As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the property & casualty insurance industry, including Skyward Specialty Insurance (NASDAQ: SKWD) and its peers.

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

The 32 property & casualty insurance stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 1.9%.

Luckily, property & casualty insurance stocks have performed well with share prices up 10.8% on average since the latest earnings results.

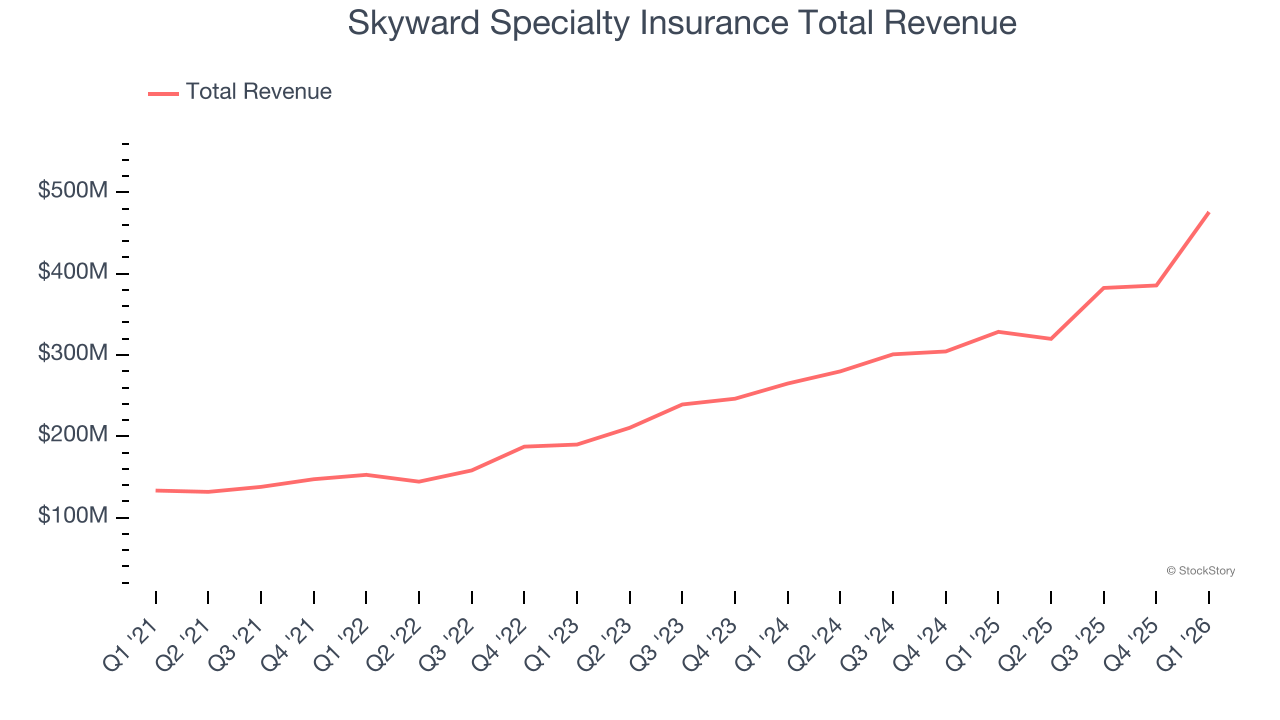

Skyward Specialty Insurance (NASDAQ: SKWD)

Founded in 2006 to serve markets where standard insurance coverage falls short, Skyward Specialty Insurance (NASDAQ: SKWD) provides customized commercial property, casualty, and health insurance solutions for underserved or specialized market niches.

Skyward Specialty Insurance reported revenues of $475.9 million, up 44.8% year on year. This print exceeded analysts’ expectations by 12.2%. Overall, it was an exceptional quarter for the company with a solid beat of analysts’ net premiums earned and EPS estimates.

Skyward Group Chairman and CEO Andrew Robinson commented, “We are off to an excellent start to the year as we report our first quarter consolidated results for Skyward Specialty and Apollo under the Skyward Group brand. Diluted operating EPS of $1.25 increased 39% year over year, driven by strong underlying earnings growth and the accretive consolidation of Apollo. Our annualized operating return on equity of 20% reflects the strength and quality of our performance. We delivered an outstanding combined ratio of 89.5%, inclusive of 1.8 points of catastrophe losses. Pro forma gross written premiums growth of 10% was solid, while total managed premiums grew 20%, including 49% growth in fee generating gross written premiums, an encouraging early indicator of the fee based earnings growth we expect over time. Most importantly, the continued diversification of our portfolio, particularly in lines with lower exposure to P&C underwriting cycles, positions us to deliver strong top‑line and bottom‑line results in a disciplined manner, consistent with our commitment to top‑quartile performance across the market cycle.”

Interestingly, the stock is up 37% since reporting and currently trades at $60.06.

