With a market cap of $22.7 billion, Corpay, Inc. (CPAY) is a global payments company that provides businesses and consumers with solutions to manage and pay expenses through services such as corporate payments, vehicle payments, lodging payments, and prepaid cards. It serves a wide range of customers by offering fuel and fleet solutions, cross-border and virtual payments, travel and lodging management, and workforce payment services.

The fuel card and payment products provider's shares have lagged behind the broader market over the past 52 weeks. CPAY stock has risen 4.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 29.7%. However, shares of the company are up 13.1% on a YTD basis, outpacing SPX’s 9.9% return.

Looking closer, shares of the Atlanta, Georgia-based company have slightly outperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 3.8% rise over the past 52 weeks.

Shares of CPAY climbed 12.5% following its Q1 2026 results on May 7, including 25% revenue growth to $1.26 billion, 11% organic revenue growth for the fourth consecutive quarter, and a 29% increase in adjusted EPS to $5.80. Investors were also encouraged by profitability improvements, as adjusted EBITDA rose 24% to $688.6 million with EBITDA margins coming in more than 100 basis points above expectations.

Additionally, Corpay raised its full-year 2026 guidance, projecting revenue between $5.25 billion and $5.33 billion and adjusted EPS between $26.30 and $27.10, while forecasting Q2 revenue growth of 18% and adjusted EPS growth of 28%.

For the fiscal year ending in December 2026, analysts expect Corpay’s EPS to surge 26.1% year-over-year to $25.49. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

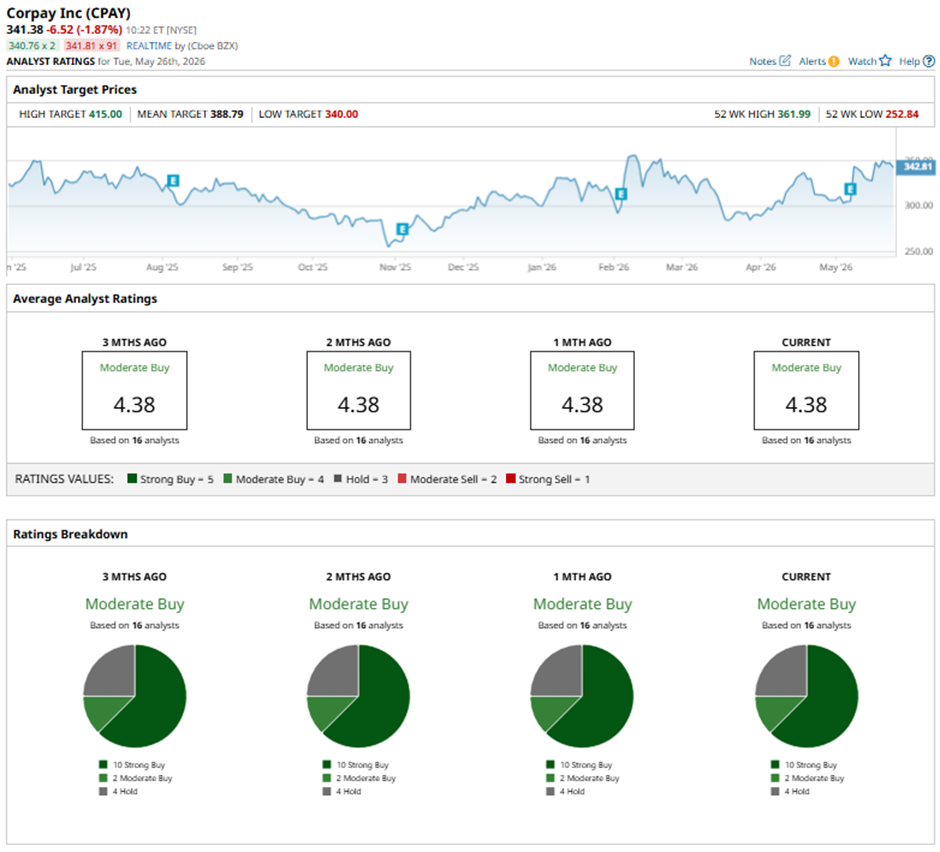

Among the 16 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, two “Moderate Buys,” and four “Holds.”

On May 10, Morgan Stanley raised its price target for CPAY to $400 while maintaining an “Overweight” rating.

The mean price target of $388.79 represents a 13.9% premium to CPAY’s current price levels. The Street-high price target of $415 suggests a 21.6% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Qualcomm Is Teaming Up With ByteDance. What It Means for QCOM Stock

- Datadog Benefits When AI Goes Into Production. Here’s Why You Should Buy DDOG Stock Now.

- Beyond Meat Stock Is Down 12% in the Last Month. Wall Street Is Starting to Bet on Its Turnaround Story.

- MU Stock Alert: Micron Just Joined the Trillion-Dollar Club