According to The New York Times, U.S. forces have recently conducted strikes on Iran’s Gulf Coast. Cynically, this geopolitical flashpoint potentially opens the door to defense contractor Lockheed Martin (LMT). While LMT stock has gained more than 10% on a year-to-date basis, since the beginning of March, the security is down around 20%. As such, it has triggered a Weak Sell warning from the Barchart Technical Opinion indicator.

Nevertheless, as some experts have argued, the correction may represent a buying opportunity for LMT stock. Essentially, LMT was previously perceived to be overbought. With the defense specialist suffering a poor first-quarter earnings report — in which the company slipped against both headline numbers — the underlying security has been rerated to a more rational valuation.

Because the core of the business remains robust, the conclusion is that LMT stock should be able to swing higher. With the recent ramping up of tensions in Iran, this assumption appears even more plausible.

Ultimately, this popular bullish argument centers on a practically universal presupposition. In order for a stock to continue on its present trajectory, more confirming news is needed — and typically, the news needs to be of great substance to maintain the inertia. However, the other side of this presupposition is that a contrary news item could disproportionately offer a greater-than-expected impact.

In the case of LMT stock, there likely needs to be more bad news for the defense firm to continue falling. However, with so much pessimism baked in, a positive catalyst could reverse the bearish trend (because there’s much less resistance in the upward direction).

What I just proposed isn’t likely to generate controversy — this is basically market physics. The issue is whether it’s worth it to jump on LMT stock as a trade (or just acquire it for an extended buy-and-hold position).

This is where it gets a little tricky.

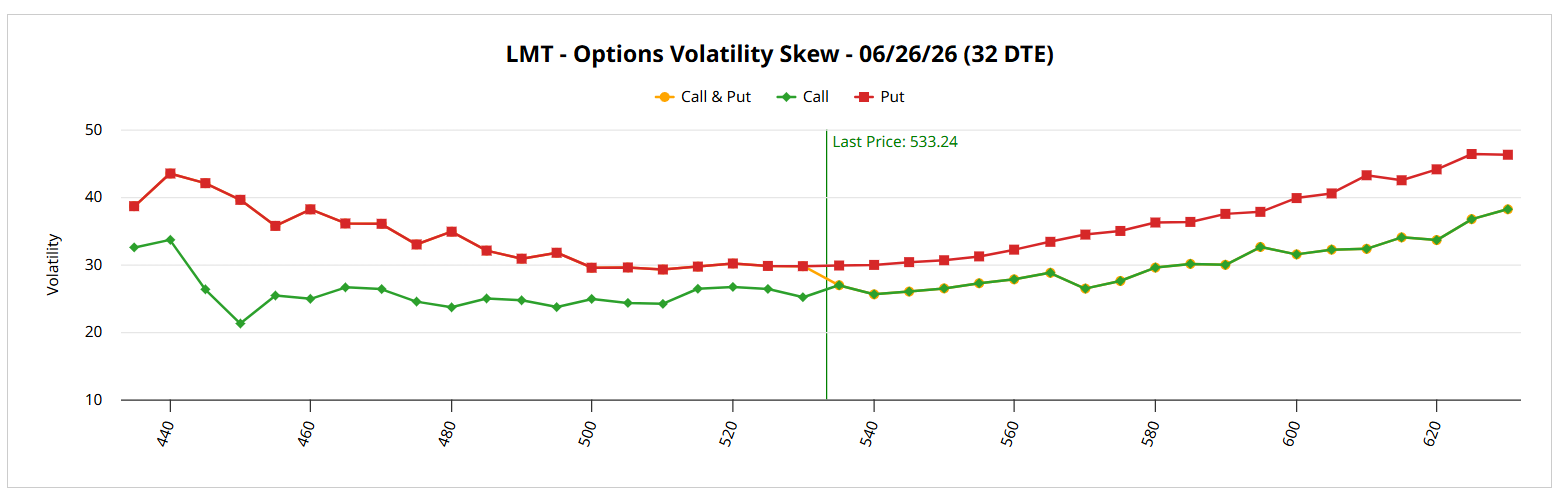

Volatility Skew Paints a Tough Picture for LMT Stock

Although Lockheed Martin stock offers fundamental relevance (for obvious reasons), the volatility skew provides a nuanced picture for options traders. By definition, the skew identifies implied volatility (IV) across the strike price spectrum of a given options chain. Since IV reflects the underlying pricing potential, traders effectively bid for coverage of the underlying movement.

Think of the skew as an insurance market. On any given day for a popular security, traders must determine the probability of it going up or going down. To hedge against either risk, these sophisticated market participants must buy insurance so they’re not caught out — whether that means the stock collapses or rips higher.

Usually, traders prefer put dominance on the left-side tail, thereby protecting against downside exposure, while paying for call dominance on the right side, thus levering up any rallies. This transactional dynamic creates a “smile” in the skew. However, the difference for LMT stock is that there’s really no upside convexity; that is, put dominance is the order of the day on both tails for the June 26 expiration date.

Effectively, traders are worried about a continued decline in LMT stock and are willing to pay a premium for risk mitigation. On the other end, they do acknowledge that upside is possible. Therefore, they refuse to pay a premium for a moonshot that likely might not happen.

Looking at the empirical data, it’s difficult to disagree with the smart money on this point.

Triangulating Where Lockheed Martin Stock May End Up

Using a dataset going back to January 2019, a random 10-week long position is likely to end up with an exceedance ratio of 48.1%, which isn’t great. Overall, the forward distribution would be projected to land between $528 and $540 (assuming a starting price of $533.24).

However, in the last 10 weeks, Lockheed Martin stock printed only three up weeks, leading to a downward slope across the period. Under this specific condition, the forward 10-week distribution tends to shift positively, with median outcomes ranging between $528 and $547. Further, by the fifth week (which coincides with the June 26 expiration date), median prices have been observed to cluster around $540.

If we accept the presupposition of this triangulated approach, there is a slight observational advantage in buying LMT stock under this condition as opposed to buying shares randomly. However, the payout for the corresponding spread isn’t all that great.

Based on both the volatility skew and the inductive model above, the 530/540 bull call spread expiring June 26 arguably makes the most sense. But this spread only provides a capped payout for 38.89%, with a current cost of $720.

It’s my opinion that LMT stock options are efficiently priced, which doesn’t leave much room for traders to exploit. At this rate, I’d be more inclined to consider a long-term buy-and-hold strategy rather than a quick scalp.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Institutional Investors Love Ford Stock - Buying Huge, Unusual Volume of Long-Term Call Options

- How to Trade Lockheed Martin Stock Now Amid Escalating U.S.-Iran Tensions

- Micron Stock Is Up 726%. This Options Strategy Pays You to Buy the Dip

- Lowe's Delivers Strong Free Cash Flow, But the Stock Fell - Time to Buy LOW?