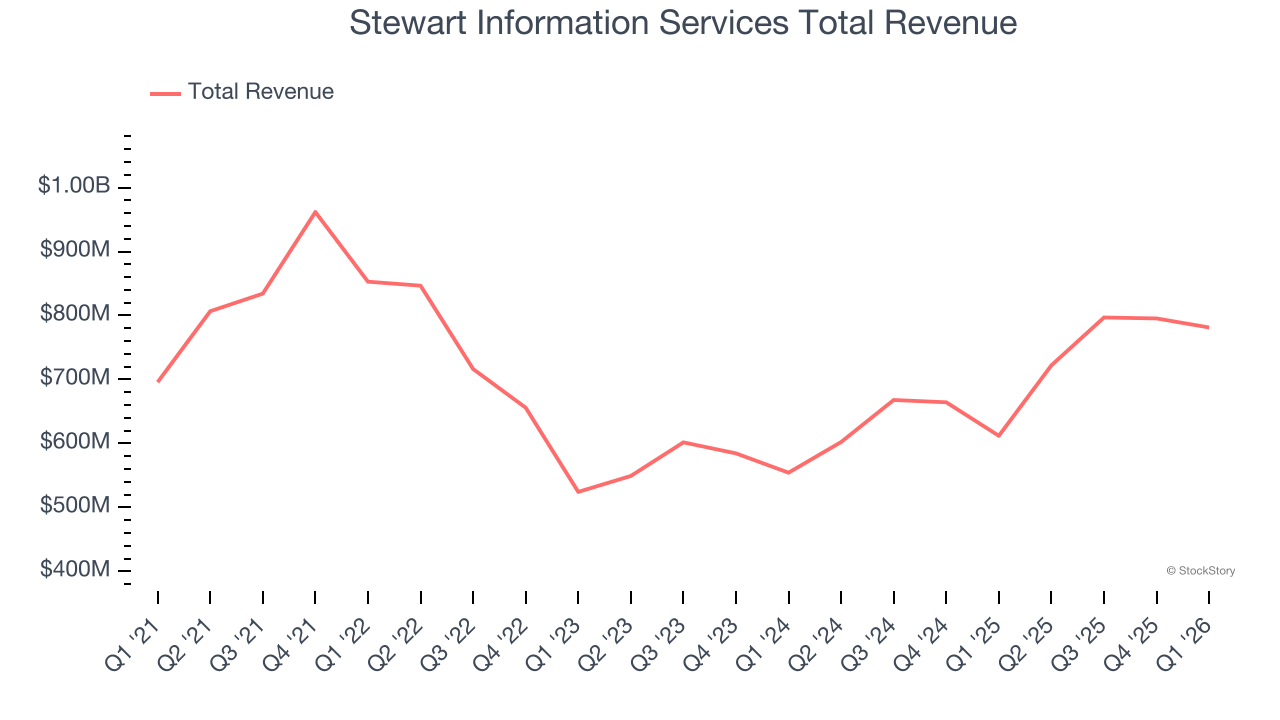

Best Q1: Stewart Information Services (NYSE: STC)

Founded in 1893 during America's westward expansion when property records were often disputed, Stewart Information Services (NYSE: STC) provides title insurance and real estate services, helping homebuyers, sellers, and lenders verify property ownership and protect against title defects.

Stewart Information Services reported revenues of $781.3 million, up 27.7% year on year, outperforming analysts’ expectations by 4.6%. The business had an incredible quarter with a beat of analysts’ EPS estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $68.03.

Is now the time to buy Stewart Information Services? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Fidelity National Financial (NYSE: FNF)

Issuing more title insurance policies than any other company in the United States, Fidelity National Financial (NYSE: FNF) provides title insurance and escrow services for real estate transactions while also offering annuities and life insurance through its F&G subsidiary.

Fidelity National Financial reported revenues of $3.23 billion, up 18.2% year on year, falling short of analysts’ expectations by 10.7%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates.

Fidelity National Financial delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 4.1% since the results and currently trades at $49.17.

Read our full analysis of Fidelity National Financial’s results here.

Assured Guaranty (NYSE: AGO)

Serving as a financial safety net for over $11 trillion in debt service payments since its founding in 2003, Assured Guaranty (NYSE: AGO) provides credit protection products that guarantee scheduled payments on municipal bonds, infrastructure projects, and structured finance obligations.

Assured Guaranty reported revenues of $261 million, down 24.3% year on year. This print surpassed analysts’ expectations by 30.6%. It was a very strong quarter as it also put up a beat of analysts’ EPS estimates.

Assured Guaranty pulled off the biggest analyst estimate beat but had the slowest revenue growth among its peers. The stock is flat since reporting and currently trades at $82.47.

Read our full, actionable report on Assured Guaranty here, it’s free.

Allstate (NYSE: ALL)

Born from a Sears, Roebuck & Co. initiative during the Great Depression with its famous "You're in good hands" slogan, Allstate (NYSE: ALL) is one of America's largest personal property and casualty insurers, offering protection for autos, homes, and personal property.

Allstate reported revenues of $17.35 billion, up 3.2% year on year. This number topped analysts’ expectations by 3%. It was a very strong quarter as it also recorded a beat of analysts’ EPS estimates and a solid beat of analysts’ net premiums earned estimates.

The stock is up 17.4% since reporting and currently trades at $249.19.

Read our full, actionable report on Allstate here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.