Over the past six months, Genco has been a great trade, beating the S&P 500 by 25.3%. Its stock price has climbed to $25, representing a healthy 33% increase. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Genco, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Genco Will Underperform?

We’re glad investors have benefited from the price increase, but we’re swiping left on Genco for now. Here are three reasons why GNK doesn’t excite us, plus one stock we’d rather own.

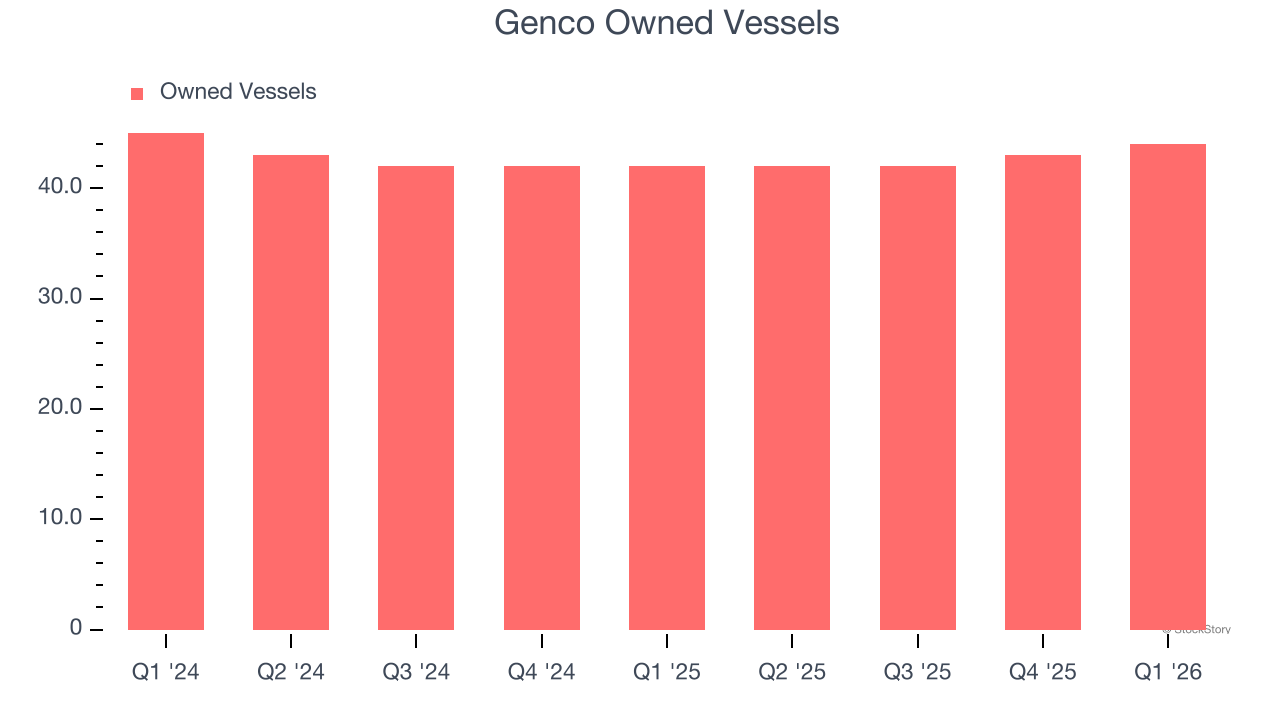

1. Inability to Grow owned vessels Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like Genco, our preferred volume metric is owned vessels). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Over the last two years, Genco failed to grow its owned vessels, which came in at 44 in the latest quarter. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Genco might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

