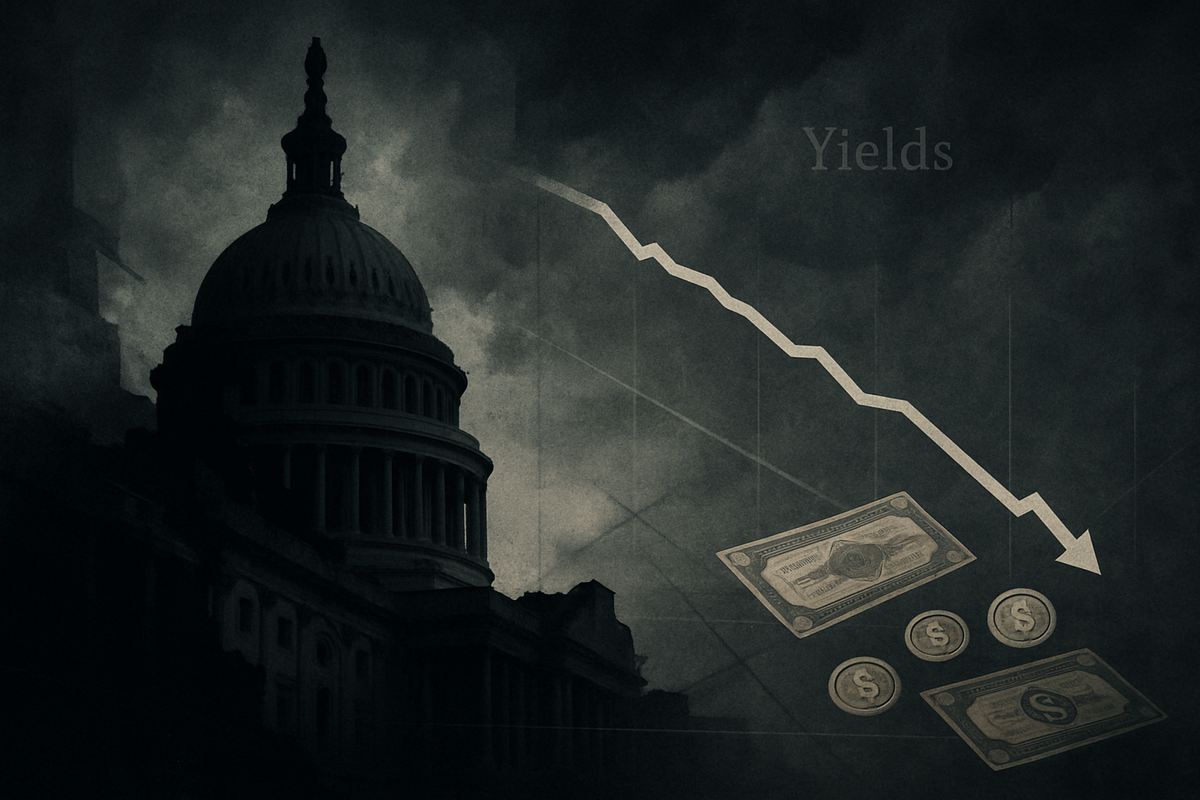

A potential U.S. government shutdown is once again casting a shadow over financial markets, triggering a predictable flight to safety that has sent Treasury yields lower. As the specter of halted government services and delayed economic data looms, investors are flocking to the perceived security of U.S. government bonds, pushing their prices up and yields down in a classic "Treasury rally." This defensive market posture reflects growing concerns about the immediate economic fallout and the broader implications for an already delicate global financial landscape.

The immediate implications extend beyond bond markets, threatening to slow an economy already grappling with inflationary pressures and interest rate hikes. While the Treasury Department continues to honor its debt obligations, ensuring bondholders are paid, the cessation of "non-essential" government functions is poised to disrupt various sectors, delay critical economic indicators, and potentially dampen consumer and business confidence. The unfolding situation highlights the inherent fragility of market sentiment in the face of political gridlock, prompting a re-evaluation of risk across asset classes.

Detailed Coverage: The Mechanics of Market Reaction to a Shutdown

The current market reaction is a direct consequence of the political impasse in Washington, where lawmakers are struggling to reach an agreement on appropriations bills to fund the government. As the deadline for funding approaches (or has passed, given the current date of 10/10/2025), the legislative brinkmanship has escalated, leading to the imminent or actual cessation of "non-essential" government operations. This includes a wide array of federal agencies and services, impacting everything from national parks to certain regulatory functions.

Historically, the timeline leading up to a government shutdown is marked by intense negotiations between the executive and legislative branches, often characterized by partisan disagreements over spending levels, policy riders, or debt ceiling issues. Key players include the President, the leadership of both the House of Representatives and the Senate, and various congressional committees responsible for appropriations. The current situation mirrors past standoffs, where the inability to pass continuing resolutions or full appropriations bills by the fiscal year-end (September 30th) triggers the shutdown mechanism.

