Williams-Sonoma trades at $217.70 and has moved in lockstep with the market. Its shares have returned 5.5% over the last six months while the S&P 500 has gained 7.2%.

Is now the time to buy Williams-Sonoma, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Williams-Sonoma Not Exciting?

We’re sitting this one out for now. Here are three reasons why WSM doesn’t excite us, plus one stock we’d rather own.

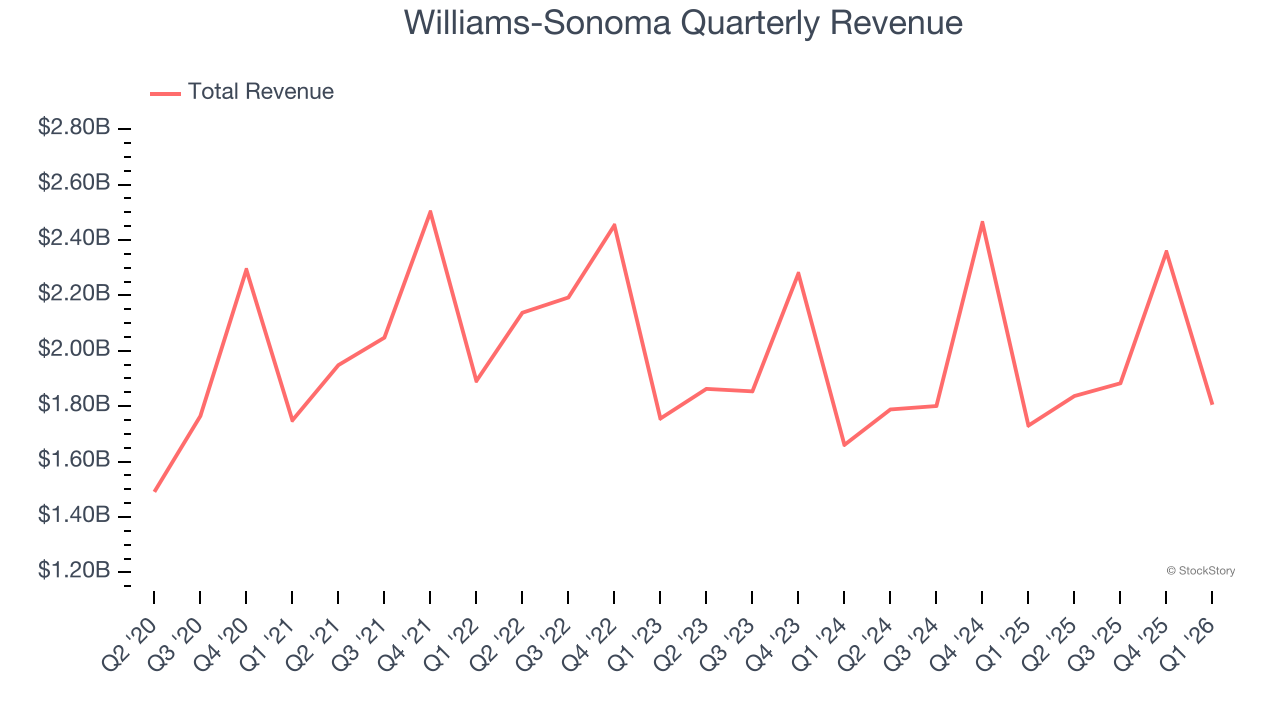

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Williams-Sonoma’s demand was weak and its revenue declined by 2.6% per year. This was below our standards and is a sign of lacking business quality.