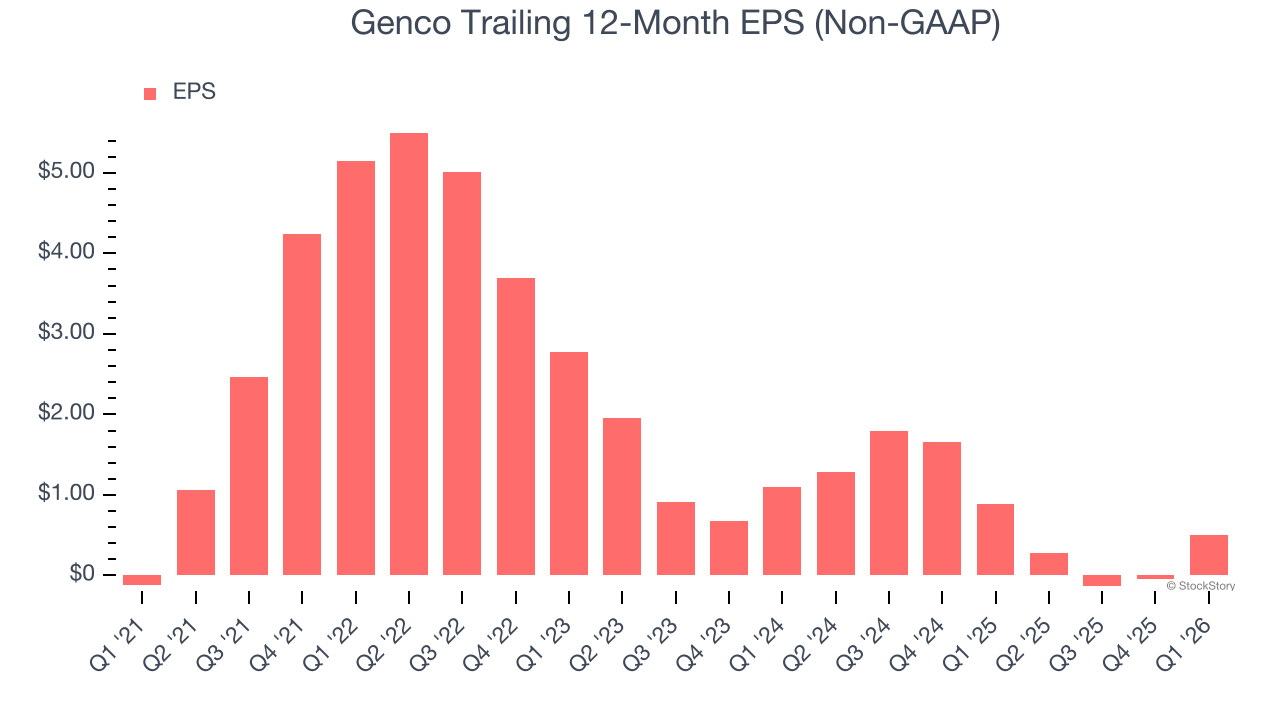

2. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Genco, its EPS declined by 32.6% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

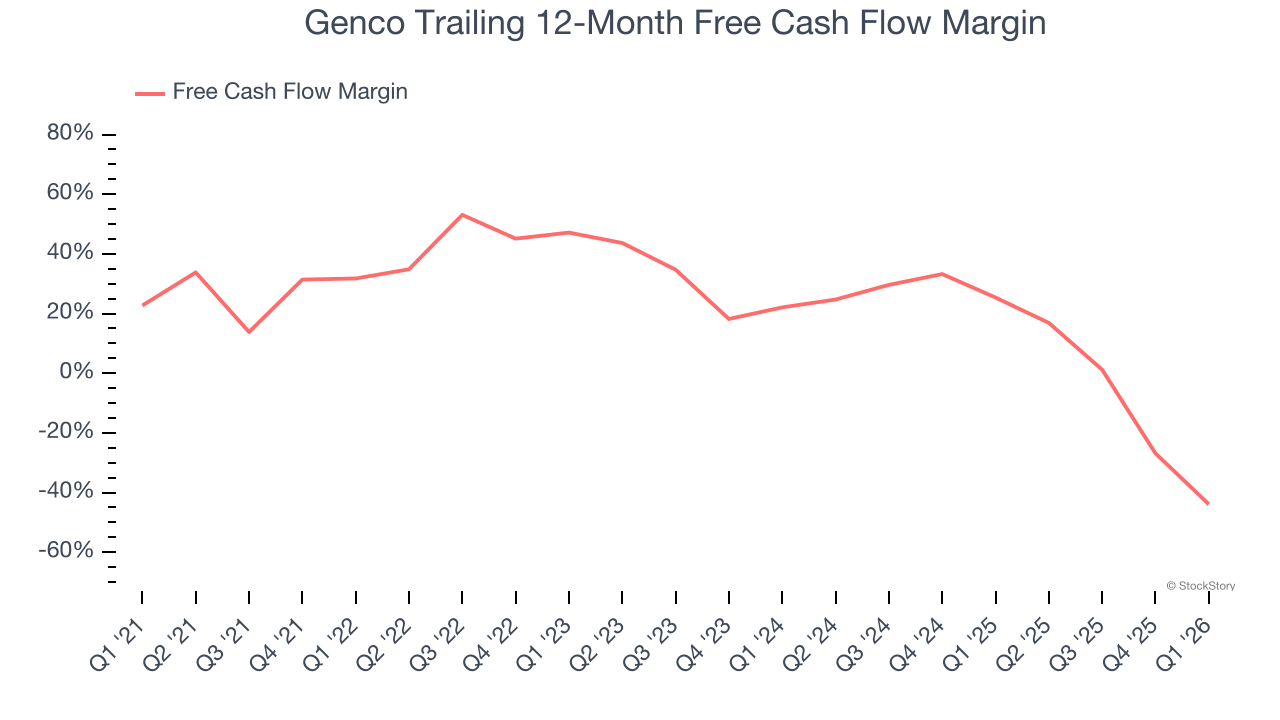

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Genco’s margin dropped by 75.7 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Genco’s free cash flow margin for the trailing 12 months was negative 43.9%.

Final Judgment

We see the value of companies helping their customers, but in the case of Genco, we’re out. With its shares outperforming the market lately, the stock trades at 16.8× forward P/E (or $25 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better investments elsewhere. Let us point you toward the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.