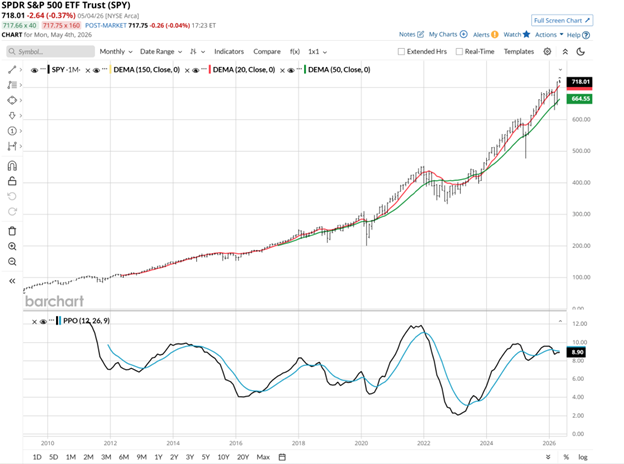

Here’s a look at the SPDR S&P 500 ETF (SPY) since the end of March 2009. That was the end of the global financial crisis.

I mean hey, what’s not to like about this chart?

Now, listen. It's OK to like the stock market – or even love it. Just don’t trust it unconditionally.

Why?

I’m not here to tell anyone not to be an optimist, or to take any particular action as an investor. That was my old job for 27 years as an advisor, and previously as the lead manager of a mutual fund. But it’s exactly that experience, from 1986 through today, that convinces me of this: it just isn’t that easy. The stock market is a cyclical animal. And we’ve seen essentially one cycle for nearly 20 years.

Sure, the S&P 500 took cat naps every so often – five weeks during 2020; nine months during 2022; a couple of weeks here and there last year; and a 9% dip here in 2026 that was bought like all the rest.

However, in the world of market analysis, there are milestones that act as flashing yellow lights. We just hit one. The tech sector is drunk on AI capex. We see and feel it in the headlines every day. We can choose to play that multiple ways. But to me, the answer is both ways.

The Best Defense

I don’t think any investor should commit to the “I’ll just hang in there, it always comes back” or “time in the market, not timing the market.” Those are just a couple of many Wall Street sayings that essentially translate to “keep buying.”

The music can’t keep playing forever. At some point, there will be a years-long cost to the global economy for what seems like two decades’ worth of coordinated action by global central banks in the form of keeping interest rates low – and in the case of the United States, doing so in a way that allows for massive liquidity-driven stock market rallies to occur.

Do I know this for a fact? Of course not.

But am I nevertheless prepared for what we might refer to as “the great realization” that could – either gradually or abruptly – sweep a generation of investors into their first real bear market, and Wall Street’s first since 2008?

Well, here’s a hint: I live by the motto, “play offense and defense at the same time.”

And you can, too, regardless of how close you are to traditional retirement age. In fact, if you’re in your peak earnings years, why let the stock market be the primary, passive custodian of that hard-earned money?

If you’re more like my Boomer peers (yes, I left out the “OK” before Boomer), recent data from Fidelity and Vanguard implies that we have more than half of our liquid portfolio assets in stocks and stock funds. Generation X is more like two-thirds. And millennials are closer to 80% in stocks.

This heavy focus on equities might work out for everyone. And everyone seems pretty well convinced it will work out.

But, you know, just in case – what else is out there, for an investor looking to play defense?

Why It’s Time to Think Outside of Stocks

It’s easy to forget, but there’s still an entire universe of investments outside the narrowly focused stock market mindset of FOMO, BTFD, and QQQ.

Why include QQQ? It has become the symbol for the modern, AI-driven, one-way, narrowly-minded stock trade. So much so that even though the S&P 500 index is the asset hog in the indexed ETF world, QQQ is the exciting one – free of those tiny sectors that “have” to be there, but don’t amount to much. As a result, QQQ and SPY correlate more than ever.

By extension, if the “stock market” is really just one big AI trade, why hyperfocus and hyperventilate about that market solely? Instead, why not hedge the risks of a stock market driven by indexation and algorithmic trading… by laddering bonds.

So while rates continue to rise, fill out a bond ladder. I’ve been doing that for more than a year, and I’ve left some room for a yield spike, if there is one. And I hedge that bond portfolio like my financial life depends on it. Because it does.

But there will come a point at which bond rates stop rising. And that’s when I think investors might want to have gone to school on bond investing, in its many forms. I’ll touch on a few of those here. Because every day, the bond market intrigues me more than the stock market does.