Initial market reactions are typically swift and decisive. The most prominent is the aforementioned Treasury rally, where demand for U.S. Treasury bonds surges. This increased demand drives up bond prices and, conversely, pushes yields down. For example, during previous shutdowns, 10-year Treasury yields have historically fallen, with some analyses showing an average drop of 0.05% to 0.59% during such periods. This reflects investors' perception of Treasurys as the ultimate safe haven amidst domestic political uncertainty. Beyond bonds, equity markets often experience increased volatility and a general downturn as investors de-risk. Sectors heavily reliant on government contracts or regulatory approvals may see more pronounced negative impacts. Crucially, the U.S. Treasury Department continues to make all coupon payments and conducts debt auctions, ensuring the government's creditworthiness remains intact for bondholders, which reinforces the safe-haven appeal of Treasurys.

Another significant immediate impact is the delay or suspension of crucial economic data releases from agencies like the Bureau of Labor Statistics and the Census Bureau. Key reports such as the jobs report, Consumer Price Index (CPI), and GDP figures become unavailable, creating a data vacuum that complicates economic analysis for investors, businesses, and even the Federal Reserve (FED) (US:FED) in its monetary policy decisions. This heightened uncertainty can further dampen market sentiment and lead to more cautious investment strategies.

Winners and Losers: Navigating the Shutdown's Market Crosscurrents

A government shutdown, coupled with a Treasury rally, creates a bifurcated market, producing distinct winners and losers across various sectors. The flight to safety that drives Treasury yields down often provides an unexpected boon for rate-sensitive industries, while direct exposure to federal spending or regulatory processes spells trouble for others.

On the winning side, Technology and Growth Stocks are often beneficiaries of a falling interest rate environment. Companies like Nvidia (NASDAQ: NVDA), Advanced Micro Devices (NASDAQ: AMD), and Dell Technologies (NYSE: DELL) thrive as lower borrowing costs reduce their expenses for research and development and expansion. Furthermore, reduced discount rates increase the present value of their future earnings, boosting valuations. Similarly, the Real Estate sector, encompassing homebuilders and Real Estate Investment Trusts (REITs), sees a direct positive impact. Lower Treasury yields typically translate to lower mortgage rates, making homeownership more affordable and stimulating demand for new homes, benefiting companies like D.R. Horton (NYSE: DHI) or Lennar (NYSE: LEN). REITs also become more attractive as their capital-intensive operations benefit from cheaper financing. Utilities, a capital-intensive sector, also gain from reduced borrowing costs for their infrastructure projects, and their stable dividend yields become more appealing to income-seeking investors in a low-rate environment. Consumer Discretionary companies such as Nike (NYSE: NKE), Disney (NYSE: DIS), and Netflix (NASDAQ: NFLX) can also see a boost as lower consumer borrowing costs potentially encourage large purchases financed through credit. Even Consumer Staples like Walmart (NYSE: WMT) and Procter & Gamble (NYSE: PG) tend to be resilient, offering stability and dividends during uncertain times. In a "flight to quality," Gold Miners such as Newmont Corporation (NYSE: NEM) often see their fortunes rise with increased demand for gold as a safe-haven asset. Large Defense Contractors like Lockheed Martin (NYSE: LMT) and Northrop Grumman (NYSE: NOC) often remain relatively insulated due to the essential nature of their long-term contracts and national security priorities, which frequently ensure continued funding.

Conversely, the direct and indirect consequences of a shutdown create significant losers. Federal Contractors are arguably the most vulnerable. Companies like Maximus Inc. (NYSE: MMS) and Science Applications International Corporation (NYSE: SAIC), which derive substantial revenue from government contracts, face immediate project halts, delayed payments, and an inability to secure new work. Unlike furloughed federal employees, contractors are not guaranteed back pay, leading to substantial financial strain. Even tech giants like Oracle (NYSE: ORCL), Microsoft (NASDAQ: MSFT), and Amazon Web Services (NASDAQ: AMZN), which have significant government cloud contracts, could experience disruptions, although their diversified revenue streams offer some buffer. Sectors requiring government approvals and licenses face severe delays; for instance, companies planning Initial Public Offerings (IPOs) or other significant financial filings with the Securities and Exchange Commission (SEC) (US:SEC) will find their processes stalled due to limited SEC staff. The Travel and Transportation industry, including airlines and airport service providers, suffers from potential staffing shortages among essential personnel like air traffic controllers and TSA agents, leading to flight delays and cancellations. A broader decline in Consumer Spending and Confidence, particularly in regions with a high concentration of federal workers, can impact a wide range of businesses. Finally, while a Treasury rally generally implies lower rates, the Financials sector can face headwinds. Lower rates can compress net interest margins for banks, and prolonged economic uncertainty can lead to reduced loan growth and increased credit risk, even if some larger institutions might benefit from stimulated capital markets.

