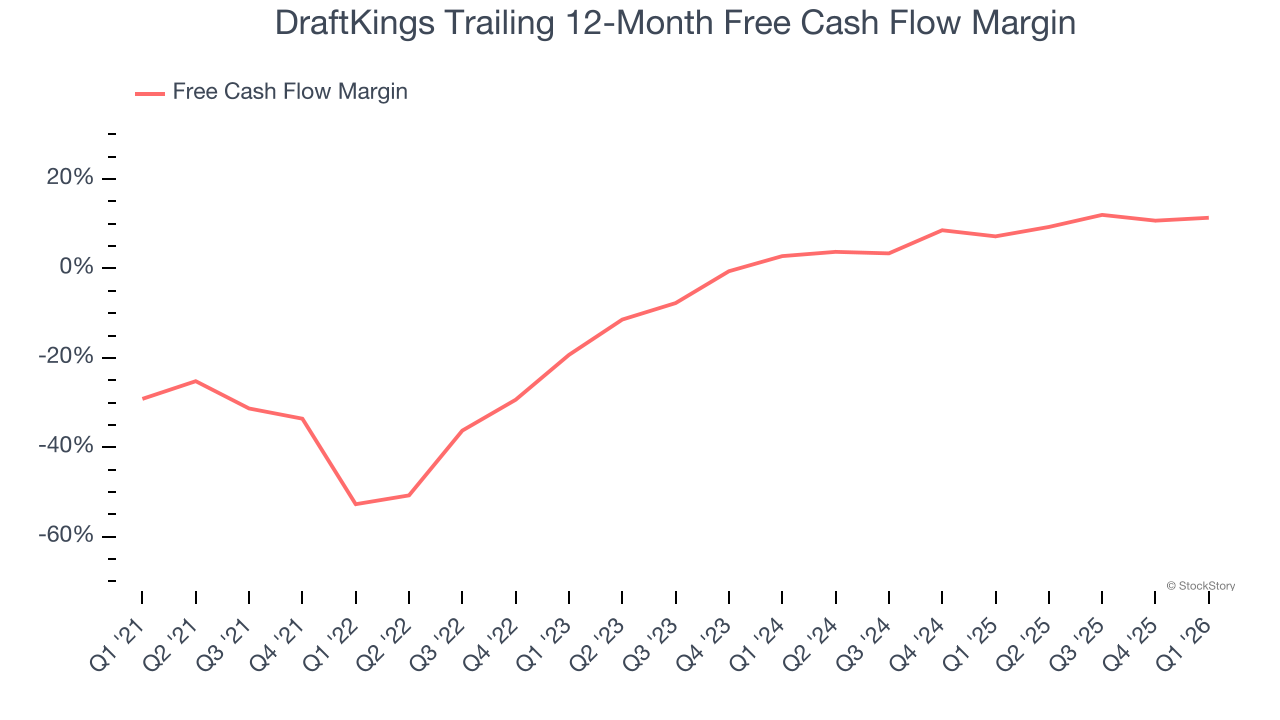

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

DraftKings has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 9.5%, below what we’d expect for a consumer discretionary business.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of DraftKings, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at 21.5× forward P/E (or $26.47 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. We’d recommend looking at one of our top software and edge computing picks.

Stocks We Like More Than DraftKings

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.