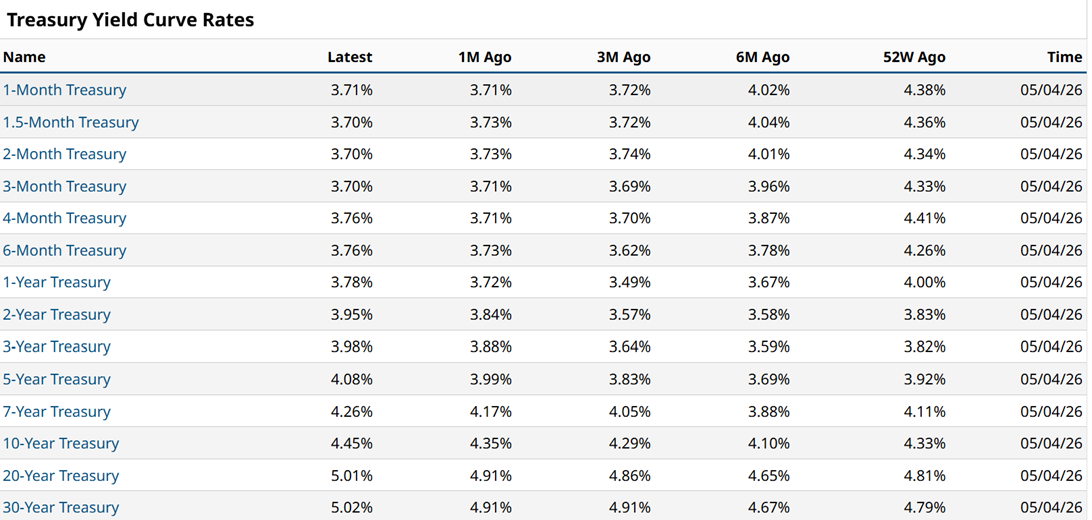

I’ve used Barchart for a very long time, but only started writing here about a year ago. During that time, of course I have my familiar “old comfortable shoes” sections of the site, which I highlight in nearly every article here. Those are the technical charts, ETF top holdings, and similar analytics. And then, yes, more charts. Hey, I’m a technician!

But this one right here below is quickly moving up my list of favorites. Not because it is data I can’t get anywhere else; I can. But because it is just so darn well done!

I consider this to be a “spot the opportunity” table, showing where rates are across maturities from 1-month Treasuries to 30-year Treasuries.

If and when the folks in DC get their wish to have America borrow money for 100 years, or at least 50, I’ll alert our data folks and see that it is added. Because in 2136, I want my great-great-great-grandkids to cash in on my “long-term investment.”

Getting back to rates and maturities we can enjoy while we’re still around, if rates in my favorite range (5-20 years to maturity) hang in this area longer-term, it is simply the best “equity crash prevention” mechanism an investor can have – if you buy the bonds and hold to maturity.

Addressing the Bond Knowledge Gap

Buying bonds and planning to hold them isn’t something many investors are familiar with. Why would they be, when zero rates were the policy for so long?

If you’re 35 years old, you were in high school the last time bond income rates mattered this much. And if you’re 70 years old, you were probably too busy working your butt off to save for retirement, and didn’t notice rates in the mid-single digits during the first decade of this century.

Expecting you to “get” immediately what I see in allegedly boring US Treasury bonds is akin to telling my adult children that they should have learned more about how to use a rotary phone. Unlike those relics of the past, bond investing is making a comeback. (Although since vinyl records did too, I guess you never know…? That’s the old 1980s college DJ talking – SUNY Albany, Class of 1986, where my Great Danes at?!)

So, it’s perfectly understandable that investors don’t know much about bond investing. What I wonder is, why isn’t someone alerting them to the generational opportunity?

The 5-year US Treasury note is what really caught my attention. Because at 4%+, and only going out 5 years, this is not one of those “bonds that acts like an income stock” kind of thing.

And that’s a fair criticism of longer-term bonds at times, since their prices gyrate more. That happens for the simple reason that, while US Treasury Bonds are expected to be “money good” at maturity, that maturity might be 2-3 decades from now. As a result, they’re way more volatile.

Not so with the 5-year. By the time our next US President is just past the midpoint of their term, these bonds will mature. Now, 4% doesn’t sound like it will blow the doors off. But there have been many times in history where the stock market didn’t sniff that kind of annualized return for many years.

When do those periods occur? Typically… after periods like the one we’ve just had. And most often, it’s when investors cannot fathom that it would actually happen again. Just saying.

Next up is the bond benchmark that’s likely most familiar to investors, because a lot of consumer debt is tied to its rate – like your mortgage, for instance. The 10-year US Treasury rate is near the top of its 20-year range. And while I can see it challenging that 4.8% recent high-water mark from early last year, as noted above, that can be hedged.

Plus, if you’re buying bonds outright, not ETFs, you still can figure you’ll get $1,000 back at maturity for every bond you bought. That’s because bonds are denominated in $1,000 lots, so to speak. And, unlike a stock or ETF, bonds are a contract.

Maybe some people these days are more willing to make a “pact” with the US Treasury. But the point I’m making is that bond returns for actual bonds owned are known the date you buy them. That’s why it is YTM (Yield To Maturity).

Stocks, even those with high dividend yields, are more like “Yield until I hope so.” There’s no maturity date, and no date where you’re certain to get repaid.

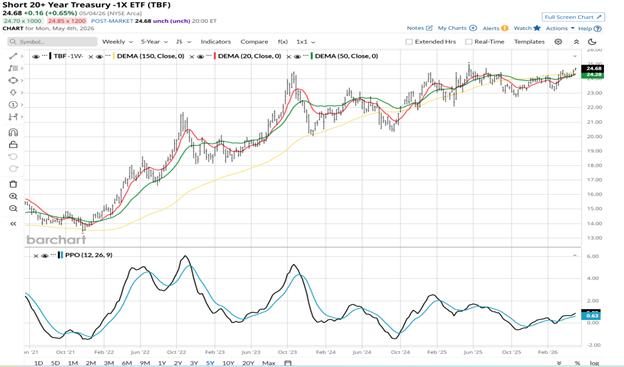

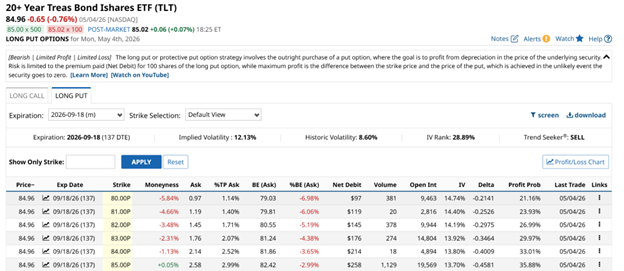

And while investors in bonds might be disappointed if their bond portfolio goes from 100 cents on the dollar to, say 90 cents or less if rates rise sharply, there are ETFs like the ProShares Short 20 Plus Year Treasury (TBF) that can be used to hedge that.

Or, as I do almost constantly, you can buy put options on TLT, and size your position to match the portion of your bond account value you wish to hedge.

Rob Can Hedge That: The Inverse ETF Play

Locking in yields is the defensive side of the ball. But what if you’re convinced that inflation or fiscal worries will push that 10-year yield past its 4.8% peak? That is where tactical tools come in.

Many investors mistakenly buy long bond ETFs like TLT for safety, only to watch the price crater as rates rise. Instead, the way to hedge like a true portfolio manager is by using inverse ETFs to profit as yields climb and bond prices fall.

Examples include:

- ProShares Short 20+ Year Treasury (TBF): This is the -1x play. It is designed to move in the opposite direction of long-term Treasuries. If the 20-year yield drifts higher, TBF gains value. I’ve used it tactically, on and off, for many years.

- ProShares UltraShort 20+ Year Treasury (TBT): For those looking for more kick, this is the -2x version. It’s a trading tool to hedge your long-term ladder against a sudden spike in rates.

- Direxion Daily 20+ Year Treasury Bear 3X ETF (TMV): You can’t “10x it” in ETF-land (at least, not yet). But when I’m looking to hedge a bond portfolio and options are too rich or otherwise not my first choice, a little position in this ETF is the closest surrogate I know. It could lose a ton of value in a short time frame, so I do think of this level of leverage more like a put option.

Here’s TBF, which is the simplest of that rate/inflation hedge trio, displayed on a weekly chart – my favorite time frame to avoid noise in the price data.

You might be pleasantly surprised that these inverse ETFs actually pay some yield, not too far off what the bonds themselves pay.

To recap: you earn a yield on the bonds, and you earn a yield hedging the bonds. That’s just scratching the surface, and it is another symptom of my lament here: that investors are undereducated about the bond side of the ledger – and in some ways miseducated, as well, to the extent that many consider TLT “bond investing.”

These ETFs are trading tools around an otherwise very long-term investment in the core bond ladder. In 2022, when rates rose sharply, any of the three ETFs above was either a great hedge, or a way for any investor to capitalize on rising rates.

When your friends are crying into their stock portfolio losses, this is a nice thing to know about. But it takes a little research to understand them, and some cojones to trade them.

How to Use Your Options

I just mentioned how I like to use TLT put options when rates are rising. When I see strong evidence that long-term rates are bound to fall, I shift the other direction, and look at owning TLT call options.

