As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q1. Today, we are looking at sales software stocks, starting with HubSpot (NYSE: HUBS).

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

The 4 sales software stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 1.5% while next quarter’s revenue guidance was 0.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 15.3% since the latest earnings results.

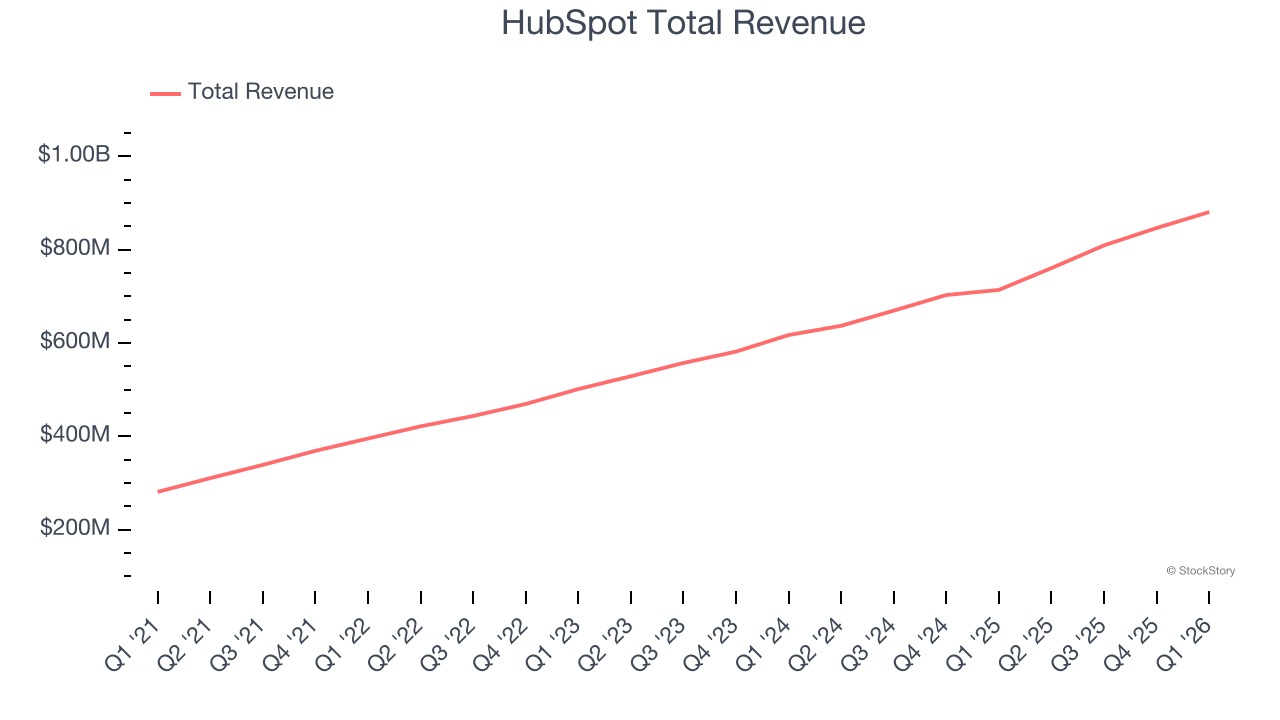

Best Q1: HubSpot (NYSE: HUBS)

Born from the idea that traditional interruptive marketing was becoming less effective, HubSpot (NYSE: HUBS) provides an integrated platform that helps businesses attract, engage, and manage customer relationships through marketing, sales, service, and content management tools.

HubSpot reported revenues of $881 million, up 23.4% year on year. This print exceeded analysts’ expectations by 2.1%. Overall, it was a strong quarter for the company with EPS guidance for next quarter exceeding analysts’ expectations and full-year EPS guidance exceeding analysts’ expectations.

HubSpot pulled off the fastest revenue growth of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 15.7% since reporting and currently trades at $205.50.

We think HubSpot is a good business, but is it a buy today? Read our full report here, it’s free.

