Regional banking company Commerce Bancshares (NASDAQ: CBSH) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 6.7% year on year to $445.8 million. Its GAAP profit of $1.14 per share was 10.1% above analysts’ consensus estimates.

Is now the time to buy Commerce Bancshares? Find out by accessing our full research report, it’s free.

Commerce Bancshares (CBSH) Q2 CY2025 Highlights:

- Net Interest Income: $280.1 million vs analyst estimates of $276.7 million (6.8% year-on-year growth, 1.2% beat)

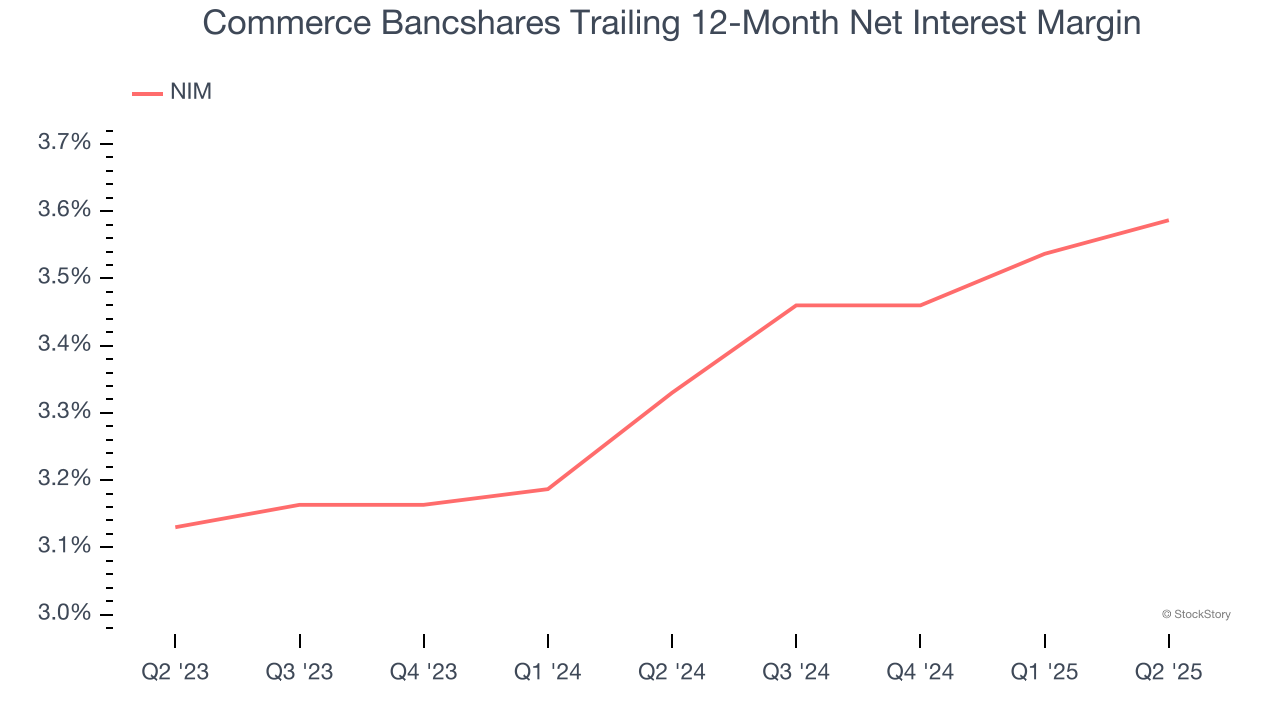

- Net Interest Margin: 3.7% vs analyst estimates of 3.6% (15 basis point year-on-year increase, 12.4 bps beat)

