The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Comstock Resources (NYSE: CRK) and the rest of the upstream natural gas e&p stocks fared in Q1.

Natural gas-focused E&P companies explore, develop, and produce natural gas resources serving power generation, industrial, and export markets. Natural gas is often positioned as a transition fuel given lower carbon intensity versus coal and oil. Tailwinds include growing LNG (liquefied natural gas) export demand, power generation switching from coal, and industrial consumption growth. Headwinds include natural gas price volatility driven by weather, storage levels, and competing supply sources. Infrastructure constraints may limit market access, while long-term demand faces uncertainty from renewable energy expansion and electrification trends potentially reducing gas consumption.

The 6 upstream natural gas e&p stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 4.3%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 14% since the latest earnings results.

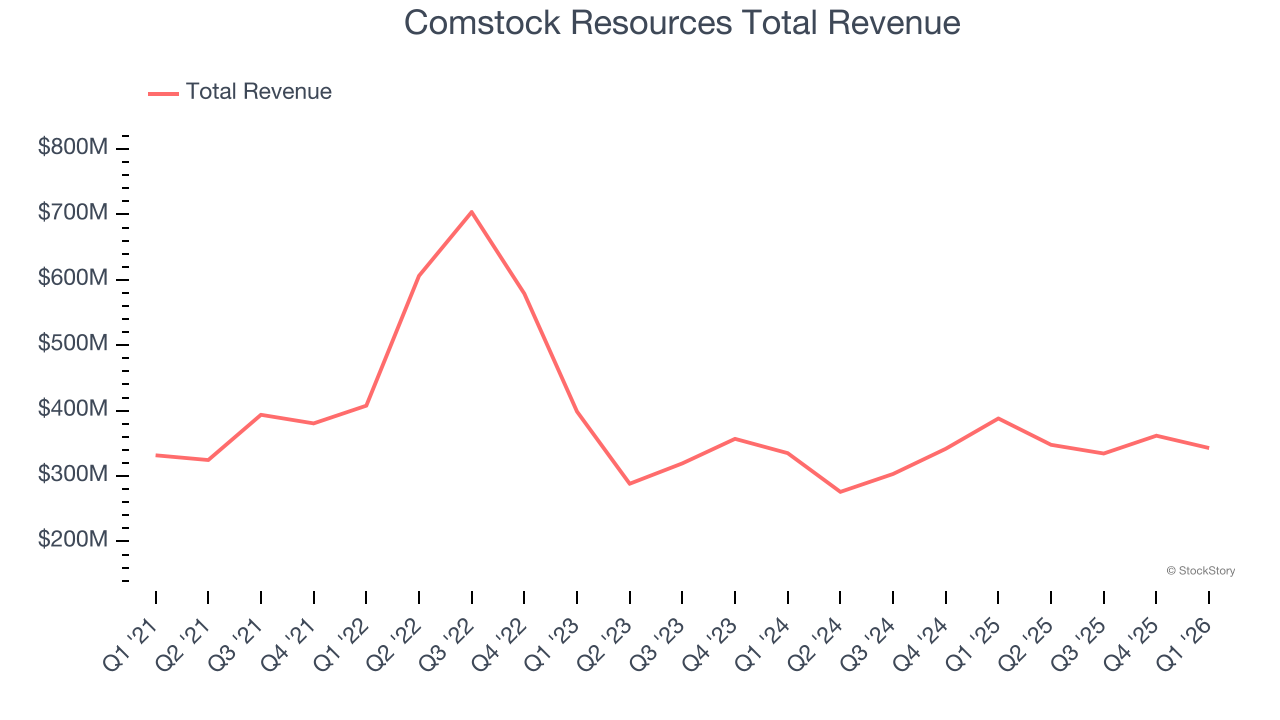

Weakest Q1: Comstock Resources (NYSE: CRK)

Operating in the Haynesville shale where a single well can produce millions of cubic feet of gas daily, Comstock Resources (NYSE: CRK) drills for and produces natural gas from underground shale rock formations in Louisiana and Texas.

Comstock Resources reported revenues of $342.9 million, down 11.7% year on year. This print fell short of analysts’ expectations by 31.7%. Overall, it was a disappointing quarter for the company with a significant miss of analysts’ EBITDA and EPS estimates.

Comstock Resources delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. The market seems disappointed with the results as the stock is down 21.2% since reporting and currently trades at $13.65.

Read our full report on Comstock Resources here, it’s free.

