MasTec’s 29.7% return over the past six months has outpaced the S&P 500 by 16.7%, and its stock price has climbed to $143 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in MasTec, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.Despite the momentum, we don't have much confidence in MasTec. Here are three reasons why MTZ doesn't excite us and a stock we'd rather own.

Why Is MasTec Not Exciting?

Involved in the 1996 Olympic Games MasTec (NYSE: MTZ) is an infrastructure construction company that specializes in the telecommunications, energy, and utility industries.

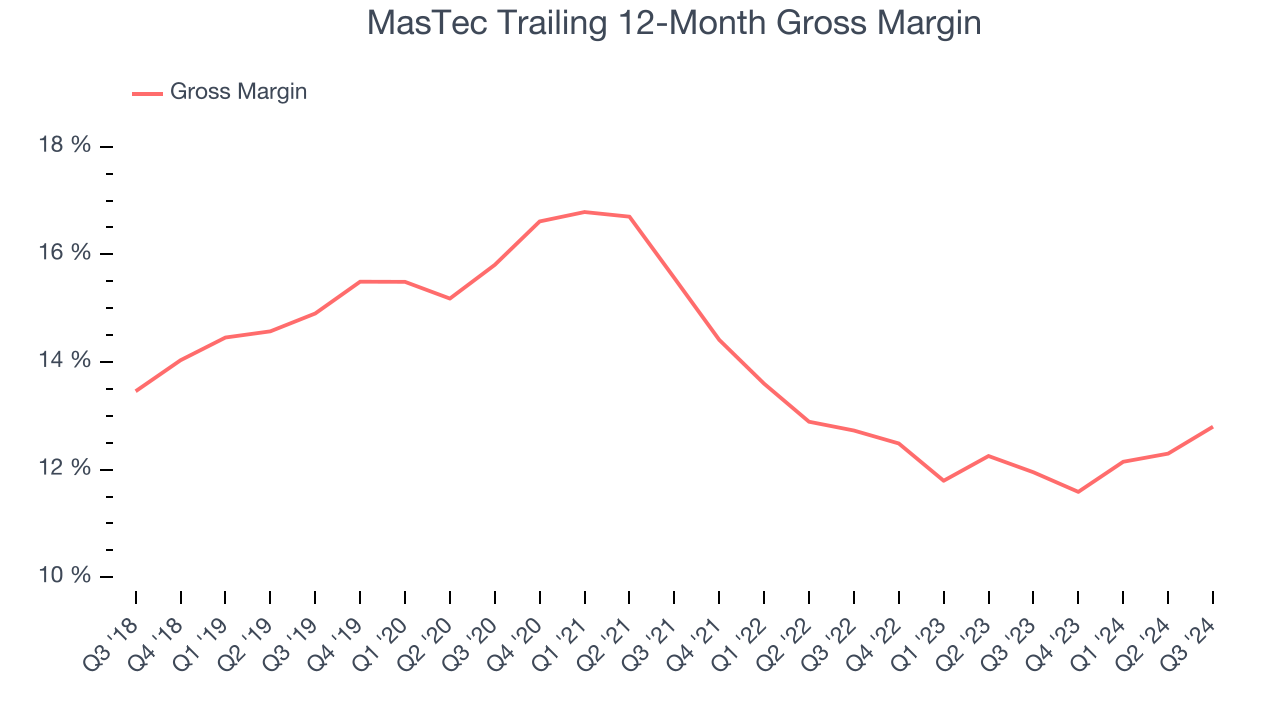

1. Low Gross Margin Reveals Weak Structural Profitability

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

MasTec has poor unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 13.4% gross margin over the last five years. Said differently, MasTec had to pay a chunky $86.55 to its suppliers for every $100 in revenue.

