The Walt Disney Company (DIS) dominated the entertainment industry for decades, where movies became merchandise empires, theme park attractions, cruises, television franchises, and lifelong nostalgia stories. Then, Netflix (NFLX) arrived, and the global pandemic cemented the company’s position as the king of online streaming. Disney responded aggressively with Disney+, entering a brutal streaming war that reshaped the entire media industry.

However, now Disney is quietly preparing for something much bigger. In the recent Q2 earnings call, CEO Josh D'Amaro revealed the company’s new strategy that hinted that its next competition may not come from Netflix at all.

Let’s take a look at what Disney’s new strategy is.

Streaming Is Becoming a Much Stronger Business

Disney second quarter showed that the company is no longer obsessed with subscriber growth. Total revenue rose 7% year-over-year (YOY) to $25.2 billion, with 8.3% increase in adjusted earnings to $1.57 per share. Disney's SVOD (Subscription Video on Demand) segment grew 11% sequentially, as subscription revenue increased because of both higher pricing and subscriber volume growth.

But the real winner is Disney’s intellectual property, which remains the backbone of its streaming strategy. Some of the successful returning series such as High Potential and Paradise, alongside new projects like Love Story: John F. Kennedy Jr. & Carolyn Bessette, were the highlights of the quarter. Notably, films like Zootopia 2, generated a massive $1.9 billion at the global box office. The company revealed that the broader Zootopia franchise has now surpassed one billion streamed hours on Disney+. This shows the extent of the successful intellectual property which continues to create value beyond its theatrical release.

But Disney’s Biggest Advantage Is Physical

Disney still has an edge over Netflix and other streaming platforms because of the physical experiences it provides its consumers. In the second quarter, Disney Experiences delivered revenue growth of 7% and operating income increase of 5%. During the quarter, Disney expanded its global experiences footprint. Disney Cruise Line introduced the Disney Adventure, its first cruise ship based in Asia. Meanwhile, Disneyland Paris opened the new World of Frozen area as part of its larger park expansion and makeover project. These projects aim to Disney’s reach into new international markets. Management sees long-term opportunity across parks, cruise lines, and immersive experiences.

Disney is now competing for consumer attention against gaming platforms, social media ecosystems, live sports networks, and even large tech companies. Its new competitors will now be YouTube, TikTok, Roblox, Fortnite, Amazon (AMZN), Apple (AAPL), and any platform that can capture hours of consumer involvement every day. Disney also views ESPN as a key growth driver, with sports driving recurring engagement and creating premium advertising opportunities.

Every great story faces some hiccups, and the hidden risk here is that Disney’s future is dependent on blockbuster franchises. If franchise fatigue eventually grows, Disney’s strategy could face pressure across several business segments all at once. However, Disney appears confident that its scale, storytelling power, and ecosystem approach can outweigh those risks over the long term.

Is Disney Stock a Buy Now?

Disney may no longer be trying to win the streaming wars. Instead, it is creating an entertainment ecosystem that will monetize customer attention across both the digital and physical worlds. Investors who believe Disney can successfully build an entertainment platform that no competitor can fully replicate, might find the stock a good buy on the dip now. Disney stock is down 7.34% year-to-date (YTD), underperforming the broader market gain.

