The Winona, Minnesota-based Fastenal Company (FAST) supplies manufacturing plants, construction sites, and maintenance crews with the industrial goods. Holding a market cap of roughly $49.7 billion, it carries fasteners, bolts, nuts, screws, anchors, rivets, metal framing systems, and a wide assortment of hardware products.

The company also takes the complexity out of keeping shelves stocked by offering inventory management, supply chain support, vending solutions, and logistics services that help businesses handle their industrial supplies.

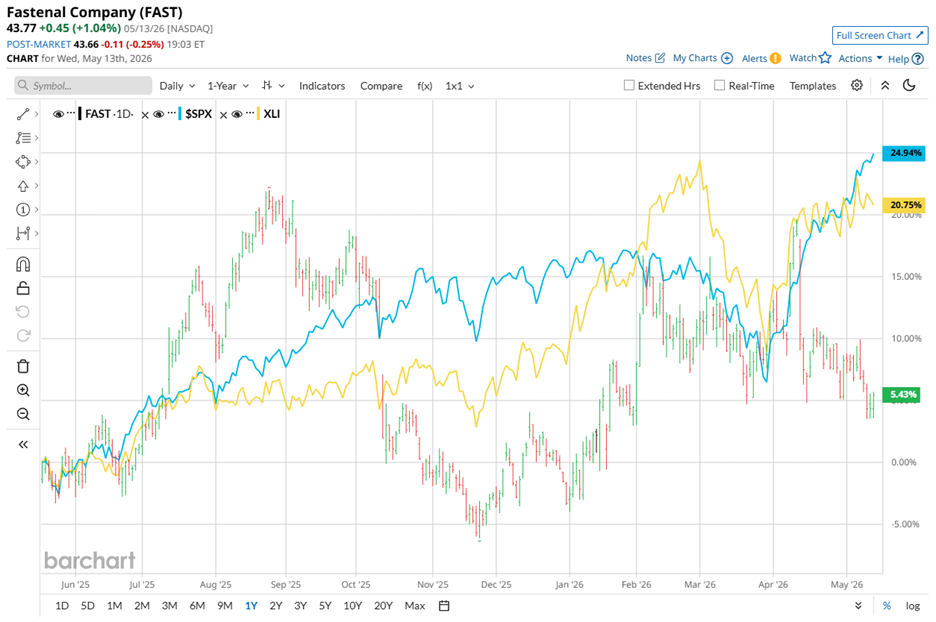

On the price performance front, FAST stock posted a 9.5% gain over the past 52 weeks. The S&P 500 Index ($SPX) left it in the dust with a 26.5% run over the same stretch. However, year-to-date (YTD), FAST stock has climbed 9.1% while the broader index logged an 8.8% gain, giving Fastenal a slight edge in the more recent stretch.

A wider look under the hood shows FAST stock trailing its own sector as well. The State Street Industrial Select Sector SPDR ETF (XLI) surged 22.9% over the past 52 weeks and sits 11.9% higher on an YTD basis.

Against that backdrop, Fastenal rolled out its Q1 FY2026 earnings on April 13. Revenue climbed 12.4% year over year to $2.20 billion, slipping past analyst expectations of $2.19 billion. EPS reached $0.30, marking a 15.4% jump from the prior year while matching Wall Street estimates exactly at $0.30.

Despite those numbers, the stock dropped 6.9% on the day of announcement because investors zeroed in on gross margin shrinking by 50 basis points to 44.6% as inflation and tariff related cost pressures tightened the screws.

Expenses rose faster than Fastenal could pass costs onto customers, while tariff uncertainty encouraged buyers to sit tight and postpone purchasing decisions. CEO Dan Florness did not sugarcoat the outlook and warned that Q2 would continue sailing through choppy waters.

For FY2026, which ends in December, analysts expect diluted EPS to increase 12.8% year over year to $1.23, signaling that earnings momentum still has fuel in the tank. Notably, Fastenal surpassed EPS estimates in one of the past four quarters, stayed flat in two others, and missed estimates in the remaining quarter.