Wider Significance: A Recurring Saga of Economic Headwinds and Safe Havens

The recurring spectacle of a U.S. government shutdown, accompanied by a Treasury rally, is not merely a fleeting political skirmish but a symptomatic event reflecting deeper economic vulnerabilities and policy impasses. It fits into broader industry trends by highlighting the interconnectedness of government function and economic stability, while exposing regulatory weaknesses and echoing a history of similar fiscal showdowns.

From a broader economic perspective, shutdowns consistently chip away at Gross Domestic Product (GDP) growth. Each week of a shutdown is estimated to reduce annualized GDP growth by approximately 0.1 to 0.2 percentage points. While some of this lost economic activity is often recouped post-reopening, a portion can be permanently lost, as evidenced by the 2018-2019 shutdown, which cost the U.S. economy an estimated $11 billion, with a permanent loss of $3 billion. This impact stems from furloughed federal workers reducing their spending and delays in government procurement. A critical ripple effect is the "data blackout," where essential economic reports—such as those on nonfarm payrolls, inflation, and GDP—are suspended. This absence of timely, reliable data complicates decision-making for investors, businesses, and critically, the Federal Reserve (US:FED) in its monetary policy decisions. The Treasury rally itself underscores a broader trend of risk aversion in times of political uncertainty, positioning U.S. Treasurys as the preeminent global safe haven, even amidst domestic fiscal dysfunction. This dynamic can also impact global supply chains, as regulatory delays in the U.S. can slow import/export documentation and create backlogs worldwide.

The regulatory and policy implications are extensive and disruptive. A shutdown means the suspension of numerous non-essential federal services, leading to delays in critical processes like passport applications, small business loans, and even food safety inspections. Regulatory agencies vital to various sectors, such as the Securities and Exchange Commission (SEC) (US:SEC), the Food and Drug Administration (FDA) (US:FDA), and the Environmental Protection Agency (EPA) (US:EPA), operate with minimal staff. This creates significant bottlenecks, stalling approvals for Initial Public Offerings (IPOs), drug trials, environmental permits, and mergers & acquisitions (M&A) reviews, directly impacting biotech, energy, and financial services. States and localities also feel the pinch through delayed federal transfers for programs like Medicaid and education, which can, in turn, affect municipal bond markets. The Internal Revenue Service (IRS) (US:IRS) curtails operations, potentially delaying tax refunds and audits, adding another layer of uncertainty for businesses and individuals.

Historically, government shutdowns are a relatively modern phenomenon, largely stemming from legal interpretations of the Antideficiency Act in the early 1980s. Since 1976, there have been at least 20 shutdowns lasting a day or more, with several notable instances. The 1995-1996 shutdown, lasting 21 days during the Clinton administration, involved disputes over spending cuts. The 2013 shutdown, a 16-day event over the Affordable Care Act (ACA), resulted in an estimated $24 billion loss and shaved 0.6% off annualized fourth-quarter GDP growth. The longest in U.S. history was the 35-day shutdown in 2018-2019 under the Trump administration, triggered by an impasse over border wall funding. This event cost the American economy at least $11 billion and notably ended after widespread absences among unpaid air traffic controllers forced a resolution. While markets have historically shown resilience, recovering relatively quickly after most shutdowns, the recurring nature of these events erodes public trust in governance and fiscal stability, and a prolonged or frequent occurrence can have more significant, long-term negative impacts on economic growth and international perceptions of U.S. reliability.

What Comes Next: Navigating the Uncharted Waters of Fiscal Uncertainty

The path forward following a government shutdown and the accompanying Treasury rally is fraught with both immediate challenges and long-term implications, demanding strategic pivots from businesses and investors alike. While historical precedents suggest a degree of market resilience, the current environment, marked by persistent political polarization, introduces a new layer of complexity.

In the short term, expect continued market volatility as the duration and resolution of the shutdown remain uncertain. The "flight to quality" into U.S. Treasurys is likely to persist, keeping yields suppressed, and gold may also benefit from its safe-haven status. Economically, each week of a shutdown could shave off an estimated 0.1% to 0.15% from annualized GDP growth, primarily due to furloughed federal workers and halted government spending. Crucially, the "data blackout" will continue, delaying vital economic indicators such as employment figures and inflation reports, thereby complicating the Federal Reserve's (US:FED) ability to make informed interest rate decisions. Sectors heavily reliant on government contracts or regulatory approvals, like federal contractors and industries awaiting permits from agencies such as the SEC (US:SEC) or FDA (US:FDA), will continue to face immediate disruptions and cash flow pressures.