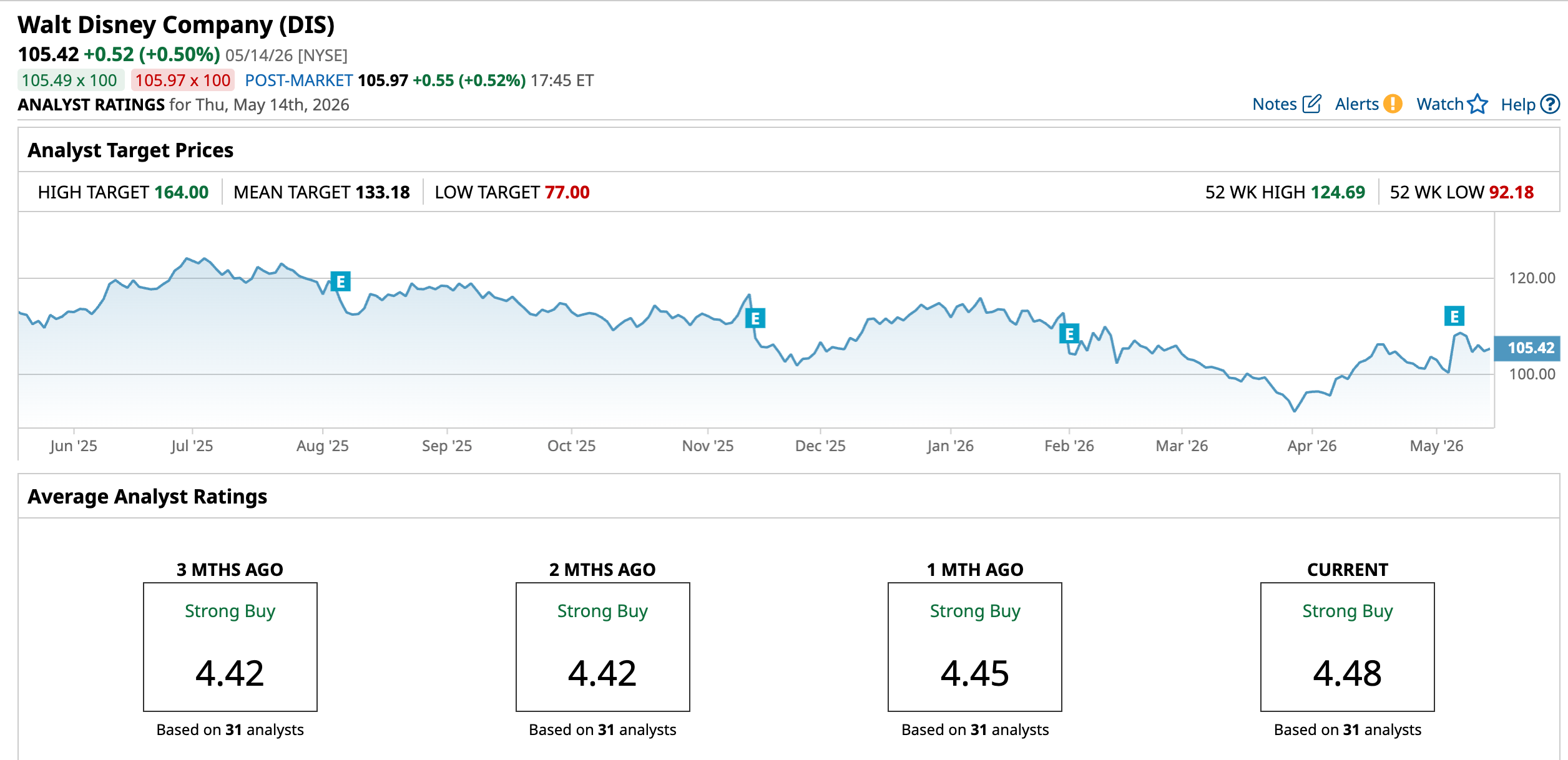

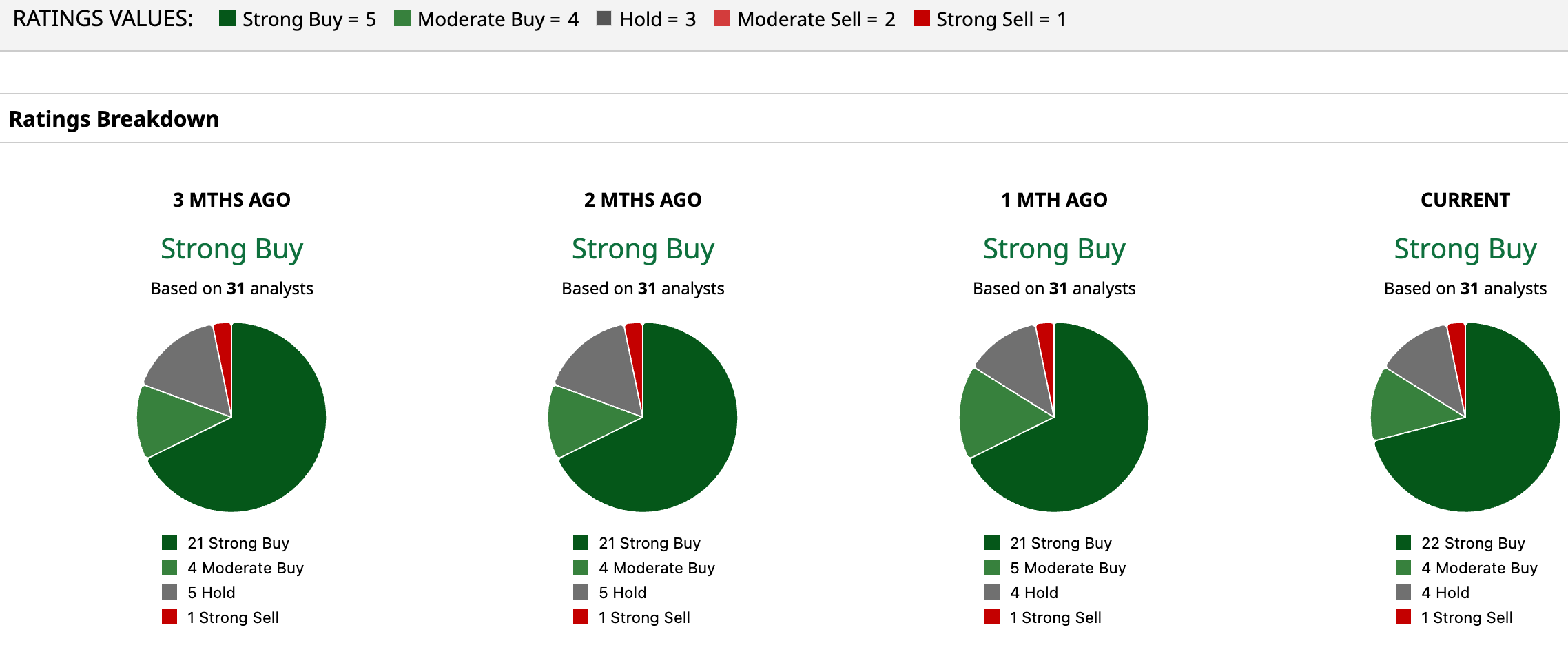

On Wall Street, DIS stock remains an overall “Strong Buy.” Of the 31 analysts who cover DIS, 22 recommend it as a "Strong Buy," four suggest a "Moderate Buy," four rate it a "Hold” and one says it is a “Strong Sell.” Analysts have set a mean price target for Disney stock of $133.18, which is 26.3% higher than current levels. Its high target price of $164 indicates an upside of 55.6% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart