NBT Bancorp trades at $44.09 and has moved in lockstep with the market. Its shares have returned 10.8% over the last six months while the S&P 500 has gained 13.3%.

Is now the time to buy NBT Bancorp, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is NBT Bancorp Not Exciting?

We're cautious about NBT Bancorp. Here are three reasons why NBTB doesn't excite us and a stock we'd rather own.

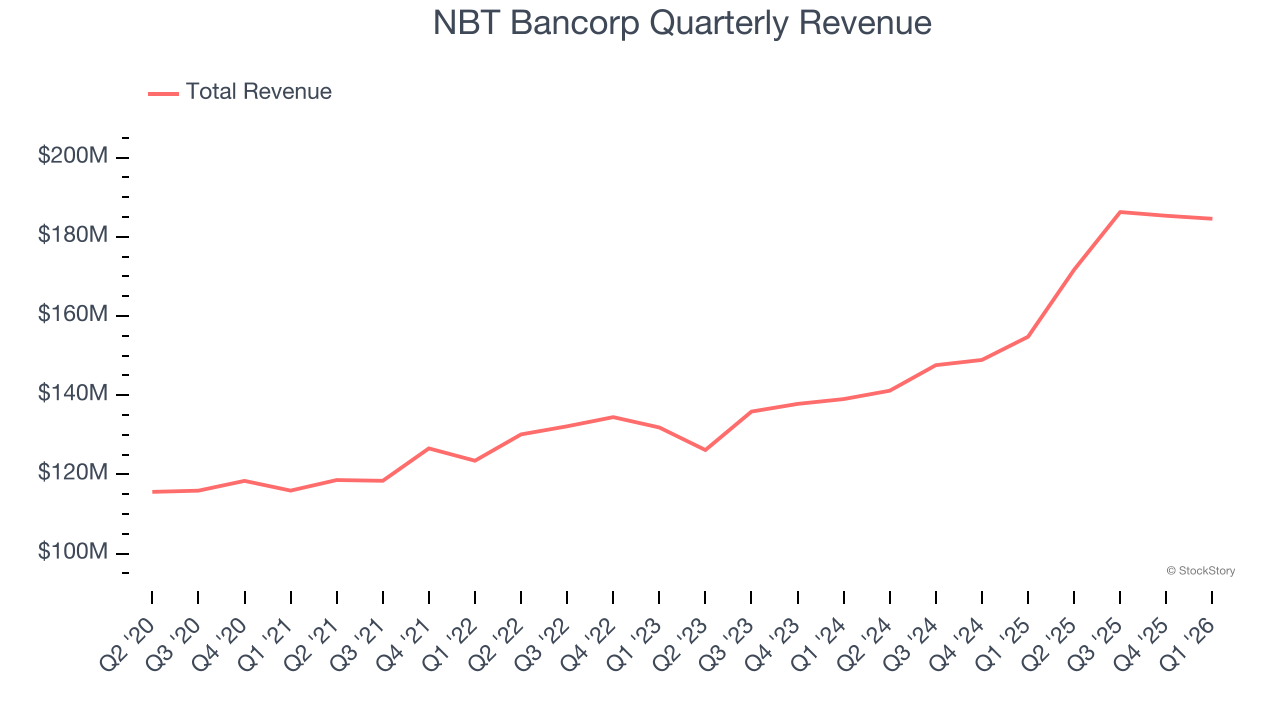

1. Long-Term Revenue Growth Disappoints

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities.

Regrettably, NBT Bancorp’s revenue grew at a mediocre 9.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector.