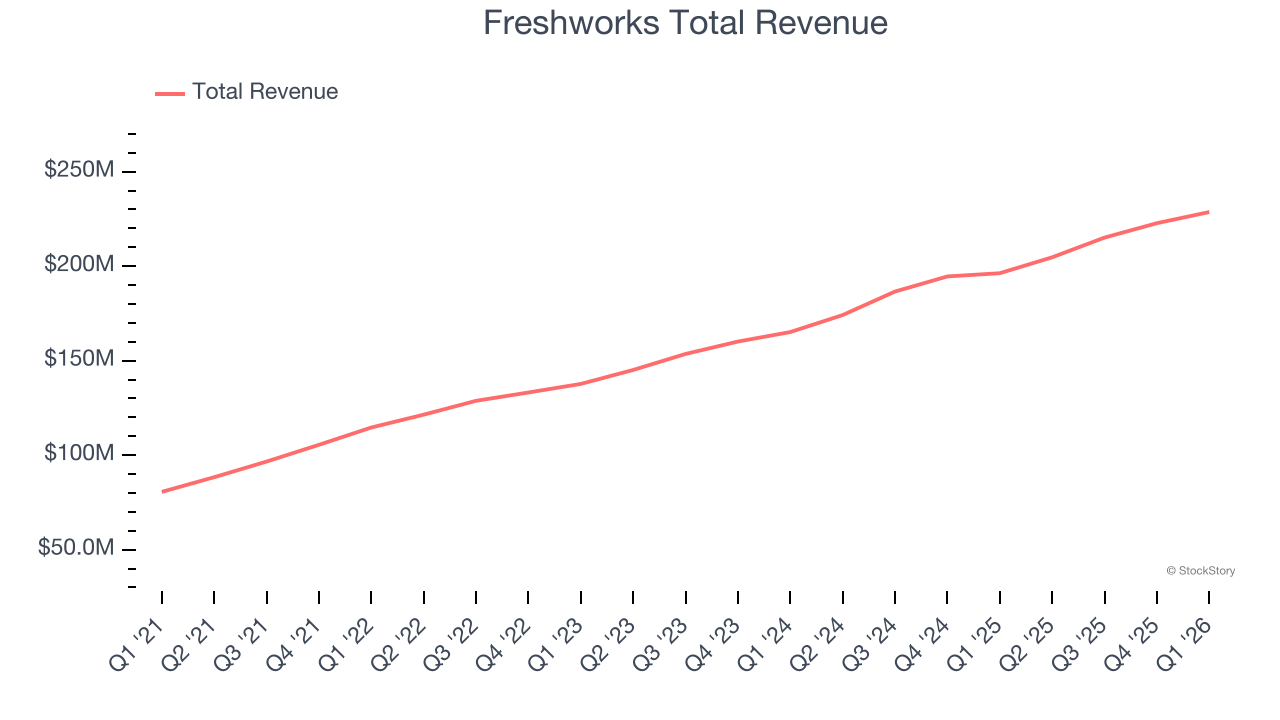

Freshworks (NASDAQ: FRSH)

Starting as a customer service solution before expanding into a comprehensive software suite, Freshworks (NASDAQ: FRSH) provides AI-powered software-as-a-service solutions that help companies manage customer service, IT support, sales, and marketing functions.

Freshworks reported revenues of $228.6 million, up 16.5% year on year, outperforming analysts’ expectations by 2.3%. The business had a strong quarter with full-year EPS guidance exceeding analysts’ expectations and a solid beat of analysts’ billings estimates.

Freshworks delivered the biggest analyst estimate beat, highest guidance raise, and highest full-year guidance raise among its peers. The company added 326 enterprise customers paying more than $5,000 annually to reach a total of 25,088. The market seems happy with the results as the stock is up 14.3% since reporting. It currently trades at $10.50.

Is now the time to buy Freshworks? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: ZoomInfo (NASDAQ: GTM)

Operating a platform it calls "RevOS" - short for Revenue Operating System - ZoomInfo (NASDAQ: GTM) provides sales, marketing, and recruiting teams with business intelligence and analytics to identify prospects and deliver targeted outreach.

ZoomInfo reported revenues of $310.2 million, up 1.5% year on year, exceeding analysts’ expectations by 0.7%. Still, it was a slower quarter as it posted revenue guidance for next quarter missing analysts’ expectations significantly and billings in line with analysts’ estimates.

ZoomInfo delivered the As expected, the stock is down 51% since the results and currently trades at $2.96.

Read our full analysis of ZoomInfo’s results here.

Salesforce (NYSE: CRM)

With its cloud-based platform named after its stock ticker symbol CRM (Customer Relationship Management), Salesforce (NYSE: CRM) provides customer relationship management software that helps businesses connect with their customers across sales, service, marketing, and commerce.

Salesforce reported revenues of $11.13 billion, up 13.3% year on year. This number surpassed analysts’ expectations by 0.8%. More broadly, it was a slower quarter as it recorded a miss of analysts’ billings estimates and full-year revenue guidance meeting analysts’ expectations.

The stock is down 8.8% since reporting and currently trades at $161.98.

Read our full, actionable report on Salesforce here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.