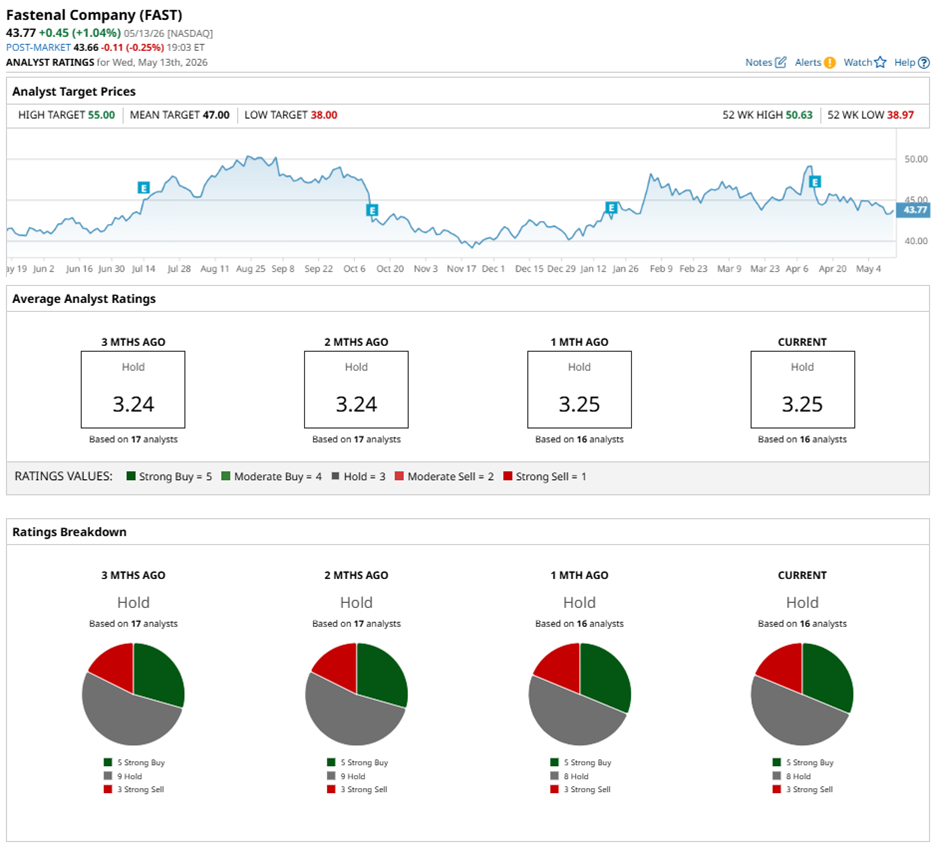

Wall Street, for its part, has planted FAST stock in "Hold" territory. Among the 16 analysts covering the stock, five carry a "Strong Buy," eight sit on "Hold," and three push a "Strong Sell."

Analyst sentiment has not budged much during the past three months. Nine analysts backed a “Hold” rating then, and eight analysts continue holding their ground now.

However, some analysts are seeing light at the end of the tunnel. Guy Hardwick of Barclays has nudged the FAST stock price target up to $45 from $44 while keeping an “Equalweight” rating on the industrial distributor’s shares.

To that end, the average price target of $47 implies potential upside of 7.4%, while the Street-High target of $55 points to a possible gain of 25.7% from current levels. Even so, the broader outlook keeps one foot on the brake given the current volatility in the company's fundamentals.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Dear Lumentum Stock Fans, Mark Your Calendars for May 18

- Why GameStop Stock Is Nosediving After Its Audacious eBay Offer Failed

- Buying CBRS Stock After the Cerebras IPO Is a Bet on Engineering Magic. That Same Magic Could Be the Kiss of Death.

- Why Applied Materials (AMAT) Stock Is a Buy Heading Into Its Earnings