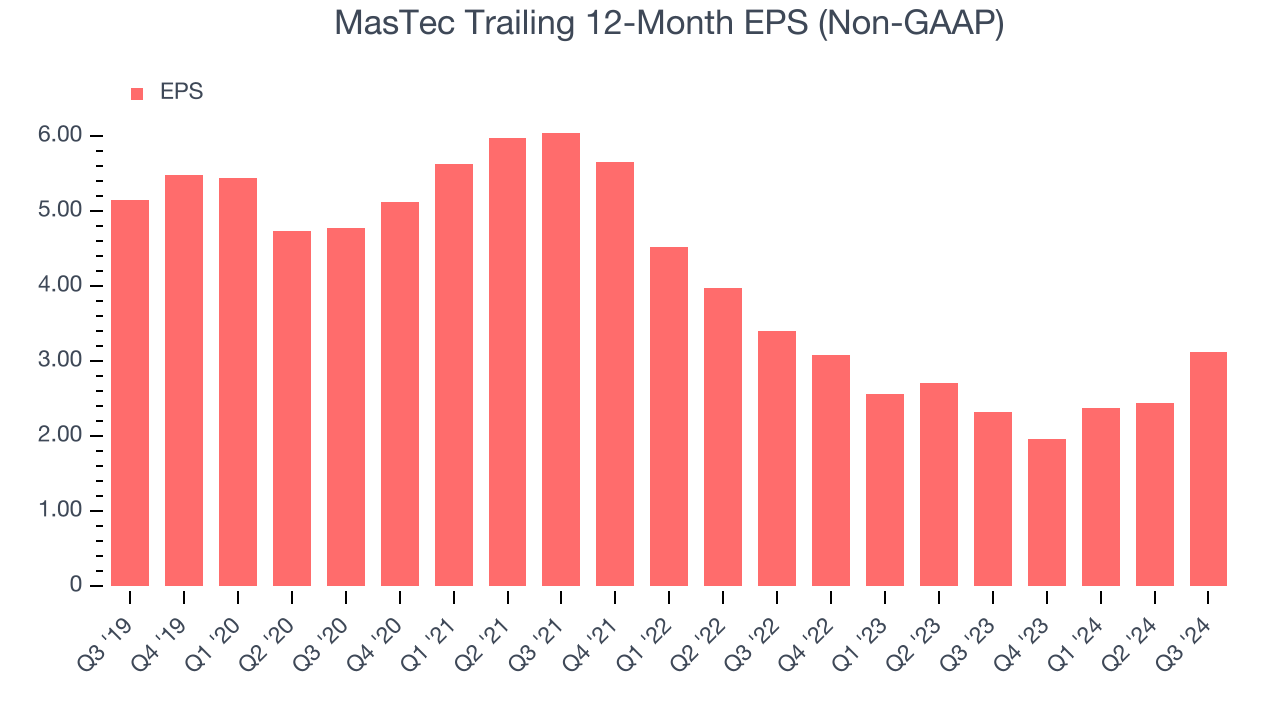

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for MasTec, its EPS declined by 9.5% annually over the last five years while its revenue grew by 10.5%. This tells us the company became less profitable on a per-share basis as it expanded.

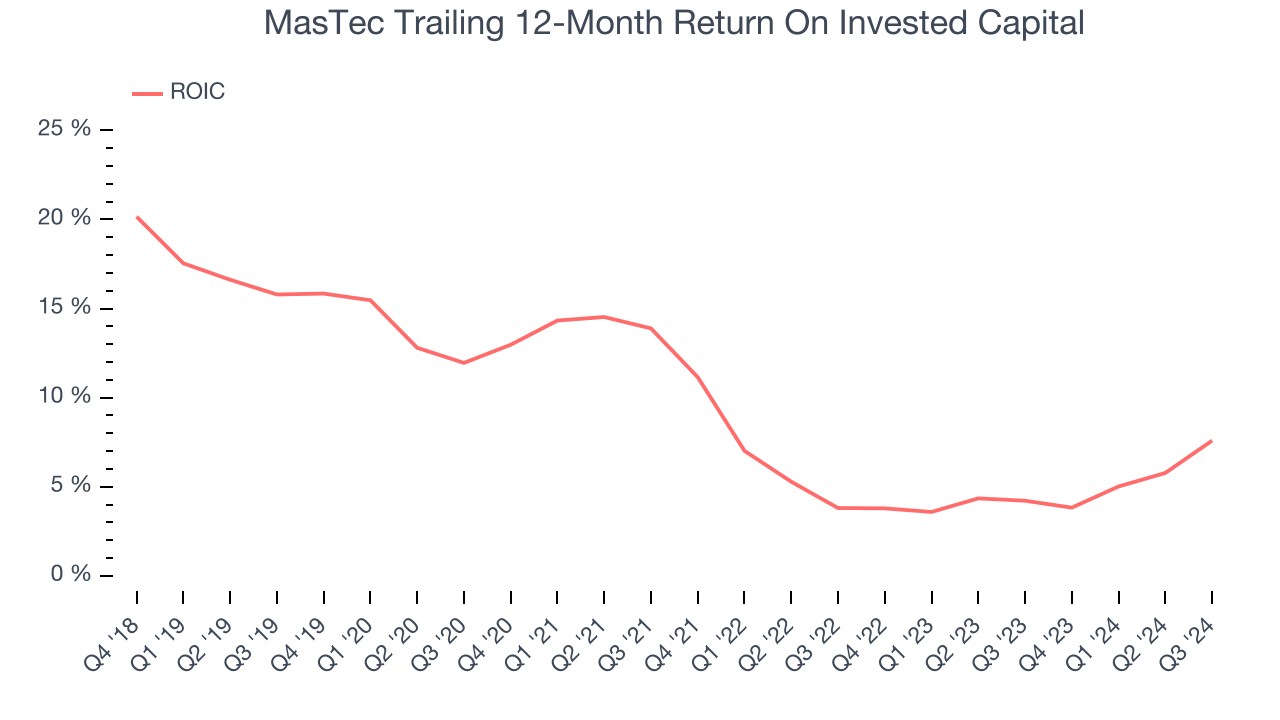

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Over the last few years, MasTec’s ROIC has decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

MasTec isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 36.6x forward price-to-earnings (or $143 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find better investment opportunities elsewhere. We’d suggest looking at Chipotle, which surprisingly still has a long runway for growth.

Stocks We Like More Than MasTec

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.