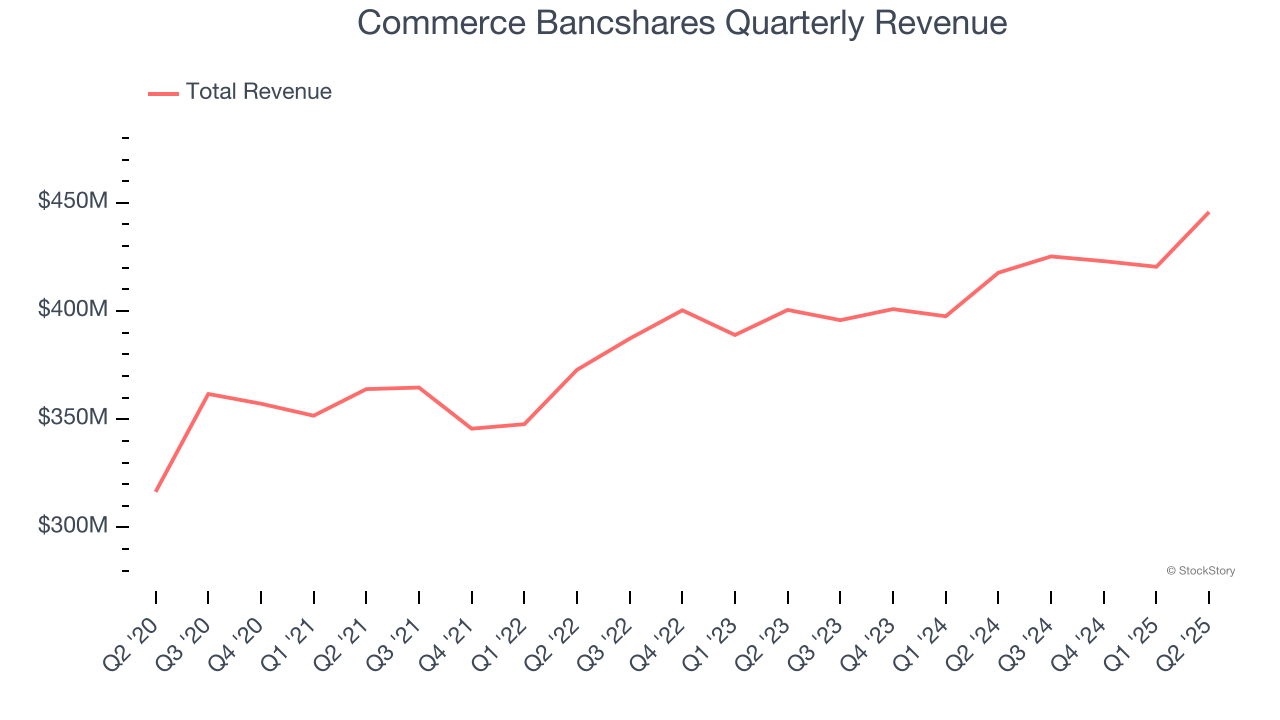

- Revenue: $445.8 million vs analyst estimates of $434.2 million (6.7% year-on-year growth, 2.7% beat)

- Efficiency Ratio: 54.8% vs analyst estimates of 55.5% (0.8 percentage point beat)

- EPS (GAAP): $1.14 vs analyst estimates of $1.04 (10.1% beat)

- Market Capitalization: $8.45 billion

In making this announcement, John Kemper, Chief Executive Officer, said, “Commerce delivered a strong financial performance in the second quarter, one that reflected our diversified operating model and the talented team behind it. Our financial results were supported by loan growth, strong fee income, low credit costs and continued disciplined expense management, all key ingredients in our steady profit growth over time.”

Company Overview

Founded in 1865 during the post-Civil War economic boom, Commerce Bancshares (NASDAQGS:CBSH) is a Midwest-focused bank holding company that provides retail, commercial, and wealth management services to individuals and businesses.

Sales Growth

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities.

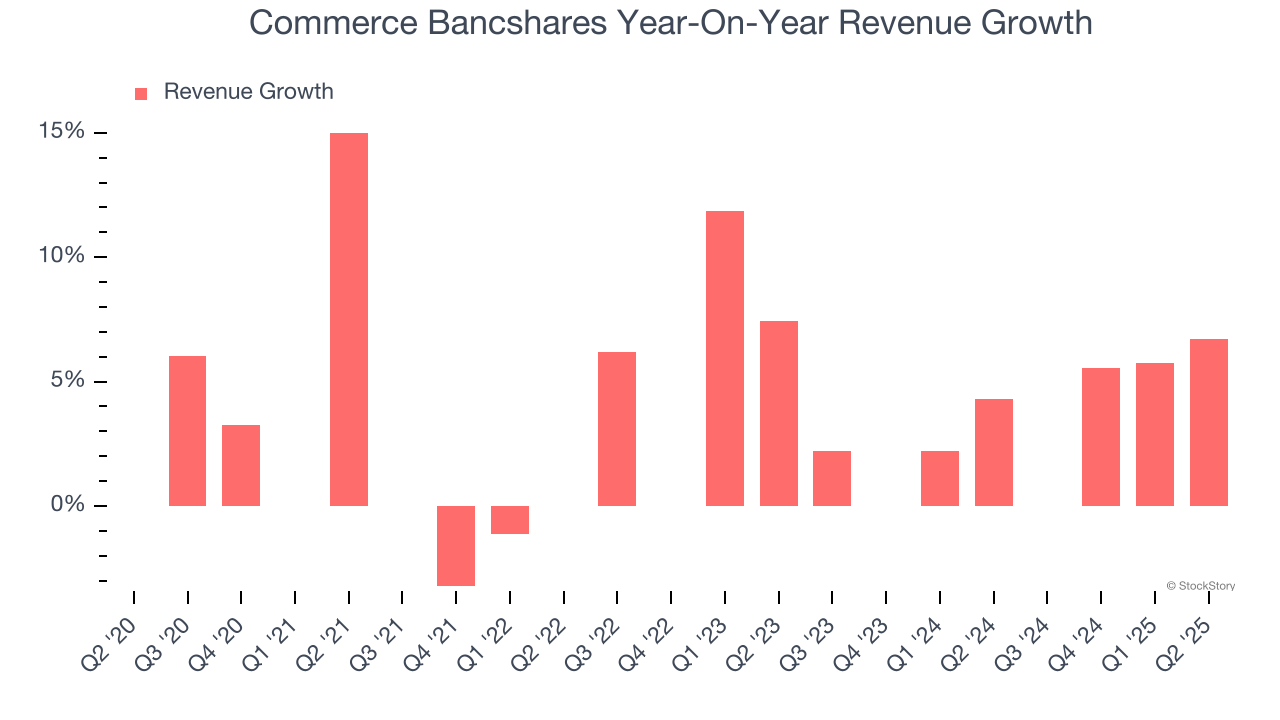

Over the last five years, Commerce Bancshares grew its revenue at a decent 5.5% compounded annual growth rate. Its growth was slightly above the average bank company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Commerce Bancshares’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Commerce Bancshares reported year-on-year revenue growth of 6.7%, and its $445.8 million of revenue exceeded Wall Street’s estimates by 2.7%.