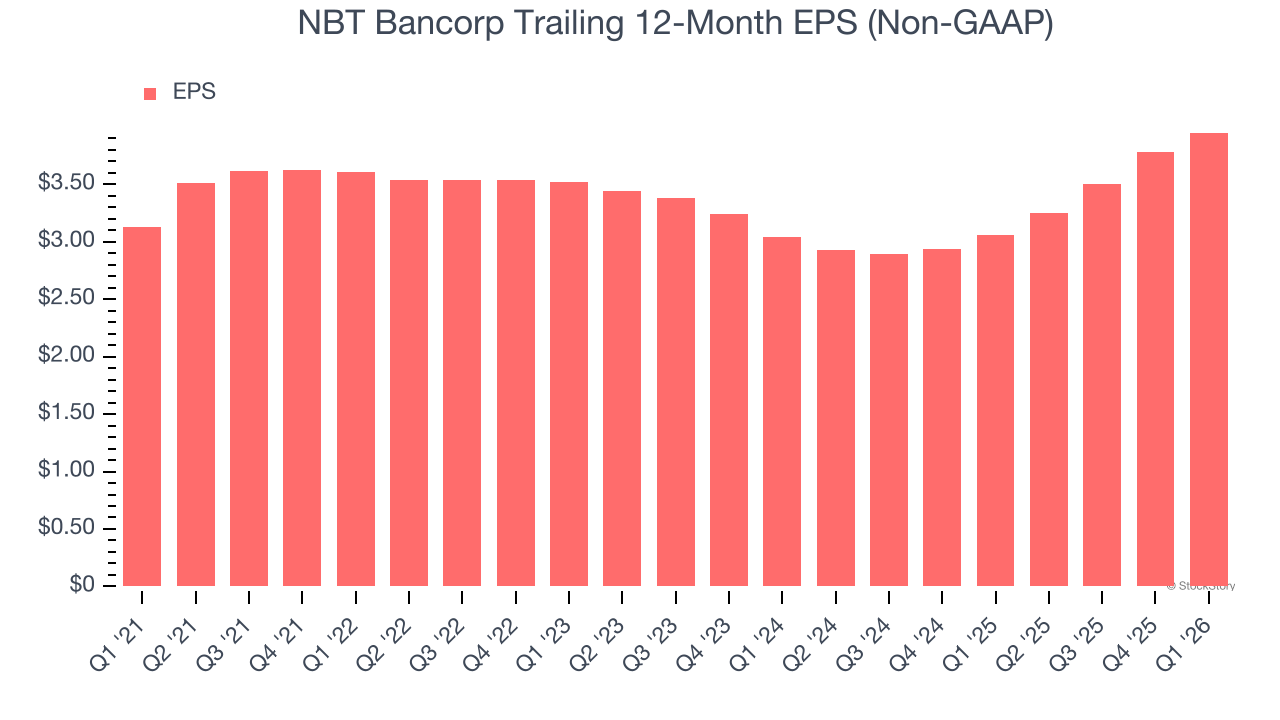

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

NBT Bancorp’s EPS grew at a weak 4.8% compounded annual growth rate over the last five years, lower than its 9.3% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

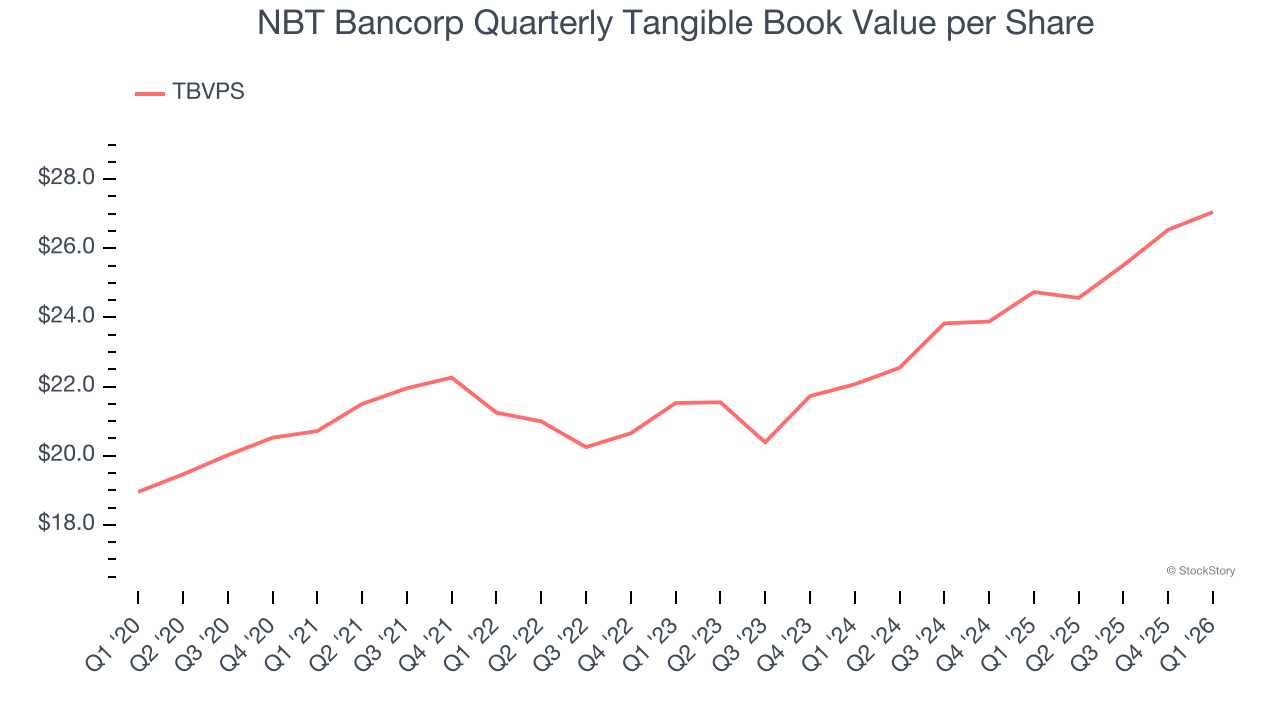

3. Projected TBVPS Growth Is Slim

Tangible book value per share (TBVPS) growth is driven by a bank’s ability to earn more than its cost of capital through lending activities while maintaining a strong balance sheet.

Over the next 12 months, Consensus estimates call for NBT Bancorp’s TBVPS to grow by 11.1% to $30.06, mediocre growth rate.

Final Judgment

NBT Bancorp isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 1.1× forward P/B (or $44.09 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.