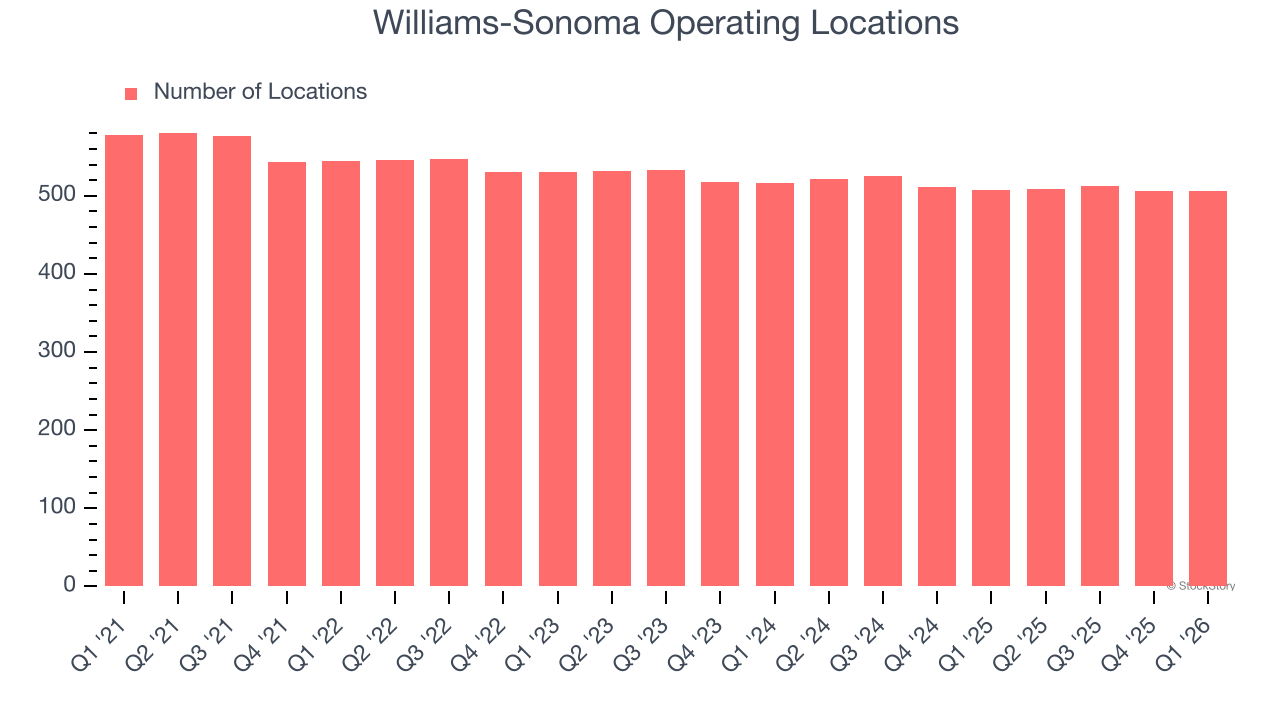

2. Stores Are Closing, a Headwind for Revenue

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Williams-Sonoma operated 506 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 1.6% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

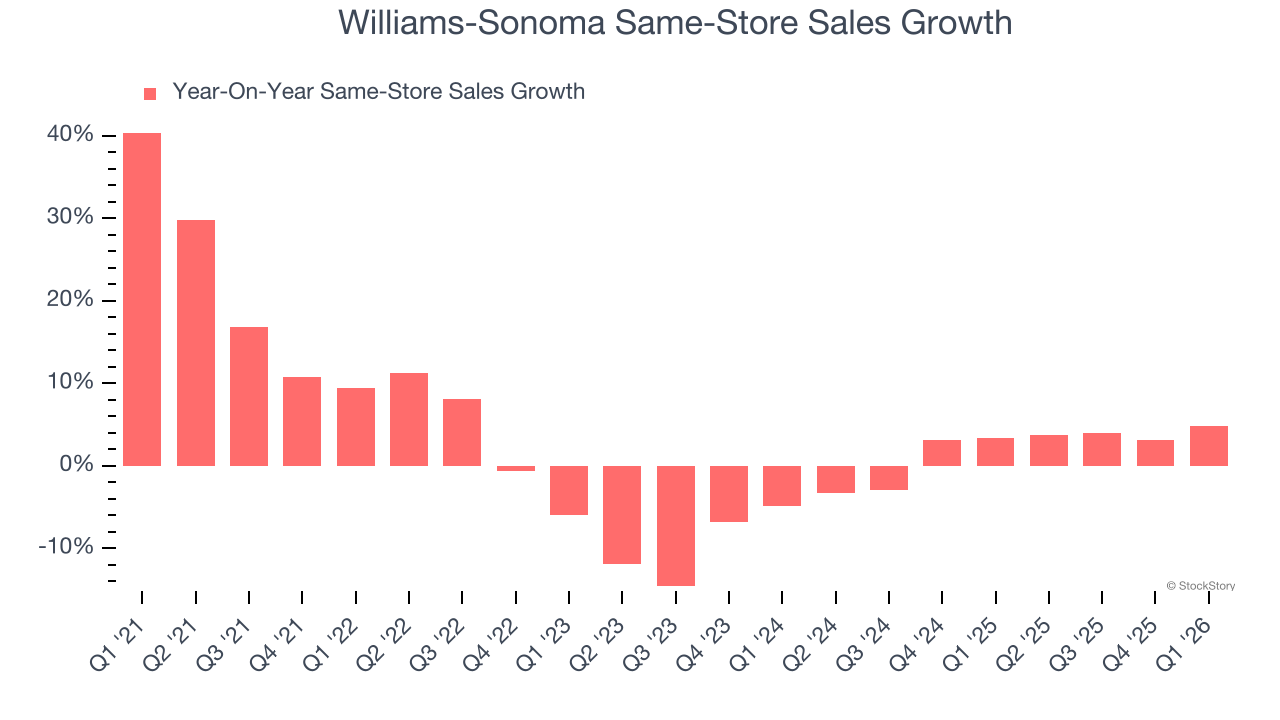

3. Same-Store Sales Falling Behind Peers

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Williams-Sonoma’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 2% per year.

Final Judgment

Williams-Sonoma’s business quality ultimately falls short of our standards. That said, the stock currently trades at 22.9× forward P/E (or $217.70 per share). This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward a dominant aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of Williams-Sonoma

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.