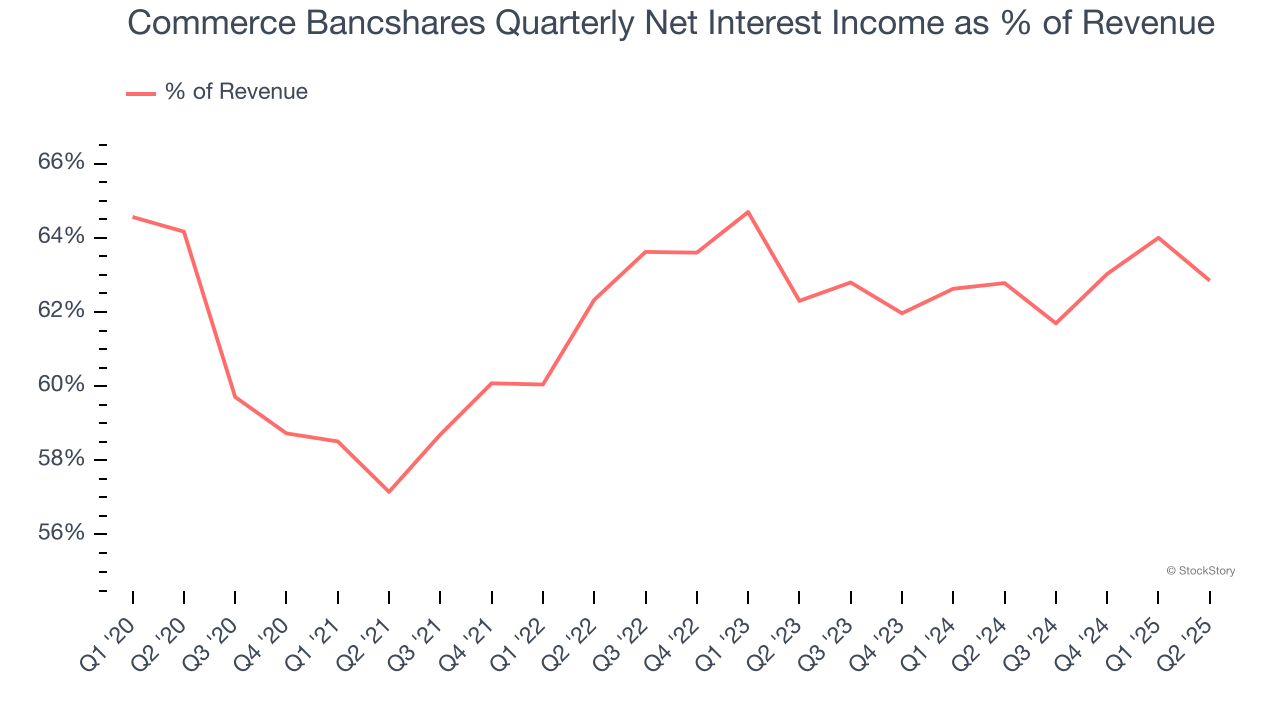

Net interest income made up 61.6% of the company’s total revenue during the last five years, meaning lending operations are Commerce Bancshares’s largest source of revenue.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Net Interest Income

Commerce Bancshares’s net interest income has grown at a 6.3% annualized rate over the last five years, slightly worse than the broader bank industry and in line with its total revenue.

When analyzing Commerce Bancshares’s net interest income over the last two years, we can see that growth decelerated to 3.7% annually.

From a unit economics perspective, we can see the company’s net interest margin averaged a subpar 3.5% over the past two years. On the bright side, it climbed by 45.7 basis points (100 basis points = 1 percentage point) over that period.

This expansion was a tailwind for its net interest income, and while prevailing interest rates matter the most for industry net interest margins, banks that consistently increase this figure generally boast higher-earning loan books (all else equal such as the risk of those loans) or provide differentiated services that give them the ability to charge higher rates (pricing power).

Commerce Bancshares’s net interest income came in at $280.1 million this quarter, up 6.8% year on year and topping Wall Street Consensus estimates by 1.2%. Net interest margin was 3.7%, beating sell-side expectations by 3.5%.

Looking ahead, sell-side analysts expect net interest income to grow 7.7% over the next 12 months, an improvement versus the last two years.

Key Takeaways from Commerce Bancshares’s Q2 Results

We enjoyed seeing Commerce Bancshares beat analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $63.30 immediately after reporting.

Big picture, is Commerce Bancshares a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.