Looking at the long term, a prolonged or frequently recurring shutdown could inflict more permanent economic damage, moving beyond temporary disruptions to permanently lost GDP. This repeated fiscal brinkmanship risks eroding investor confidence in U.S. governance and its fiscal reputation on a global scale, potentially leading to a re-evaluation of investment strategies and even a gradual shift in global capital flows away from the U.S. Moreover, while interest payments on Treasurys continue, persistent political instability could eventually impact the U.S. credit rating. The threat of permanent federal job cuts, a more severe possibility than traditional furloughs, could also have a lasting negative impact on the labor market and consumer spending.

Strategic pivots for businesses and investors are paramount. Companies with significant federal dependencies must implement robust contingency plans, managing cash flow carefully and potentially delaying non-essential projects. Diversifying information sources to include private-sector data and industry-specific surveys will be crucial to mitigate the impact of official data blackouts. For investors, this period of volatility presents an opportunity to rebalance portfolios, potentially increasing exposure to U.S. Treasurys as a safe haven and upgrading the quality of equity holdings. Diversification across sectors less susceptible to government disruption (e.g., utilities, consumer staples, select defense contractors) and even across geographies can help mitigate risks. A fundamental focus on companies with strong balance sheets and durable earnings capacity will provide a hedge against policy uncertainty.

Market opportunities may emerge in safe-haven assets like Treasurys and gold, while a post-shutdown rebound, historically observed, could offer buying opportunities for those with a long-term perspective. Certain resilient sectors, such as defense, healthcare, and utilities, may continue to outperform. Conversely, challenges include heightened market volatility, persistent regulatory bottlenecks, and the pervasive uncertainty stemming from the "data blackout," all of which can dampen consumer and business confidence.

Several potential scenarios could unfold. The most common historical outcome is a short, contained shutdown, leading to a quick market recovery and minimal, reversible economic impact. However, a prolonged shutdown with political stalemate would result in a more significant economic drag, deeper erosion of confidence, and potentially push the Federal Reserve towards earlier rate cuts due to weaker economic signals. A more severe, though less frequent, scenario involves a shutdown with permanent job cuts, which would have a substantial and sustained negative impact on the labor market and consumer spending. Finally, a pattern of repeated shutdowns and fiscal brinkmanship could cumulatively damage U.S. fiscal reputation, potentially leading to a long-term shift in global capital flows and even rising long-term sovereign bond yields as investors demand higher compensation for increased political risk. The market's ability to absorb these shocks, therefore, hinges not just on the immediate resolution but on the broader trajectory of U.S. fiscal governance.

Wrap-up: Navigating Through Political Headwinds

The current government shutdown, marked by a rally in Treasurys, serves as a potent reminder of the interplay between political stability and financial market dynamics. While the immediate economic impact of past shutdowns has often been muted and temporary, the recurring nature of these events demands a careful assessment of their cumulative effects and future implications.

Key takeaways from this event include the consistent "flight to quality" into U.S. Treasurys, which drives yields down as investors seek safety amidst uncertainty. While equity markets may experience short-term volatility, their historical resilience suggests that the overall impact on broader market performance is often limited. However, the "data blackout" caused by the cessation of non-essential government services remains a critical concern, complicating economic analysis and Federal Reserve policy decisions. The potential for a more significant economic drag increases with the duration and contentious nature of the shutdown, particularly if it involves permanent federal job cuts or coincides with debt ceiling debates.

Assessing the market moving forward, investors should understand that while political noise can create short-term fluctuations, fundamental drivers like economic growth, corporate earnings, and interest rates typically dictate long-term market performance. The lasting impact on overall equity performance and economic growth has historically been minimal for short shutdowns. However, repeated fiscal brinkmanship can subtly erode trust in U.S. governance and fiscal stability over time, a harder-to-quantify but significant long-term risk.

What investors should watch for in coming months will be crucial. First, the duration and specific terms of the shutdown's resolution will signal the immediate path forward. Second, the resumption of key economic data releases (e.g., jobs report, CPI) will provide much-needed clarity on the economy's health. Third, the Federal Reserve's response to this data, particularly regarding interest rate policy, will be paramount. Fourth, corporate earnings reports, especially from companies with significant government exposure, will reveal the direct financial impact. Finally, monitoring consumer and business sentiment will offer insights into broader economic activity. In times of uncertainty, a focus on strong fundamentals and a diversified portfolio, potentially including defensive sectors and safe-haven assets like short-duration Treasuries and gold, remains a prudent strategy.

This content is intended for informational purposes only and is not financial advice