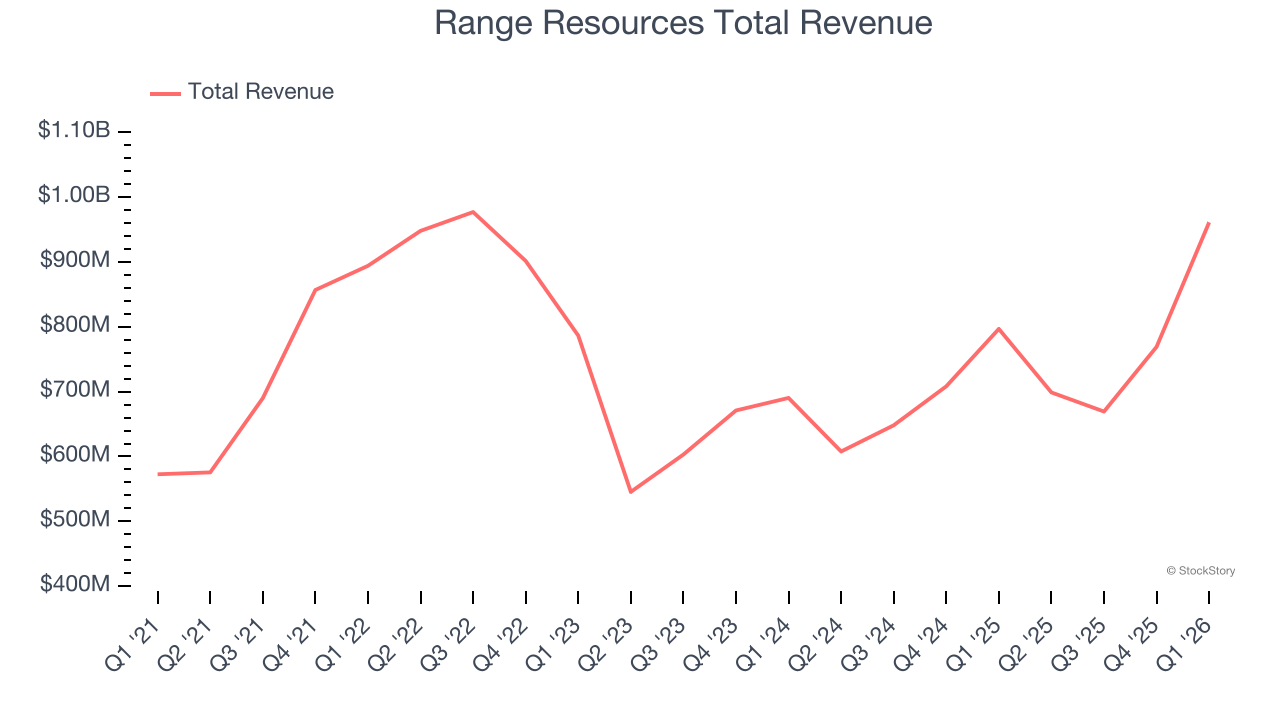

Best Q1: Range Resources (NYSE: RRC)

Focused almost entirely on the Marcellus Shale beneath Pennsylvania's forests and farmland, Range Resources (NYSE: RRC) drills for and produces natural gas, natural gas liquids, and oil from shale formations.

Range Resources reported revenues of $961.1 million, up 20.6% year on year, outperforming analysts’ expectations by 7.6%. The business had an incredible quarter with a solid beat of analysts’ EBITDA and EPS estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 11.3% since reporting. It currently trades at $36.97.

Is now the time to buy Range Resources? Access our full analysis of the earnings results here, it’s free.

EQT (NYSE: EQT)

The largest natural gas producer in the United States by daily volume, EQT (NYSE: EQT) produces natural gas and natural gas liquids from wells drilled in the Appalachian Basin.

EQT reported revenues of $3.14 billion, up 45.7% year on year, falling short of analysts’ expectations by 1.7%. Still, it was a satisfactory quarter as it posted a solid beat of analysts’ EBITDA estimates.

As expected, the stock is down 11.4% since the results and currently trades at $50.48.

Read our full analysis of EQT’s results here.

Antero Resources (NYSE: AR)

Holding roughly 521,000 net acres across West Virginia, Ohio, and Pennsylvania, Antero Resources (NYSE: AR) drills and produces natural gas, natural gas liquids, and oil from underground rock formations in the Appalachian Basin.

Antero Resources reported revenues of $1.90 billion, up 43.4% year on year. This result topped analysts’ expectations by 16.8%. It was a strong quarter as it also put up EPS in line with analysts’ estimates.

The stock is down 11.6% since reporting and currently trades at $34.49.

Read our full, actionable report on Antero Resources here, it’s free.

BKV (NYSE: BKV)

Operating a "closed-loop" model linking gas production to carbon capture, BKV (NYSE: BKV) produces natural gas from shale formations in Texas and Pennsylvania, selling it to utilities, industrial users, and exporters.

BKV reported revenues of $432.8 million, up 449% year on year. This print surpassed analysts’ expectations by 37.6%. It was a very strong quarter as it also recorded a beat of analysts’ EPS estimates and EBITDA in line with analysts’ estimates.

BKV achieved the biggest analyst estimate beat and fastest revenue growth among its peers. The stock is down 11.6% since reporting and currently trades at $26.38.

Read our full, actionable report on BKV here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.