Using TLT options like this adds a “kicker” to existing price gains I’ll get on the bonds I own. If I hold until maturity, that is just trading around a virtual certainty.

To me, every part of my portfolio is about maximizing return every year, but with a clear priority: ABL, or Avoid Big Loss.

That’s why bond investing is now at the top of my portfolio food chain. Because with that setup, and money coming due each year predictably, I cannot emphasize enough how much that helps me sleep at night. (And perhaps as I get older, during the day too… but we’ll see about that.)

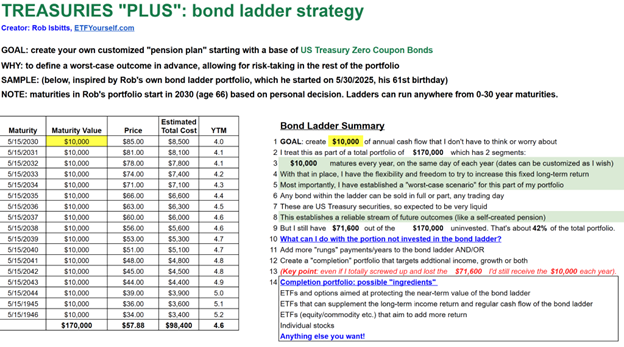

What My Bond Ladder Structure Looks Like

Candidly, this bond opportunity is very fluid right now. With concerns about information from the Strait of Hormuz/Iran War situation, an economy that just won’t quit, and a Fed Chair who also just won’t quit, we have a perfect storm for inflation-driven higher yields for a bit longer, and stagflation for a lot longer (cue the 1970s).

Regardless, this graphic is one I’ve used to teach my bond ladder technique to investor groups before. I use my own case as an example, but this is actually a sheet that allows the user to input (in yellow) the amount they want to have maturing each year. I used a generic $10,000 maturity value.

You can buy bonds in $1,000 increments, and if you are well-heeled, you can add zeroes or multiples to that $10,000 a year maturing.

And of course, there’s no reason you can’t allocate different amounts to different maturity years. Since bonds typically mature between a month and 30 years from now, the customization is ultimately up to the investor to craft.

This is just a tool I built, to help me and others to walk through the thought process, step by step. This is a very different frame of mind than, “buy so-and-so stock on today's earnings beat.”

So to summarize it for now, here are the 60-second takeaways from my approach to bond ladders.

The Bond Ladder: Key Features

The investor builds a ladder by purchasing bonds that mature in successive years (e.g., 2030 through 2046).

- Guaranteed Cash Flow: In this example, the investor secures $10,000 in annual payouts.

- Discounted Entry: Because these are zero-coupon bonds, they are bought at a discount (e.g., paying $8,500 now for a $10,000 payout in 2030).

- Safety: By using US Treasuries, the "worst-case scenario" for this portion of the portfolio is locked in and virtually risk-free if held to maturity. Because if Uncle Sam can’t pay us back, that’s the least of our world’s troubles.

The "Plus": The Completion Portfolio

My pet name for this strategy is Treasuries Plus. Here’s the plus: The efficiency of buying bonds at a discount leaves a significant portion of capital uninvested. In the sample provided, it costs roughly $98,400 to secure $170,000 in future payouts, leaving $71,600 (42%) of the original principal available.

Investors can use this "leftover" capital for a Completion Portfolio to:

- Add more "rungs" to the ladder for higher annual payouts.

- Invest in higher-growth assets like ETFs, stocks, or commodities.

- The Bottom Line: Even if the Completion Portfolio loses all its value, the investor’s base payout of $10,000/year remains secure.

That is where I sit back, relax and plot out the rest of my portfolio.

And if you’re wondering where some of the ideas for my regular daily articles at Barchart come from, I’ll tell you: I scour hundreds of charts each week, ETFs and stocks. I write about the ones that most interest me. It might be for actionable investment reasons soon. But it might also be trying to think steps ahead.

And speaking of steps, it should be clear by now: I think a lot of investors would benefit from better understanding what bond ladders do, and then determine to what extent they care to apply that knowledge to their own portfolio. Because the stock market got us this far. But historically, it can very quickly taketh away years of what it giveth.

Rob Isbitts created the ROAR Score based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Don’t Trust This Top-Heavy Stock Market, Hedge It. Here’s Your Roadmap.

- Unusual Shopify Stock Options Activity Signals a Unique Trade for Income and Upside

- HOOD Stock Bullish Diagonal Trade Targets a Price of $85 by June 18th

- Ahead of Airbnb Earnings, Here Is What Barchart Options Data Shows for ABNB Stock